The three things investors should know this week

Global bond and equity markets have been markedly weaker in the beginning of the year.

The reason behind this is policy uncertainty out of Washington, both on the executive and the central bank level. Although some weakness is highlighted, the UK is impacted similarly to most markets in the world.

However, we need to remember bonds have a yield, and this means they have a floor. Bonds simply don’t crash the same way as equities.

----------------------------

Summary

The Fed’s double about-turn and policy uncertainty have contributed to market weakness in both bonds and equities since the beginning of the year. Bond markets are now pricing in one to two rate cuts by the end of the year, on aggregate, and we would not be too surprised if some investors begin to price in rate hikes. There are many factors aggravating the problem, such as overall policy uncertainty, the high level of debt across the world, large debt issuance ahead and a debt ceiling battle coming up in the US. However, we need to remember something about bonds: They have a yield, and this means they have a floor. Bonds don’t crash the same way as equities, except in a debt crisis (we don’t appear to be in one). As prices fall, yields rise. As such, after a point (usually around 5%) they become more attractive, limiting their downturn.

This is a US-related policy uncertainty issue, reverberating across global bond markets. Markets may highlight individual weaknesses, but ultimately the source of this bond downturn is in Washington. And, likely, so will the solution.

-----------------------------

The year started on a negative note for risk assets, for both global equities and bonds. Equities are down 4.5% since their December highs and bonds down 6.5% from their own September highs.

Why are we witnessing a bond rout?

The answer is simple: The Fed’s double about-turn and policy uncertainty.

The Fed’s surprise decision to perform a double (0.5%) cut in September while essentially declaring victory over inflation, sent a signal to financial markets that it was prepared to aggressively cut rates in the end of 2024 and into 2025. After that meeting, bond markets were pricing an end US rate for 2025 at 2.7%. The 10-year Treasury found a floor at 3.6% and equities rallied. From that point on, we noted that risks were on the upside, and often repeated that if it didn’t follow through with such a signal, the Fed would be sending a wrong message.

In the weeks that followed, the Fed tried to moderate the signalling impact of the double cut, by suggesting that similar cuts would not necessarily follow. The bond market started weakening from that point, although equities remained on a positive track. It is worth noting that until a couple of weeks before the US election, the result was considered a toss-up.

In November, the US election resulted in a Republican trifecta, which would allow Mr Trump more room to implement trade tariffs across the board, a move generally considered inflationary. Inflation expectations started climbing faster, and bond prices came down (bonds have fixed payments, so their owners dislike inflation).

In its mid-December meeting the Fed completed its about-turn suggesting that it was now more mindful of inflation. From that point on, equities began to slip as well.

Bond markets are now pricing in one to two rate cuts by the end of the year, on aggregate, and we would not be too surprised if some investors begin to price in rate hikes.

There are many factors aggravating the problem, such as overall policy uncertainty, the high level of debt across the world, large debt issuance ahead and a debt ceiling battle coming up in the US.

However, we need to remember something about bonds: They have a yield, and this means they have a floor. Bonds don’t crash the same way as equities, except in a debt crisis (we don’t appear to be in one).

A “bond yield” is a promise to investors about fixed returns for a fixed period. Holding a bond to maturity, an investor knows exactly what they will get, unless a default happens (no one is pricing one in).

As prices fall, yields rise. As such, after a point (usually around 5%) they become more attractive, limiting their downturn.

Does this rout have any extra implications on UK investors and businesses?

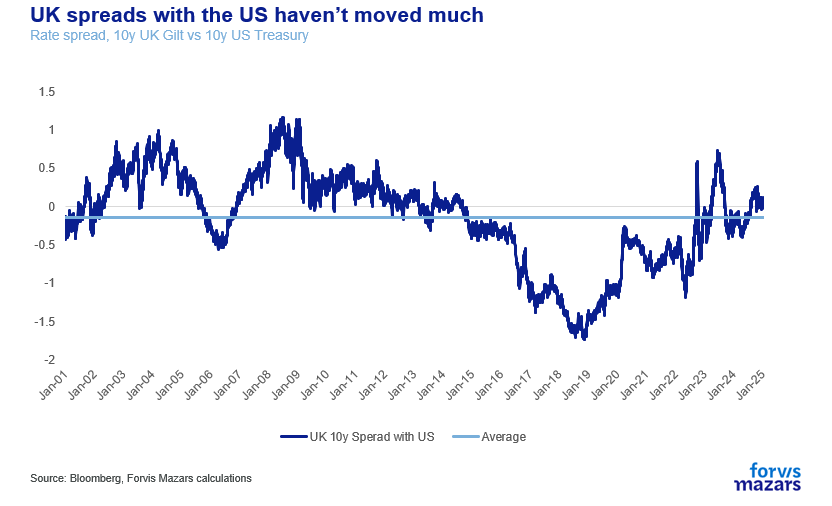

The sharp move in bonds even prompted questions to the UK Chancellor in the House of Commons, dramatizing the situation. Yet, there’s nothing particularly bad about His Majesty’s Government Debt. The spread of the 10yr Gilt and the 10yr Treasury is fairly stable, which suggests that UK debt is following the US. The Pound is weaker vs the Dollar, to be sure, but again that’s due to perceptions of higher inflation in the US. It did take a 1.4% plunge against the Euro, but it’s still 2.5% up since August.

The UK economy is stable. For 2025 the IMF projects growth of 1.5%, while it downgraded EU’s growth from 1.5% to 1.2%. The UK has a relatively stable government (Germany is faced with elections in February and France is politically unstable), which seems keen to facilitate business growth, even by pressuring regulators to accept more risk.

The UK’s extra problem is really its debt structure.

As yields and inflation expectations rise, so do inflation-linked Gilts. For the UK this is a particular problem, a quarter of the debt is inflation-linked, more than double that of the next large economy’s, which means that interest payments also rise, limiting fiscal space. This means that the government will need more funding. This can come either from more borrowing or with higher taxes. Borrowing may have been the government’s preference, and could still happen, but with long yields going up, repayments will become onerous, and increasing the supply of UK debt in this market is becoming more difficult.

So now investors are beginning to think that the government will be left with no solution, other than to increase some taxes or cut spending during the Spring Budget. We believe that the decision will be made further down the line, when bond markets are calmer and the government has a better inkling as to what sort of repayment schedule its facing.

In conclusion, this is a US-related policy uncertainty issue, reverberating across global bond markets. Markets may highlight individual weaknesses, but ultimately the source of this bond downturn is in Washington. And, likely, so will the solution.