The Baltic Dry Index slipped into the red last week after six consecutive weeks of gains. The capesizes and panamaxes contributed jointly to the weakness, as the smaller segments remained in the black. For commodities, the past week also delivered mixed performances. Iron ore was among the winners, as the steelmaking ingredient staged a rebound as traders recovered some of their optimism.

By Ulf Bergman

Macro/Geopolitics

The US dollar continued to gain ground last week as investors became increasingly convinced that the Federal Reserve will keep interest higher for longer. After gaining 0.7 per cent during the preceding week, the US dollar index ended Friday’s session with a 0.6 per cent gain for the week. The new week has seen the gauge stabilising as traders await the release of the PCE price index report, the US central bank’s preferred inflation gauge, on Friday. Markets are expecting core inflation to edge down marginally from January. However, in line with the recent propensity of US economic data to surprise on the upside, a stronger-than-expected reading could see the greenback gaining further strength. Such a development would weigh on the demand for commodities and seaborne transportation, generating downward pressure on prices and freight rates.

Commodity Markets

Crude oil saw some volatility throughout the past week as several supply-side issues and concerns over demand competed for traders’ attention. Early gains were offset later in the week, and the May Brent futures ended Friday’s session at 85.43 dollars per barrel, broadly in line with the preceding week’s close. The new week has begun with gains of around 1.5 per cent amid rising concerns over global supplies.

European natural gas prices ended the past week near their highest levels since early February, as maintenance and repair outages in Norway and the US limited supplies. The front-month TTF futures settled at 27.78 euros per MWh, a 2.8 per cent gain for the week. The contracts have also continued to gain in today’s session, trading around two per cent above Friday’s close.

The benchmark futures for the Asian and European coal markets had another week of diverging fortunes. The contracts for delivery in the port of Newcastle next month recorded a weekly decline of 4.7 per cent, settling at 124.50 dollars per tonne on Friday. Concerns that Chinese demand will soften amid the potential for an oversupplied market contributed to the losses. On the other hand, the futures for delivery in Rotterdam in April gained nearly half a per cent over the course of the past week as higher natural gas prices supported demand.

While iron ore endured some volatility over the past five trading sessions, it was with an upward trend as the steelmaking ingredient moved into recovery mode. The April iron ore futures listed on the SGX recorded a weekly gain of 8.2 per cent, settling at 108.14 dollars per tonne on Friday. The weekly gain offset some of the losses sustained during the preceding week as traders recovered some optimism over the Chinese demand outlook. Today’s season has maintained last week’s positive momentum amid limited gains.

Looming concerns over the Chinese demand outlook and a stronger dollar contributed to losses for many base metals last week. The three-month copper futures listed on the LME recorded a weekly decline of 2.3 per cent, while the zinc and nickel contracts dropped by 3.0 and 4.6 per cent, respectively, over the period. However, the aluminium futures went against the flow and recorded a weekly gain of 1.5 per cent on robust demand.

After three consecutive weeks of losses, the May wheat futures listed on the CBOT rose by 5.0 per cent over the past five trading sessions as Russian attacks on Ukrainian ports raised the prospects of global supply disruptions. The corn contracts edged up by 0.6 per cent over the past week, while the soybean futures shed half a per cent.

Freight and Bunker Markets

After six consecutive weeks of gains, the Baltic Dry Index fell into the red last week as the capesizes and panamaxes faced headwinds. The headline index dropped by 7.5 per cent but remained 51 per cent above the level seen a year ago. The sub-index for the largest vessels sailed into considerable headwinds and declined by 13.4 per cent, with rising tonnage supply in the Atlantic contributing to the negative sentiments. Still, falling market lead times and increasing order volumes suggest that the weakness could prove shortlived. The gauge for the panamaxes recorded a weekly decline of 3.1 per cent amid downward pressure on cargo order volumes across the major basins. On the other hand, the smaller segments enjoyed a week of gains. The indicators for the supramaxes and handysizes rose by 4.3 and 1.8 per cent, respectively, as softer tonnage supply supported freight rates.

Red dominated the past week for the Baltic Exchange’s wet freight indices, with only the clean tankers escaping the negative territory. Concerns over crude oil demand and possible supply disruptions contributed to the dirty tanker index recording a weekly decline of 3.4 per cent. The gauge for the LPG tankers dropped by 20.3 per cent over the week, while the index for the LNG carriers shed a quarter of a per cent. The clean tanker index was the outlier, with a weekly gain of a third of a per cent.

The bunker-fuel trading swung between daily gains and losses throughout the past week. As a result, weekly price moves were limited in several ports. In Singapore, the VLSFO recorded a weekly decline of 0.5 per cent, while the MGO shed 0.3 per cent. The former fuel ended Friday’s trading unchanged compared to a week earlier in Rotterdam. On the other hand, the European port recorded a weekly decline of 2.2 per cent for the MGO. In Houston, the two fuels had a week of diverging fortunes. The VLSFO gained 1.5 per cent, while the MGO shed 2.0 per cent.

The View from the Shipfix Desk

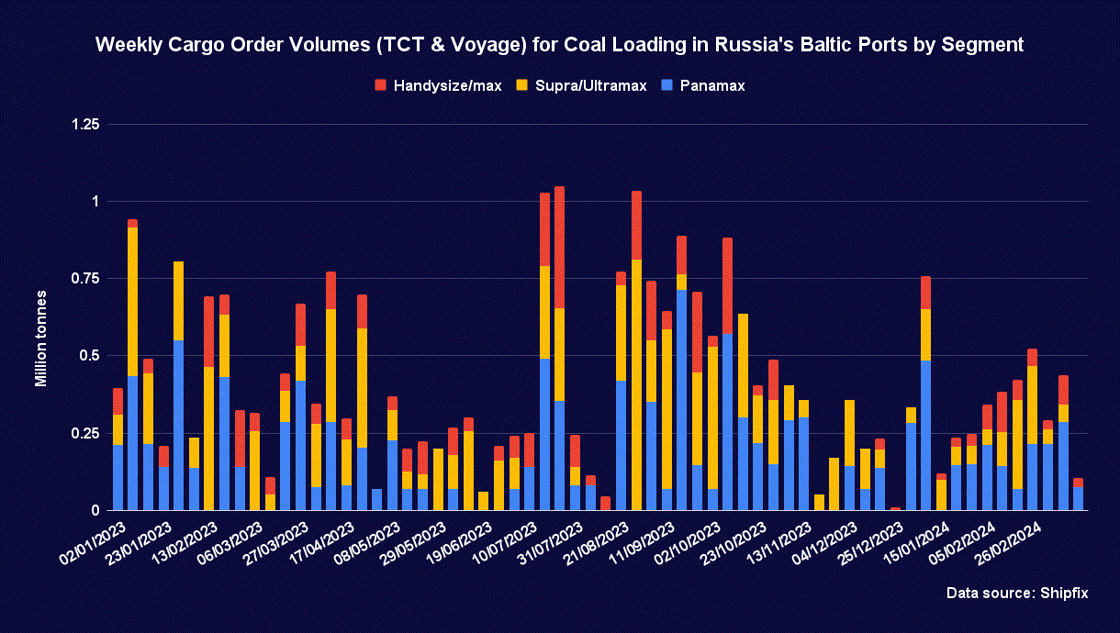

European coal prices are currently trading at the highest levels seen since early November last year. Still, despite gaining around 30 per cent over the past five weeks, the prices remain around 25 per cent below what was observed nearly a year ago. Rising natural gas prices have fueled the somewhat unseasonal surge over the past month amid supply disruptions, which has led to higher demand for the dirtiest of fossil fuels.

Traditionally, supplies from the nearby Russian ports in the Baltic Sea would have satisfied a rise in European coal demand. However, with European sanctions in place for Russian coal imports, the coal trade from the Baltic Sea has lost some of its previous importance. While the loss of the European market has led to lower cargo order volumes, the nature of the trade has also changed, with voyages becoming longer.

While weekly cargo order volumes for Russian coal loading in the Baltic Sea have been trending higher since the middle of January, they still remain relatively low in a historical context. Also, the data for the past three weeks suggest that demand may hit a soft patch. The depressed ordering activities have, to a great extent, weighed on the market for seaborne transportation onboard the smaller vessel segments. The longer voyages in the trade to destinations such as India have greatly favoured the panamaxes. The segment has accounted for around 55 per cent of the market since the beginning of the year, compared to 43 per cent during the same period last year.

Data Source: Shipfix