In the first two months of 2024, China has experienced a robust start in foreign trade.

"In a torrid week for banking stocks, and for stock markets in general, Baltic indices showed their mettle, being one of the least volatile asset classes in the eleventh trading week! In an eventful week, the Baltic Dry Index managed to stay on an upward trajectory, concluding today at 1535 points" was the opening paragraph of Doric's weekly insight this week last year. Back then, midweek, Credit Suisse shares tumbled by as much as 30 percent to an all-time low, following comments from its largest shareholder that it would not provide the bank with any additional capital. One day earlier, the Zurich-based bank said it had identified “material weaknesses” in its internal controls over financial reporting.

One year later, the twelfth trading week unfolded without any headline-grabbing events. In this regard, it was a rather uneventful week, marked by a downward correction in the Dry Baltic index to 2196 points. Despite cruising for fifteen consecutive trading days in the $30,000 daily territory, the leading Capesize index concluded the week down at $28,875 daily. Similarly, after reaching multi-month highs of $20,685 daily on Monday, the Baltic Panamax index declined to $19,483 daily by Friday's close. On the other hand, the geared segments of the market reported gains, with the Supramax and Handy indices balancing at $15,212 and $14,309 daily, respectively.

Despite a recent semblance of calmness in the international trade, debates have emerged lately regarding the fairness of China's trade practices. An increasing number of Western nations argue that Beijing's subsidization of domestic manufacturing provides an unfair competitive advantage in international markets. In contrast, Beijing defends its production efficiency and dismisses the accusations made by Western countries.

Earlier this month, the European Commission emphasized that it has gathered "sufficient evidence" indicating that imports of new battery electric vehicles from China have received subsidies. These subsidies include direct transfer of funds, tax breaks, or the provision of goods or services by the public below market prices. As a response, the Commission initiated an anti-subsidy investigation into Chinese battery electric vehicles to assess whether tariffs should be imposed to safeguard EU producers. The investigation is set to conclude by November, although provisional duties could be imposed as early as July. In response to these developments, the China Chamber of Commerce to the EU expressed disappointment, stating that the surge in imports reflects the increasing demand for electric vehicles in Europe. China's auto exports surged 30.5 percent year-on-year to 822,000 units in the first two months of this year, data from the China Association of Automobile Manufacturers showed.

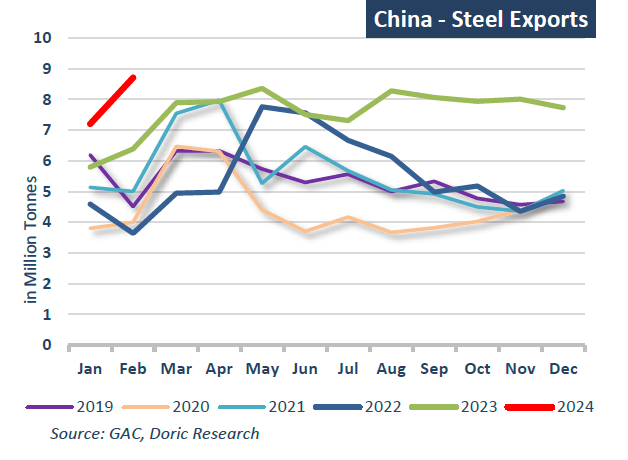

On the same wavelength, Brazil's Ministry of Industry has launched several investigations into the alleged dumping of industrial products by China, as Latin America's largest economy faces a surge of cheap imported goods. Specifically, the Brazilian Ministry of Development, Industry, Trade, and Services has initiated an investigation targeting the imports of flat rolled products of iron or non-alloy with thickness lower than 0.5 mm from China. Notably, this investigation does not encompass the primary concerns of the Brazilian steel industry, namely HRC and CRC. The Brazilian Steel Institute is advocating for an increase in the import tax on these products to 25 percent, up from the current average of 12 percent. However, Brasília is likely to seek to avoid a confrontation with Beijing, given that China is Brazil's largest trading partner and a significant purchaser of commodities such as soybeans and iron ore. In addition to Brazil, China’s steel exports to Vietnam, Thailand, Malaysia and Indonesia have risen sharply in recent months.

In the first two months of 2024, China has experienced a robust start in foreign trade. According to the General Administration of Customs, from January to February, China's foreign trade in goods amounted to 6.61 trillion yuan (about $930.96 billion), marking an increase of 8.7 percent year-on-year. Exports showed significant growth, rising by 10.3 percent year-on-year to reach 3.75 trillion yuan, while imports also saw a notable increase, rising by 6.7 percent from the same period in 2023 to 2.86 trillion yuan. Notably, exports of machinery and electronic products accounted for nearly 60 percent of the country's total exports during this period, underlining the significance of these sectors in China's trade landscape. During the same period, China's trade with its largest trade partner, the Association of Southeast Asian Nations, increased by 8.1 percent year-on-year, reaching 993.24 billion yuan. This accounted for 15 percent of the country's total trade value. Additionally, China's foreign trade with its Belt and Road Initiative partners amounted to 3.13 trillion yuan, reflecting a year-on-year growth of 9 percent.

As international criticism escalates over Chinese industrial oversupply, a roster of global chief executives, including Apple’s Tim Cook, ExxonMobil chair Darren Woods, and HSBC’s Noel Quinn, is expected to attend China’s equivalent of Davos in Beijing this weekend. Beijing aims to address the mounting international criticism of its response to weakened demand stemming from a property slowdown by further stimulating manufacturing. However, analysts caution that this policy could exacerbate oversupply and dumping on global markets, posing a threat to the industrial bases of China’s trading partners. These diverging dynamics highlight the intricate and contentious nature of global trade, particularly concerning China's role and its impact on international markets.

Data source: Doric