Crunch Time

Three recent developments suggest a changing market for VLCCs over the age of 20:

The US sanctioned another 21 tankers this week for involvement in the Iranian oil trade, bringing the total number of sanctioned VLCCs up to 80, or 9% of the global VLCC fleet.

China cut back its imports of sanctioned crude grades in November, including oil from Iran.

Two shadow fleet VLCCs are being pushed in the market for demolition. If they are scrapped they will be the first VLCCs to go to the breakers since 2022.

Sanctions on Iranian exports, which we believe will only get tougher under Trump, have raised the cost of imports from the country for independent Chinese refiners, the main buyers. Declining refining margins in China since summer have increased competition for discounted grades, also raising prices relative to non-sanctioned crude sources. As a result, China cut back its imports of Iranian crude in November. If sanctions continue to make Chinese customers wary of Iranian barrels, the VLCCs over the age of 20, which carry the majority of Iranian oil, are likely to be scrapped. Two VLCCs with Iranian history are already being pushed for demolition. Others will follow.

This week, the US sanctioned another 35 entities and vessels involved in transporting Iranian oil, including 10 VLCCs and a number of China-based ship management firms. The sanctions build on those imposed on 11 October following Iran’s 1 October missile attack on Israel. Lower oil prices have opened the door for the US to ramp up sanctions on Iran, providing room to disrupt Iranian exports without raising prices at the pump. Brent has averaged $81.10/bl so far this year, compared to $82.5/bl in 2023 and $101.10/bl in 2022. Since mid-October it has traded between $71/bl and $77/bl. OPEC+ is widely expected to again delay the return of 2.2mn b/d of oil to the market when it meets today. But even without any additional OPEC+ barrels, the IEA is forecasting a surplus of more than 1mn b/d next year because of cooling global demand as top importer China falters and the US, Guyana and Canada increase exports. A renewal of Trump’s “maximum pressure” strategy will force Iran’s fleet of overage VLCCs into floating storage or out of the fleet all together.

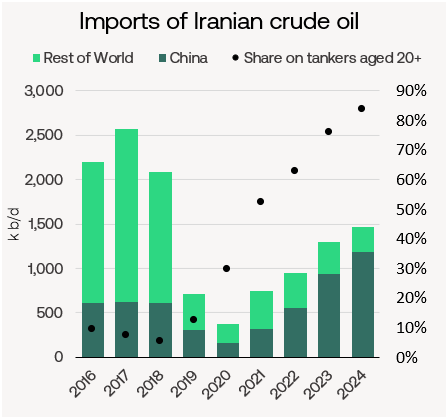

Iran has provided the majority of employment for VLCCs turning 20 years old in recent years. So far in 2024, two-thirds of the crude oil on 20+ year old VLCCs has been Iranian, with another 9% Venezuelan. VLCCs aged over 20 years made up 14% of oil on VLCCs this year, from 5% in 2021. Iranian crude oil exports have soared from 400k b/d in 2020 to 1.4m b/d in 2024. This output travels aboard an aging armada: in 2019, just 12% of Iran’s oil exports used ships over 20 years old; today, that share is 82%. As the US steps up its sanctions efforts, one third (52) of the 148 VLCCs that will be over 20 at some point next year (assuming no scrapping) are already subject to OFAC sanctions. Of the Iranian oil on 20+ year old VLCCs, 88% went to China this year. If sanctions take Iranian exports back to 2020 levels it will be a cut of 1mn b/d and remove two-thirds of the current demand for VLCCs over the age of 20. Saudi Arabia, the UAE and others would likely be the ones to replace Iranian exports to China, supporting demand for compliant VLCCs.

China’s independent refining sector has maximised its imports of discounted crude since the country emerged from COVID. Imports of crude from Russia and Iran has more than doubled from January last year to October 2024, at a time when China’s imports from the rest of the world (on compliant tankers) declined. The growth of Iranian crude exports to China peaked in October last year. Declining refining margins since summer have increased competition for discounted grades, raising prices relative to non-sanctioned crude sources. A recent tightening of sanctions on trade finance and the vessels carrying crude from sanctioned exporterers has further diminished the advantage of importing crude from Russia and Iran. Chinese import data for November, according to Vortexa, suggest that while import volume is up by 7% on the previous month, shadow exporters’ share of imports has shrunk considerably. Imports from Venezuela, Russia and Iran made up a third of China’s crude oil imports in October but that dropped to just over a quarter in November. Sanctions raise the risk of disruptions to supply or sudden price increases for Iranian crude, reducing appetite for Iranian crude and the aging tankers that carrying it. The larger private-sector refiners have already reportedly stepped back from purchases of Iranian oil.

Around 44% of Iranain oil cargoes on VLCCs this year were on sanctioned tankers. This, and their age, makes it unlikely that these ships will be able to easily return to unsanctioned trades. Some will be go back into floating storage but most will be scrapped, although sanctions may complicate this, if Iranian exports are cut back significantly and lastingly. For VLCCs turning 20 soon, unless age restrictions are relaxed more widely on unsanctioned trades, these tankers will more likely find themselves in breaking yards, as they did before 2020, than carrying oil.