Key takeaways from this report:

Dirty – East of Suez: Fuel oil tightness and weaker refining margins to support tonne-miles

Clean – East of Suez: Longer-haul VLGC voyages supressed, but situation could be changing

Dirty – West of Suez: TMX raises supply competition for heavy sour crudes in the US Gulf, presents opportunity for Aframaxes

Clean – West of Suez: LR2s likely to win out in a changing European refining landscape

By Mary Melton

Dirty – East of Suez: Fuel oil tightness and weaker refining margins to support tonne-miles

The current depressed refining margins for clean petroleum products (CPP), amid ongoing fuel oil supply tightness, could provide significant support to the dirty tanker market, particularly for Aframax and Suezmax vessels

➔ A lighter crude slate, combined with US sanctions on Russian oil, has tightened global supplies

➔ The re-routing of Russian fuel oil to Asia continues to support global tonne-mile demand

Weaker refining margins may lead refineries to reduce operations in secondary processes/desulphurisation units, thereby increasing fuel oil output in the market

Should the flow of fuel oil along the Russia-to-Asia route continue to increase, this will further bolster tonne-mile demand

➔ This trend will be especially evident if fuel oil prices remain below the price cap, encouraging more Western-operated Aframax and Suezmax

➔ These operators prefer the longer route via the Cape of Good Hope, rather than transiting via the Suez Canal

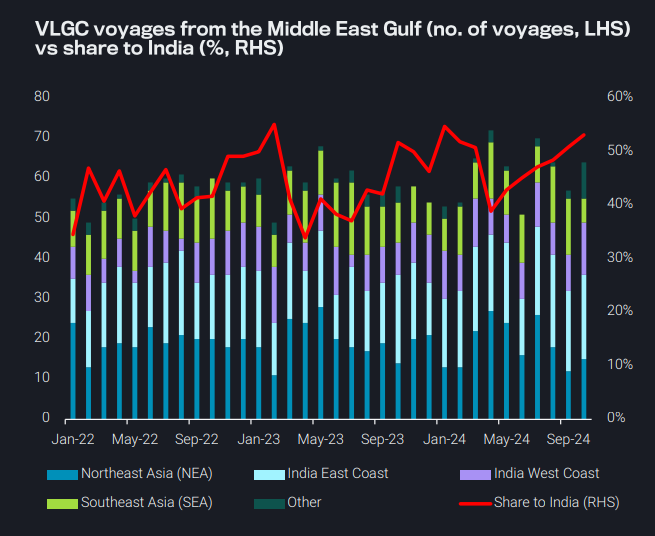

Clean – East of Suez: Longer-haul VLGC voyages supressed, but situation could be changing

VLGC freight rates MEG-to-Japan (BLPG1) and US Gulf-to-Japan (BLPG3) remain under pressure compared to 2023 levels

LPG carrier transits via the Panama Canal are recovering, minimising turnaround time for VLGC voyages and adding downwards pressure on rates

Declines in longer-haul utilisation from the MEG-to-East Asia is another important factor contributing towards falling freight rates, as weaker ethylene cracker and PDH margins reduced demand for LPG

➔ Additionally, short-haul utilisation to India increased over the last few months, as pricing favoured LPG for power in industrial and residential use

Around 20% of PDH capacity is offline in China. When this returns, we should expect to see more LPG flows East, which will support tonnemile demand

➔ With a return in demand from East Asia, increasing LPG exports from the US Gulf may face increased Panama Canal congestion, as LPG carrier transits are not prioritised over other vessel types, which should support freight rates

Dirty – West of Suez: TMX raises supply competition for heavy sour crudes in the US Gulf, presents opportunity for Aframaxes

With the TMX opening, more heavy-sour Western Canada crude is absorbed by PADD 5 in the seaborne export market or sent to Asia

➔ This has led to a loss in market share in PADD 5 for Colombian heavy-sour crude

➔ As a result, more Colombian crude has headed to PADD 3

The share of voyages arriving in the US Gulf from the Caribbean increased to over 25% in October

➔ This includes Venezuelan arrivals on sanctions waivers, but also encompasses arrivals from Colombia, which have been elevated since TMX loadings commenced

Moving forward, this presents an employment opportunity for the Americas Aframax market, which has had to contend with increasing competition from Suezmaxes

➔ Especially when the Olmeca refinery opens, and reduces heavysour Maya crude loadings at Dos Bocas, PADD 3 could increasingly look to Colombia as a supplier

Clean – West of Suez: LR2s likely to win out in a changing European refining landscape

Structural changes to the European CPP market is shifting tanker demand in favour of the larger vessel classes

High imports of middle distillates from the Wider Arabian Sea, combined with declining gasoline demand from West Africa and PADD 1, have tilted tonne-mile demand in favour of LR2s

Higher tonne-mile demand for TA diesel flows has provided some demand support for MRs arriving into Europe, but this does not offset the significant loss in traditional gasoline employment for voyages outside of the continent (on average 1.8 bn tonne-miles per month compared to 2021)

➔ European MRs are increasingly competing on Handysize routes

In contrast, middle distillate arrivals from the Wider Arabian Sea (especially since Cape of Good Hope rerouting has become the norm), have translated to an average gain of 18 bn tonne-miles per month in 2024 compared to 2021 As European refinery margins continue to be under pressure, which could lead to further run cuts and shutdowns, inflows of middle distillate from the East will remain elevated

Data Source: Vortexa