Key takeaways from this report:

Dirty – East of Suez: Russia-China crude trade may see support due to Iranian supply hiccups and Northern Sea Route closure

Clean – East of Suez: LR transits around the Cape of Good Hope increase, but trend could prove short-lived

Dirty – West of Suez: Red Sea impact on crude rates proved mild, but attack concerns pivoted Suezmaxes to the Atlantic Basin

Clean – West of Suez: 2024’s record-high TC14 employment is a stark contrast to an increasingly short-haul Atlantic MR market

By Mary Melton

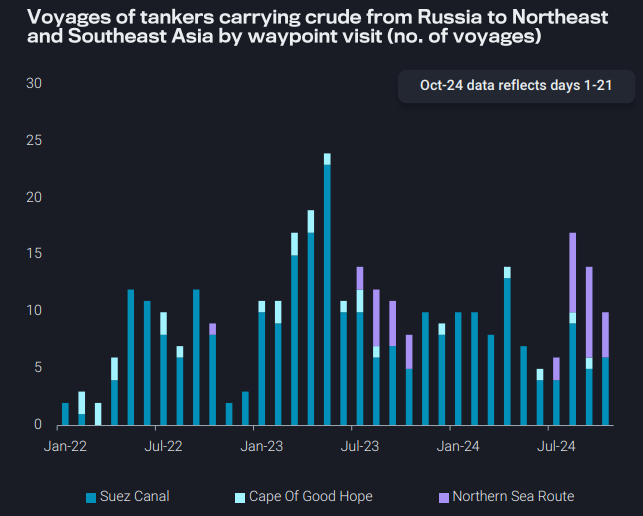

Dirty – East of Suez: Russia-China crude trade may see support due to Iranian supply hiccups and Northern Sea Route closure

Tonne-miles for Aframaxes and Suezmaxes carrying crude from Russia Baltic, Black Sea, and Arctic-to-China are expected to remain strong this month, as Chinese refiners may increase interest in Russian Urals and Arctic crude amid potential disruptions in Iranian oil supplies

➔ If Iranian crude supplies face disruptions, Chinese refiners are likely to turn to other discounted sources, with long-haul Russian Urals and Arctic crude being key alternatives

In addition, as the winter season approaches, tankers will shift to longer routes through the Suez Canal or around the Cape of Good Hope, rather than using the Arctic route

➔ The Northern Sea Route offers a shorter transit time for Aframaxes transporting crude from Ust-Luga to Qingdao, taking approximately 27 days, compared to 40 days via the Suez Canal and 51 days around the Cape of Good Hope

➔ This shift is already evident, with zero Suezmax and fewer Aframaxes navigating the Northern Sea Route this month

Clean – East of Suez: LR transits around the Cape of Good Hope increase, but trend could prove short-lived

LR transits via the Cape of Good Hope declined precipitously in Jul/Aug as employment on the MEG-to-Europe middle distillate route was lost to cleaned-up supertankers, and fewer LR ballasters returned to the MEG after a Europe discharge

However, over the past few weeks, LR transits via the Cape of Good Hope have climbed upwards

➔ A softly open arb for E-W diesel flows (Argus) contributed to an increase in LR voyages MEG-to-Europe at the same time as a small uptick in ballasters heading to the Middle East

➔ Additionally, favourable arbitrage economics for Med naphtha to Asia (Argus) have seen Med-to-Asia transits around COGH increase

Questions around the sustainability of this recent uptick in LR Cape of Good Hope voyages remain

➔ Supertanker clean-ups have slowed in October, but closed arbs will likely limit E-W middle distillate departures

➔ Asia’s naphtha demand may have peaked as reformer and ethylene cracker margins are under pressure

Dirty – West of Suez: Red Sea impact on crude rates proved mild, but attack concerns pivoted Suezmaxes to the Atlantic Basin

As we approach the one-year mark since the beginning of the Red Sea attacks, crude tanker rates have remained relatively unaffected by the events, particularly when compared to the clean tanker segment

➔ This stability can be attributed to shifting employment patterns for Suezmax vessels.

Following the Russian invasion and the EU oil ban on Russia, Suezmax tankers increasingly found employment routes from the Atlantic Basin and the Middle East, rather than the Baltic

➔ However, after the Red Sea development, partly due to fear of attacks for transiting the Bab-el-Mandeb, and partly due to the surge in distances to reach Europe, the majority of Suezmaxes from the Middle East pivoted towards the Atlantic Basin

➔ As a result, arrivals in September for Suezmax voyages operating on the MEG-to-Europe route, reached the lowest point since at least Jan 2022

➔ Projections for October suggest a likely increase in arrivals, as a m-o-m rise in September departures combined with stronger market enquiries has maintained TD23 rates at four-month highs

Clean – West of Suez: 2024’s record-high TC14 employment is a stark contrast to an increasingly short-haul Atlantic MR market

For most of this year, USGC-to-NW Europe MR voyage counts for diesel cargoes have flown past seasonal records

High PADD 3 exports have pushed diesel exports transatlantic, especially considering the loss of Brazil post-Russia invasion as a traditional consumer of PADD 3 diesel

➔ This arrangement is attractive to European buyers, as the freight costs for LRs bringing middle distillates from EoS skyrocketed because of the Red Sea attacks

Although TC14 freight rates have been volatile throughout the summer and in the past two weeks, periods of an open TA arbitrage plus periods of downward pressure on USGC freight rates due to high vessel supply have kept demand robust on this route

The European MR market suffers from a lack of demand on TC2 and to WAf, and short-haul demand from PADD 3 to Mexico East Coast and the Caribbean remains elevated

➔ Robust demand on TC14 remains a big positive for Atlantic Basin MRs in a market increasingly tilting to short-haul trade

Data Source: Vortexa