The three things businesses and investors need to know this morning

Market and business uncertainty does not seem to subside, as tariffs continue to shift fast

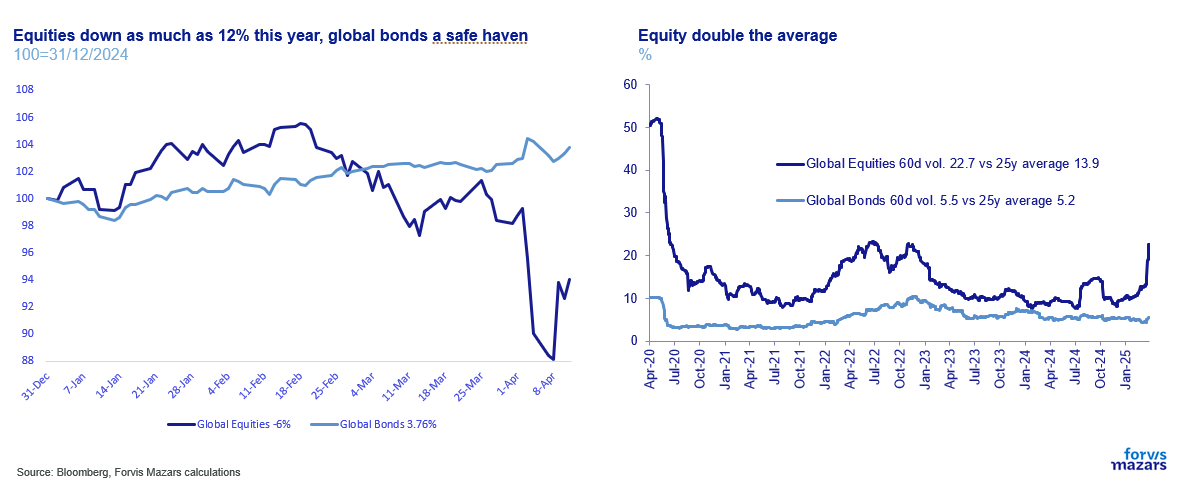

Some market dislocations (borrowing costs up, Dollar down) are suggesting that some market participants might be moving away from US risk assets as safe havens

As days pass, uncertainty may well be factor in as more long-term. This could cause markets and investors to seek “bubbles” of safety.

---------------------------------------

Summary

As trade wars continue, business and investors are seeing volatility and uncertainty rise exponentially. Financial markets are experiencing dislocations, which, continued could invite a Fed intervention. Some market participants, in fact, think that this is now required anyway, to calm nerves. While the probability of a financial and credit event is not very high, as central banks have learned the lessons of the past and can guarantee liquidity, the economy has no such safety net. The post- WWII liberal economic and financial order has come to a halt as the US and China enter the most dangerous phase of ending their unwilling co-dependency. It is still very difficult to imagine the next regime, as no such planning exists. So investors and businesses are looking for pockets of safety and stability. Some of it can be found in central banks. Some in more secure legal regimes, such as Europe. Whatever the case, the more days pass, the wider the long-term repercussions for business planning in the next few years.

----------------------------------------

My grandfather was a life-long boy scout. A few years before the Second World War, a military dictatorship in Greece banned all boy scout regiments, in favour of a military youth regime, echoing those of Germany. During WWII, boy scouts remained banned in occupied Greece and ordered to hand over their insignia. After grandfather became an Naval Officer and went to fight in WWII, his mom, my great-grandmother, hid all the insignia (flags, journals, books, uniforms etc) in an attic. The occupation was particularly brutal in Athens and she risked her life to preserve the boy scout legacy. When liberation came and the regiments re-emerged, she was honoured for her stewardship.

Trade wars continue unabated. Looking to make sense of it all, I realised that investors and businesses don’t want the newsflow, or even look for exact answers. The news is manic, and illuminating answers are unavailable. Instead, what everyone looks for, is “the bigger picture”. Where do we go from here? And whereas the long-term answer is difficult, over the medium term a world that becoming increasingly fatigued with White House uncertainty is looking for someone to hold up the flag and be the steward of the liberal economic and financial order we knew as our reality until a few months ago.

On “Liberation Day”, 2nd April, the word and financial markets were shocked to see the US retreating from the global economic, financial and geopolitical construct itself had carefully devised and painstakingly built up after the Second World War and the fall of the Soviet Union.

The result of imposing the highest tariffs in over a century across the globe, has been a precipitous drop in equity prices and very high financial market volatility.

More importantly, investors have noticed significant economic dislocations. The Dollar, the world’s reserve currency continues to drop, despite the initial inflationary impact of tariffs (which all other things being equal should mean higher interest rates). At the same time, US borrowing costs are moving higher.

This particular move was disconcerting. These two assets (Dollar and borrowing costs) usually move together. If, for example, markets think that the Fed will raise rates, both the Dollar and borrowing costs will rise, and vice versa. On some occasions, we could see the yields hovering lower and the Dollar higher. It would be in times of higher risk, where investors would rush to buy both the US debt and US currency, due to their safe haven status. The selloff of both assets at the same time, signals exactly the opposite, the potential loss of that “safe asset” status quo reserved for the biggest economies in the world.

To be sure we are very far from the Dollar’s retreat as the global reserve currency. Over 57% of global reserves are still in Dollars.

And while the Euro has unexpectedly picked up, it is difficult to imagine emerging market consumers rushing to buy either the European common currency or the Renminbi in times of crisis

As for the bond movements, speculation is rife that funds unwound leveraged positions or that China might have sold off some of its Dollar holdings (which account for roughly 2.2% of total US debt).

Still, the dislocations were enough to give the White House pause. The President announced the delay of extra tariff implementation for 90 days (but still maintained 10% tariffs across the board) for everyone but China, with whom essentially trade has stopped. He shook up his economic team, which is now led by Scott Bessent, whom markets consider thus far a level-headed actor, while Commerce Secretary Howard Lutnick and trade advisor Peter Navarro are confined to more auxiliary roles. Elon Musk, head of Department Of Government Efficiency and a close ally to the President even went so far as stating that he would like a free trade zone with Europe.

For many in the markets, this was a signal that the White House “blinked”. In other words, that the pressure from financial markets was enough for the President to tone down some of his aggressive rhetoric. This notion was further enhanced by a moratorium on import tariffs from China. Yet, late on Sunday, the White House moved quickly to disabuse any notion of potentially return to stability, as both Mr Lutnick and the President emphasised that tech/semiconductor tariffs would eventually be returning.

Where are we left after a tumultuous ten days? America’s trade war is now focusing mostly on China, with the two countries escalating tariffs to the point where trade between them ceases altogether. It marks a very dramatic end to the trade relationship that defined the first quarter of the 21st century.

Policy uncertainty continues to climb. Businesses and markets are still weighing the answer to the most important question for now: whether what we are experiencing is deliberate and planned “negotiation with everyone about everything at the same time” with clear but uncommunicated expected outcomes, or the product of big strategy objectives (re-industrialise the North, assert America’s primacy, reduce debt burdens, close trade deficits) driven by power of personality and lacking a coherent tactical implementation. Did we move from “irrational exuberance” to “irrational uncertainty?”*

However, this isn’t a newspaper. And the data will likely change very soon again in the next few hours. To jump ahead, we need to recognise pillars of stability in an increasingly unstable world. Thus far, we see two: The Fed and Europe.

Markets are waiting for the Fed’s intervention, or at the very least the affirmation of the Fed Put, a reminder that when market stability is threatened it will step in to buy assets. The most important global economic and financial agent, the central bank issuing the global reserve currency is slow to respond, as it is also in a fight for its independence. A few days ago, the US administration asked the Supreme Court for the right to fire heads of independent agencies, which would include Jerome Powell. And while we can’t speculate on SCOTU’s answer, we must assume that the Fed’s fight to maintain its independence against its own government may be, at best, a drawn-out affair.

The more secure bet, markets have been telling us, is Europe. As China and the US fight for primacy in this “post liberal trade order”, the unexpected winner, so far is Europe (including UK). Already, Germany abandoned a mercantilist trade approach, and embraced fiscal expansion, with France expanding its nuclear umbrella. European and British assets, and currencies, have picked up significantly since inauguration day. The UK is moving strategically closer to the EU, turning Brexit’s bad blood into water and putting it under the bridge. Anecdotally, our Partner in charge of the auto sector, Vesco Petkov, told us that he was hearing some concerns from clients who want to move operations to the EU and the UK, as they feel the environment offers more certainty. It makes sense. Strategically, it should not be inconceivable that as the two global economic behemoths, the US and China weaken each other economically, the third economic power, Europe, emerges as a pole of long term liberal-order systemic stability.

Europe has its own internal disagreements and architectural issues. But every day we move away from the pre-tariff liberal world order, could be a day where more investors trust the German Bund and the Euro over the Treasury and the Dollar.

While the US consumer is central to the global economy, businesses need to survive, and so do investors. Right now everyone is holding their breath. But it’s unlikely they will (or can) do so forever. Business leaders need to be able to forecast something in order to function. Portfolio managers can’t (and will not be allowed by their mandates and risks managers) to remain exposed to 9-sigma events (probability 1/14bn if anyone is interested). Every day that passes will be a day where investors and businesses will factor in persistent White House uncertainty and look for ways to move away from uncertainty and find pockets of certainty, hoping that the US will eventually return to the world itself built.

In the next few months we will continue to monitor the situation for all our business and investment clients, with updates available at our Forvis Mazars Tariff Hub (click here)

*The term coined by my good friend John Gaskel, Head of Personal Financial Planning at the ICAEW in London.