Tanker - Weekly Market Monitor

Snapshot of Crude and Product Freight Rates, Supply-Demand

Week 15, 10 April, 2025

Signal Ocean Data Highlights a March 2025 Spike in Aframax Voyages to the Far East

Updated voyage data from Signal Ocean shows that Aframax tanker shipments from Russia’s Pacific ports to the Far East saw a notable month-over-month increase in March 2025, despite a slight year-over-year decline compared to March 2024.

Key Observations: Q1 2025 vs Q1 2024

In March 2025, a total of 44 Aframax voyages were recorded discharging in the Far East, marking a sharp 41.94% increase compared to February 2025. This significant month-on-month rise suggests a tactical end-of-quarter push in exports, likely in response to shifting market conditions and geopolitical signals. However, when viewed year-on-year, the figure reflects a modest decline of 8.33% compared to the 48 voyages logged in March 2024, indicating that broader export activity remains somewhat restrained despite mounting political pressure, particularly from the United States. Looking at the full quarter, Q1 2025 showed slightly lower activity than Q1 2024 overall. While March saw a rebound in shipments, the cumulative voyage data points to a more measured start to the year. This implies that the March increase was likely a short-term tactical adjustment, rather than part of a sustained upward trend.

Drivers Behind the March 2025 Surge

Geopolitical Pressure: U.S. Threatens Tariffs

In late March 2025, the United States escalated its stance on Russian energy exports by reiterating threats to impose secondary sanctions and steep tariffs—ranging from 25% to 50%—on international buyers of Russian crude. This geopolitical development likely triggered a tactical response from both Russian exporters and Asian refiners, who moved swiftly to secure cargoes ahead of any policy implementation. While the year-on-year export volumes dipped slightly in March, the sharp month-on-month increase suggests that the tariff threat played a significant role in the end-of-quarter surge, as market participants sought to front-run potential disruptions to trade flows.

Oil Market Volatility: Brent Falls Below $60

The late-March voyage spike also coincided with heightened market volatility, particularly as Brent crude prices fell below $60 per barrel for the first time since early 2021. This drop followed OPEC+’s unexpected decision to raise output, which pressured global benchmarks and raised concerns about an oversupplied market. In anticipation of further price deterioration, Russian exporters likely front-loaded shipments in March to capitalize on relatively stronger pricing. The increase in Aframax voyages during this period suggests a deliberate effort to move volumes quickly before the market fully priced in the new supply dynamics.

Looking ahead

Although March 2025 did not surpass March 2024 in overall voyage count, the observed surge highlights the Aframax segment’s acute sensitivity to short-term shifts in policy and pricing. These vessels remain central to Russia’s Pacific export strategy, notably as sanctions have reshaped traditional trade routes.

Signal Ocean’s granular voyage data provides valuable real-time insight into these shifts, revealing how operators recalibrate flows in response to both geopolitical pressure and market fundamentals—even when longer-term trends appear flat or subdued.

Signal Ocean's real-time voyage data offers valuable insight into how operators adjust flows in response to geopolitical pressure and market fundamentals.

The first half of April saw mixed momentum in crude oil freight market sentiment, with downward trends in the VLCC and Aframax segments, while the Suezmax segment maintained a degree of firmness.

VLCC freight rates on the MEG–China route dropped to WS53, marking a 7% monthly decline. Suezmax rates from West Africa to continental Europe remained strong, holding above WS100 and marking a 17% month-on-month increase. Meanwhile, rates on the Baltic–Mediterranean route held steady at WS130, reflecting the same firm sentiment seen in mid-March and standing 24% higher than the previous month.

Aframax freight rates in the Mediterranean fell to WS160, representing a 10% decline week-on-week, yet remaining 30% higher than the levels recorded last month.

LR2 AG freight rates continued a soft downward trend from the end of March with rates at WS135, reflecting a 13% weekly decrease.

Panamax Carib-to-USG settled at approximately 210 WS, reflecting a 40% increase for the week.

MR1 freight rates for Baltic-to-Continent shipments hovered around WS150, representing a 20% monthly decrease.

MR2 freight rates for shipments from the Continent to the US Atlantic Coast (USAC) reached WS145, reflecting a 15% weekly decrease. Meanwhile, MR2 rates on the US Gulf–to–Continent route dropped to WS100, marking a 20% weekly decrease.

The number of available crude tankers remains below the yearly average; however, there is upward pressure on the VLCC and Suezmax, driving activity toward the annual average.

VLCC Ras Tanura: The current number of ships is around 60, almost 10 lower than the annual average.

Suezmax Wafr: The current number of ships is around 49, up significantly from approximately 40 at the start of the year.

Aframax Med: The first days of April indicated a downward trend, as the number of ships remained below the annual benchmark of 10.

Aframax Baltic: The ship count stood at approximately 21, nearly 10 vessels below the annual average.

Clean LR2 AG Jubail: The downward trend persists, with vessel count remaining below the annual average of 11 over the last eight weeks.

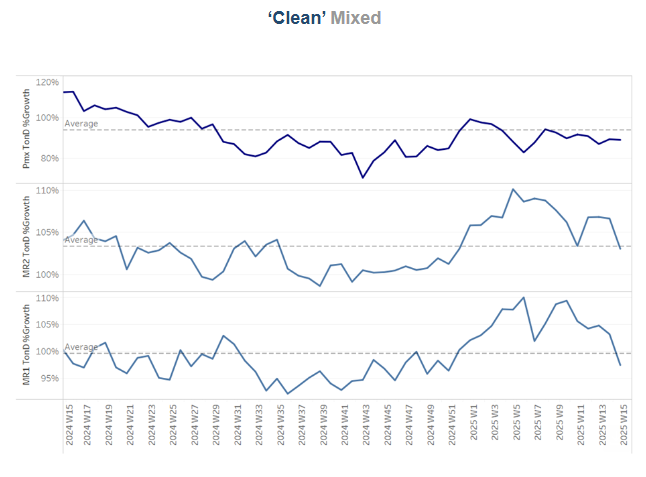

Clean MR: Algeria’s Skikda port has seen a decline in activity, with MR1 vessel calls falling to 26—12 fewer than the peak recorded in Week 8. Meanwhile, MR2 calls in Amsterdam continue to trend upward, currently hovering above the annual average of 32, extending the momentum observed since the end of Week 13.

Dirty tonne days: During the second week of April, the VLCC segment continued its downward trend in tonne-day growth, extending its decline further below the annual average following the last peak observed in week 13. In the Suezmax market, tonne-day growth has now nearly converged with the annual average, indicating a slowdown. In contrast, the Aframax segment shows a notable surge, reaching one of its highest growth levels since the beginning of the year.

Panamax tonne days: The growth rate remains below this year's weekly average, extending a downward trend that has persisted since early March.

MR tonne-days: The MR segment has seen a sustained decline in growth rate since the end of week 5, with the onset of the second quarter further reinforcing this downward momentum.

Data Source: Signal Ocean Platform