Market & Policy Impacts: EU Regulations Reshaping Global Coal Trade

Coal has long been a critical part of Europe’s energy mix, but its role has diminished due to climate policies, the growth of renewables, and shifting economic priorities. The European Union has actively reduced coal consumption as part of broader decarbonization efforts. However, geopolitical factors, energy security concerns, and market demands continue to shape coal use in the region.

EU environmental policies such as the Emissions Trading System (ETS) and the Carbon Border Adjustment Mechanism (CBAM) have increased costs for coal-fired power plants, making coal less competitive compared to gas and renewables. The rising price of carbon allowances has accelerated coal-fired power plant closures and placed long-term pressure on seaborne coal imports. Since its introduction, carbon pricing has surged from around €5–€10/mt in the early 2010s, peaking above €100 in early 2023 before stabilizing at around €65 in 2024—a 35% decline from its peak. Additionally, higher carbon costs have hit industrial users including steel and cement manufacturers, pushing them to seek alternative energy sources or relocate production outside the EU. As a result, coal imports have declined, reshaping trade flows and hitting regional dry bulk shipping, while demand for alternative energy sources continues to grow.

The EU’s Energy Transition: 2018-2024

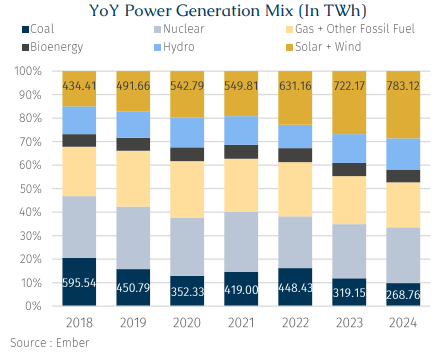

In December 2019, the EU launched its net-zero policy under the European Green Deal, igniting an aggressive push to slash fossil fuel reliance. Coal-fired power generation nosedived from 595.54 TWh in 2018 to 268.76 TWh in 2024—a staggering 55% collapse as the EU’s carbon-cutting drive took full effect. Gas-fired power has followed suit, slipping from 488.95 TWh to 430.02 TWh, with the sharpest fall post-2022 due to soaring gas prices and supply disruptions, as the EU’s reduced reliance on Russian gas led to extreme price volatility, making gas-fired power generation economically unviable.

Furthermore, nuclear energy has faced a rollercoaster ride, tumbling from 761.94 TWh in 2018 to 609.26 TWh in 2022 before rebounding to 648.37 TWh in 2024, reflecting national policies regarding the sector. Similarly, bioenergy generation slipped from 155.46 TWh in 2018 to 150.39 TWh in 2024.

Meanwhile, renewables have come to dominate. Solar and wind generation surged from 434.41 TWh in 2018 to 783.12 TWh in 2024—an 80% increase, driven by record investments, falling costs, and government policies, notably REPowerEU. This initiative accelerated deployment by fast-tracking permits and announcing €30 billion in funding in October 2022, to be invested over five years in scaling up clean energy projects

In 1H24, renewables surpassed fossil fuels in the EU’s electricity mix, with wind and solar overtaking coal. This marks the fourth time renewables have led, following full-year milestones since 2020. However, electricity prices remained a concern. Household electricity prices averaged €29.40 per 100 kWh in early 2023, but then fell to €28.30 later that year, before rising slightly to €28.90 in early 2024. Non-household prices peaked at €21.51 per 100 kWh in early 2023, before dropping to €18.67 by early 2024. Prices have varied widely across the EU, with Germany recording the highest (€41.50 per 100 kWh) prices and Hungary the lowest (€10.90 per 100 kWh), reflecting differing national policies and market dynamics.

While subsidies for renewable energy and grid infrastructure have supported the transition to cleaner power, they have also influenced end-user prices. For instance, Germany's proposed reductions in network fees would cost billions annually, while Sweden's participation in cross-border projects like the Hansa PowerBridge depends on Germany’s electricity market reforms. Additionally, variations in taxation, reliance on imported fuels, and market competition contribute to price disparities among EU nations.

The Steady Decline of Seaborne Coal Arrival in Europe

Since 2018, coal consumption in Europe has been gradually decreasing. According to AXS-Marine data, between 2018 and 2024, coal imports in the EU fell by 53% from 137 mln mt to 63.1 mt, highlighting the effectiveness of these government policies in driving long-term reductions.

However, in 2021, a temporary uptick occurred in arrival of coal shipments, driven by the initial phase of economic recovery from the Covid pandemic, which altered energy demand patterns, and uncertainties in natural gas supply that led EU countries to rely on coal for base load stability. Although it supported short-term coal usage as energy demand surged, coal imports dropped again in 2023, largely due to the energy crisis triggered by the Russia-Ukraine war, which caused soaring fuel prices and accelerated Europe's shift toward wind and solar energy. Nevertheless, variations existed across countries—some replaced coal with increased nuclear or hydro output, while others leaned more heavily on LNG imports or energy efficiency measures.

In 2024, European coal imports continued to decline, falling to 63.1 mln mt. The transition aligns with the EU’s goal of achieving climate neutrality by 2050, with top EU countries already setting Coal phase-out targets within the next decade. This shift is largely driven by the rapid expansion of renewable energy, with wind and solar replacing fossil fuels at an accelerating pace. Investments in clean energy infrastructure and advances in technology have strengthened the transition, reducing the continent’s reliance on coal while ensuring energy security. At the same time, phase-out plans remain broadly on track, with most EU countries continuing to shut down coal-fired power plants and gradually shifting toward alternatives.

Shipping Contraction in the EU Coal Market

In 2024, the Capesize segment saw the largest decline in demand to carry coal into Europe as it dropped by 53% to 18.4 mln tonnes from 39.2 mln mt in 2022. Meanwhile, Panamax shipments declined sharply by 44% to 27.8 mln mt in 2024. The drop was observed across all vessel segments, though the extent varied. aligning with the overall decline in EU coal imports.

The Eurozone has historically relied on coal imports, mainly from Russia, the US, and Australia. In 2024, EU seaborne coal imports recorded a 27% y-o-y decline, driven by a sharp reduction in Russian shipments due to sanctions. As a result, Russian coal shipments to Europe fell by 81% to 3.8 mln mt since 2022.

In contrast, Australian imports remained relatively stable, increasing by a slight 0.6% y-o-y to 18.2 mln tonnes. Meanwhile, the US (16.8 mln mt), Colombia (8.8 mln mt), and South Africa (3.5 mln mt) saw shipments to the EU fall, though the declines were more moderate than in previous years with some support likely coming from these suppliers partially offsetting the loss of Russian coal.

Future Uncertainty – Flip a Coin

If the Ukrainian war was to end in the near future, this would likely lead to another re-drawing of seaborne coal flows. Simply put, sanctions on Russia coal should ease. However, would EU procure some of that coal, partially reinstating pre-2022 trade patterns? Or still baulk at (Russian) coal as it remains unwavering to its green policy despite needing to shoulder both a much heavier defence budget and expensive energy costs while the US simultaneously pivots towards the Indo-Pacific and exits the Paris Agreement. If Russian coal cannot find a home in EU post-war, would China be willing to procure them all (even at heavy discount) when its real estate and deflation-plagued economy is still facing critical hurdles? Meanwhile, India has appetite for seaborne coking coal, not so much for thermal coal.

On the other hand, could Europe liberalise its energy policy and embrace coal in its energy mix to counter ‘Dunkelflaute’, periods of low wind and limited solar power generation? However, with operable coal-fired capacity in western Europe down 30% y-o-y at the end of 2024, and against Argus Media’s projections that this could fall to 38% by end- 2025, the immediate upside to freight will likely be capped.