The Baltic Dry Index gave up Monday’s gains yesterday as the fortunes of the capesizes faded. Still, the panamaxes provided some offset as the segment’s freight indicator recorded a second session of gains. The trading screens for the commodities were dominated by red during yesterday’s session, as concerns over the demand outlook contributed to losses in many cases.

By Ulf Bergman

Macro/Geopolitics

According to data released yesterday, Chinese exports unexpectedly jumped to the highest monthly value since September 2022 amid strong global demand. The year-on-year growth of 8.7 per cent in August beat the consensus projection of 6.5 per cent by a healthy margin and delivered a rare boost for the world’s second-largest economy. However, reflecting continued sluggish demand, imports failed to impress with a year-on-year growth rate of half a per cent, which was well short of the 2.0 per cent expected by the markets. While the better-than-expected exports improved the probability that the country could meet its annual growth target, the weak imports highlighted the continued challenges facing the Chinese economy despite already extensive support measures.

Commodity Markets

After recovering some of the recent losses on Monday, crude oil took another nosedive yesterday as an increasingly weak demand outlook weighed on sentiments. The November Brent futures recorded a daily decline of 3.7 per cent, ending Tuesday’s session at 69.19 dollars per barrel. However, fears that a hurricane will disrupt production and refinery operations in and around the US Gulf have supported prices in today’s session, with the contracts trading around two per cent above yesterday’s close.

European natural gas prices declined sharply yesterday as the stiff headwinds for crude oil weighed on LNG prices. The front-month TTF futures dropped by 5.5 per cent and ended the session at 35.28 euros per MWh, the lowest closing price since the final days of July. The contracts have recovered somewhat in today’s trading, buoyed by higher crude oil prices.

The benchmark futures for the Asian and European coal markets also faced headwinds yesterday amid soft demand. The futures for delivery in Newcastle next month retreaded by 2.0 per cent, settling at 135.60 dollars per tonne. The contracts for delivery in Rotterdam ended the session at 113.15 dollars per tonne, following a daily decline of 1.8 per cent.

Following two consecutive sessions of limited gains, the iron ore futures listed on the SGX faced headwinds yesterday as weaker-than-expected Chinese imports highlighted sluggish domestic demand. The October contracts declined by 1.3 per cent, ending the decision at 90.62 dollars per tonne. However, the contracts have enjoyed a shift in fortunes in today’s trading, with gains of around 2.5 per cent.

The headwinds affecting most commodities yesterday also weighed on the base metals as concerns over the global demand outlook translated into daily losses. The three-month copper futures listed on the LME shed 0.8 per cent, while the aluminium and zinc contracts retreated by around two-thirds of a per cent. The nickel futures delivered the session’s weakest performance amid a daily loss of more than one per cent.

Among the grain and oilseed CBOT futures for delivery towards the end of the year, only wheat avoided the red yesterday. A tightening of global supplies supported the December wheat contracts, which recorded a daily gain of 1.0 per cent. On the other hand, the November soybean futures and the December corn contracts retreated as the supply outlook improved further. The former declined by 2.0 per cent, while the latter shed 0.7 per cent.

Freight and Bunker Markets

After three sessions of gains, the Baltic Dry Index dipped into the red on Tuesday as the freight indicator for the capesizes gave up some of its recent gains. The headline index shed 0.9 per cent yesterday, with the panamaxes offsetting some of the losses in the other segments.

The gauge for the largest vessels fell by 1.8 per cent as tonnage supply increased. The indices for the supramaxes and handysizes retreated by 0.1 and 0.7 per cent, respectively, as demand remained soft. An improving demand situation for the panamaxes supported the segment’s freight index, which advanced by 1.2 per cent.

The Baltic Exchange’s clean and dirty tanker indices maintained the positive momentum that began to build late last week during yesterday’s session. The gauge for the dirty tankers rose by 0.6 per cent, while the indicator for their clean relatives advanced by 2.4 per cent. For the indices for the liquified gas carriers, the day was mixed. The freight gauge for LNG recorded a gain of 1.0 per cent, while the LPG indicator dropped by 2.4 per cent.

Retreating crude oil prices contributed to losses in the bunker fuel trading during yesterday’s session. The VLSFO declined by nearly two per cent in Singapore, Rotterdam and Houston. The MGO faced less resistance across the world’s leading bunker hubs. The latter fuel shed 0.8 per cent in Houston and 0.6 per cent in Rotterdam while retreating only marginally in Singapore.

The View from the Shipfix Desk

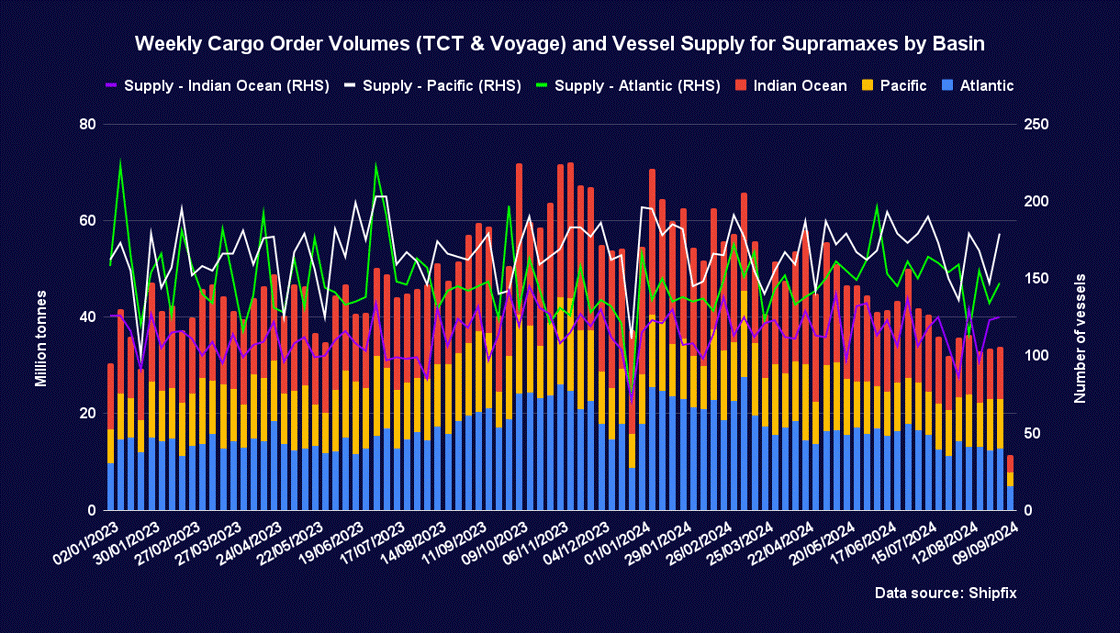

While the Baltic Exchange’s supramax index remained broadly unchanged yesterday, it has been trending lower since the last week of August. As a result, It is currently 3.3 per cent below the level recorded a month ago. Still, despite the recent losses, the gauge is nearly seventeen per cent higher than a year ago.

The past three weeks have seen global spot cargo order volumes under pressure, with all major basins feeling the squeeze. While there has been a marginal recovery over the past few weeks, the average weekly volumes for the past six weeks are 42 per cent lower than during the same period last year. At the same time, the average weekly vessel supply is broadly in line with the levels seen a year ago.

The past week saw cargo order volumes in the three principal basins well below the levels observed at the beginning of September last year. In the Indian Ocean, the weekly aggregate was more than 50 per cent lower than a year ago, while the Atlantic and Pacific basins saw volumes more than 30 per cent below last year's readings for the same period.

The new week has faced a slow start to ordering activities in the supramax segment, with cargo volumes below those of the early stages of last week. At the same time, tonnage supply has been on the rise in recent weeks. Hence, from a demand and supply perspective, a substantial rebound for the supramaxes does not appear to be imminent.

Data Source: Shipfix