The four things investors need to know this week:

Mazars is now Forvis Mazars.

The global economy lacks a clear direction, causing central banks and markets ambiguity

As long as the Fed remains unclear about the potential for further tightening, markets will likely remain nervous.

This market offers very few tactical opportunities, as a lack of clear direction is accompanied by low volatility.

First and foremost, let me share the wonderful news, that this newsletter now comes from a new entity, a global top-ten network, Forvis Mazars, which brings together Mazars and Forvis. You can find out all about it here.

Now to our weekly.

Alcibiades (450-404 BCE), a personal hero, was a student of Socrates. He was also a brilliant general. At age 35, the Athenians elected him to lead a very promising expedition to Sicily. To gain the position, he immersed himself in politics and made a lot of enemies. So, on the night of his departure, his enemies defaced statues of Hermes all over the city and then blamed him. An angry Agora (forum) recalled Alcibiades to be tried for no reason, other than popular wrath. It would be the most consequential decision the Athenian democracy ever made, and the one that led to its downfall. Instead of returning, and facing probable execution, Alcibiades fled to Sparta. The Sicilian campaign failed and the army was captured. From Sparta, Alcibiades instructed Athens’s enemies on how to win the Peloponnesian war. Sparta won, and Athens was humiliated. The Athenian democracy effectively died, arguably by suicide, never to be revived again.

The lesson here? The world is a complex place, which makes it difficult for people to understand their best interests.

Case in point, a recent Bloomberg podcast (you can find it here) suggested that although the US economy is doing better, people don’t ‘feel it’. If anything, middle and lower-income consumers are extremely disappointed. Is it because they lack intellect? No. It is because prices haven’t come down to pre-covid levels.

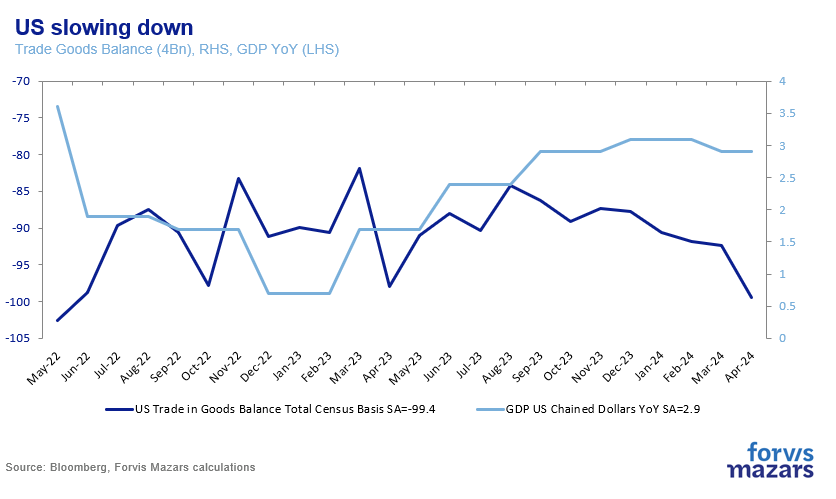

The US economy is doing better, to be sure, but on the margins. There’s no solid economic narrative to support optimism. Making things worse, an election year would tend to polarise people more and skew any objective basis of economic perceptions.

The past couple of weeks have been bereft of direction.

The global economy is dithering. US growth is marginally decelerating, with inflation only very slightly slowing.

Meanwhile in Europe, growth appears to be stabilising, but inflation is rebounding.

As the data dithers, so do data-dependent central banks, and especially the Fed. In the last few days, two key Fed officials (Logan, Kashkari), as well as the FOMC minutes suggested that even rate hikes might be on the table. At the same time, other key officials (Williams, Bostic, Goolsbee) suggested that monetary conditions are tight enough.

To be sure, a two-year inverted yield curve without a recession (but instead above-trend growth), and inflation stuck north of 3% (core PCE around 2.7%) suggests that the Fed may have been too dovish in its approach. Inflation is, of course coming down, but not quickly enough.

A key theme, which we discussed at the time of Jay Powel’s selection is playing out. That when the world’s de facto central bank would need leadership, Mr. Powell w didn’t have the experience and academic background to deliver the extraordinary. Maybe the world is better without the ego of a Greenspan or the singular pursuits of a Bernanke. Central banks handing some power back to democratically elected governments does not sound like a bad idea in principle, even if that transference isn’t 100% voluntary. But it does beg a question: what will be the role of central banks at a time of intensifying trade wars and high debt? Will they observe, will they lead or will they follow? In the next few weeks, we will explore the theme of trade wars and their implications more.

Meanwhile, later in the week, the ECB will likely perform the first rate cut amongst major central banks, but we are still not 100% certain, even with three days to go.

With the economy ambiguous, inflation ambiguous and central banks ambiguous, it is only natural that the stock and bond markets are ambiguous too. The S&P has been trading in a narrow range of 100 points in the past two weeks, and the US 2y Treasury remains shy of the 5% level. As long as the Fed remains unclear about the potential for further tightening, markets will likely remain nervous.

This does not mean that we may not have one of those uncomfortable times when the market moves towards a direction (usually upwards), but in small imperceptible steps. This type of movement usually catches asset allocators off guard, and by the time the bulk of it is complete, many an asset manager have left the possibility of beta-generation (going overweight risk assets) on the table.

So what is the answer?

Do we wait for some meaningful movement from the data? It could take some time, and by the time the data moves, it will be another lost opportunity to generate returns.

Do we take risks with little information in a directionless environment? Not a responsible course of action when one manages client money.

Do we spend time and effort to uncover trends underlying the noise? A better approach, but we need to remember that noise isn’t the problem, as much as lack of direction.

This market offers very few tactical opportunities, as a lack of clear direction is accompanied by low volatility. This means that asset prices would not, even temporarily, fall to a level which would make them attractive. So even if one were to take shorter-term risks, they would likely not be rewarded over a short-term period.

With the risk of sounding like a broken record, we don’t think of investing as making uninformed decisions, especially with other people’s money. Short-term opacity compels asset allocators to fall back towards their strategic allocation, something we have often advocated for. The existence of a strategic asset allocation means that we are never passive viewers of markets. Instead, we rely on the big trends to curry returns.