Strong labour data out of the US pushed rate cut expectations even lower

The European Election confirmed the rise of euro-scepticism, causing elections in France and Belgium and threatening the coalition in Germany.

Europe has been putting off a debate about its future for too long. Markets, who have always been uneasy with the imperfections of the monetary union are looking for answers.

Summary

Last week’s strong US labour data pushed rate cut expectations even further down. Now the Fed is expected to deliver one rate cut by the end of the year. US rate cuts are balancing on a razor’s edge. On the one hand, US manufacturing growth is slowing down. On the other hand, inflation falling has been very much a function of lower prices from China, as the latter tries to snatch manufacturing market share. That disinflationary effect is being fought every step of the way by the US government, who imposes tariffs on China and practices expansionary fiscal policy

Yesterday’s European Parliamentary elections showed that voters are turning increasingly towards euroscepticism, causing elections in France and Belgium and threatening the coalition in Germany. Possible reasons are

A bad economy

The wholesale rejection of multilateralism

Demographics

Lack of interest.

Whatever the case, the need for a post-mortem is dire. Europe has for too long relied on the blueprint of Maastricht, a document in its fourth decade whose inspirers have all passed on. Meanwhile, voters are becoming more disenchanted with it.

Last week’s strong US labour data pushed rate cut expectations even further down. Now the Fed is expected to deliver one rate cut by the end of the year.

US rate cuts are balancing on a razor’s edge. On the one hand, US manufacturing growth is slowing down.

On the other hand, inflation falling has been very much a function of lower prices from China, as the latter tries to snatch manufacturing market share. That disinflationary effect is being fought every step of the way by the US government, which imposes tariffs on China and practices expansionary fiscal policy.

Another week, another piece of data for the inflation/rate jigsaw really. Markets tend to react to this, because this is data they can understand and handle.

But the big news comes from the part investors have always had a difficult time quantifying: Politics.

One of the biggest and most pronounced risks that we have traditionally flagged is that of the Eurozone breakdown. Since its inception, the Eurozone has remained an incomplete monetary union, without a banking union or fiscal transfers. A confederation trying to manage one hard currency and a common interest rate for twenty countries that could not be more different in their economic structure. In the past decade, where the Commission, Europe’s supra-national and de facto governing body, has failed to make decisions, it has relied on the ECB to back European debt and stave off attacks in the bond market.

Yet, it is apparent to the naked eye that the situation is only deteriorating.

Yesterday’s European Parliamentary elections showed that voters are turning increasingly towards euroscepticism. The result was so bad, that it forced Emmanuel Macron, who has been projecting himself as Europe’s leader, to force a snap lower house election, after his party significantly underperformed that of Marin LePen. Belgium also forced a snap election. French stocks were down 2% at the opening, while French banks were down 6%. In Germany, all parties of the ruling coalition of socialists, Greens and Liberal Democrats, failed to secure anything better than third place. The government becomes increasingly shaky.

On paper, the result should not overly worry European leaders. The European Parliament is mostly a symbolic (albeit expensive) function with few real powers. Traditional parties, like the European Popular Party, the Socialist Party and the Greens have more than enough votes to elect a European President to replace Ms Von De Layen, another ceremonial position. European elections are often seen as nothing more than a glorified opinion poll.

Nevertheless, the need for a post-mortem is dire. We are a long way from 1992, the Maastricht Treaty, the last time when Europeans really sat down to discuss what sort of union they wanted. The monetary union was left incomplete, as it was thought that crises would force future European leaders to unite.

In the meantime, Europe adopted a common currency. No one objected to low borrowing rates. So no one wanted to sit down and talk.

Then the Global Financial Crisis happened. Europeans scrambled to save national champions. So no one had time to talk.

Then the Euro crisis happened. It was revealed that Europe was vulnerable to even the solvency problems of one of its smallest economies. Europeans scrambled, but no one wanted to talk, at least about the future.

Then Britain left the Union. Europeans spent a lot of time in anger, but they could still find no time to talk.

Then the pandemic happened. Leaders could hardly meet, let alone find time to talk.

Europe still relies on the blueprint of Maastricht, a document in its fourth decade whose inspirers have all passed on. Meanwhile, voters are becoming more disenchanted with it.

What does the future hold? Are we sleepwalking towards a Eurozone breakup, an event that, in my humble opinion, would likely dwarf the GFC?

The answer is: “we don’t know. We need to ask”. Why did last night’s vote bring forward so many Eurosceptics?

One likely answer is the economy. Slowing growth and high supermarket prices, in conjunction with the non-critical nature of the election, can easily turn the European parliament vote into a protest vote. “All politics is local” Tip O’Neil, a former US speaker exclaimed in 1932. It holds true, even for Europe.

If that is the case, then in five years we should expect a simple mean reversion towards political realism.

Yet I am not convinced. Inflation tends to be a big political issue and has brought down many a government, to be sure. But Europe has always been seen as a solution to economic troubles, not an originator. A disunited Europe would be significantly more inflationary for most countries.

Another likely answer is the wholesale rejection of bureaucratic multilateralism. A trend we have seen in the US, in the UK and in many European countries. People often don’t see the point in more trade treaties, especially as results take a long time to show.

But I think that’s still not the whole story. Trade tends to enrich people, not impoverish them, a fact well-known since antiquity. Distrust of multilateral, unelected institutions is, of course, a trope. But one can’t wonder why this distrust never extended to central banks, who hold real power, or other similar institutions.

A third answer is demographics. What do Marine LePen’s National Front, Italy’s ruling party and Germany’s AfD, now the second biggest party, last night’s winners all have in common? An anti-immigration agenda.

As I spent the morning wondering what the meaning of it all was, I turned to the upcoming British election.

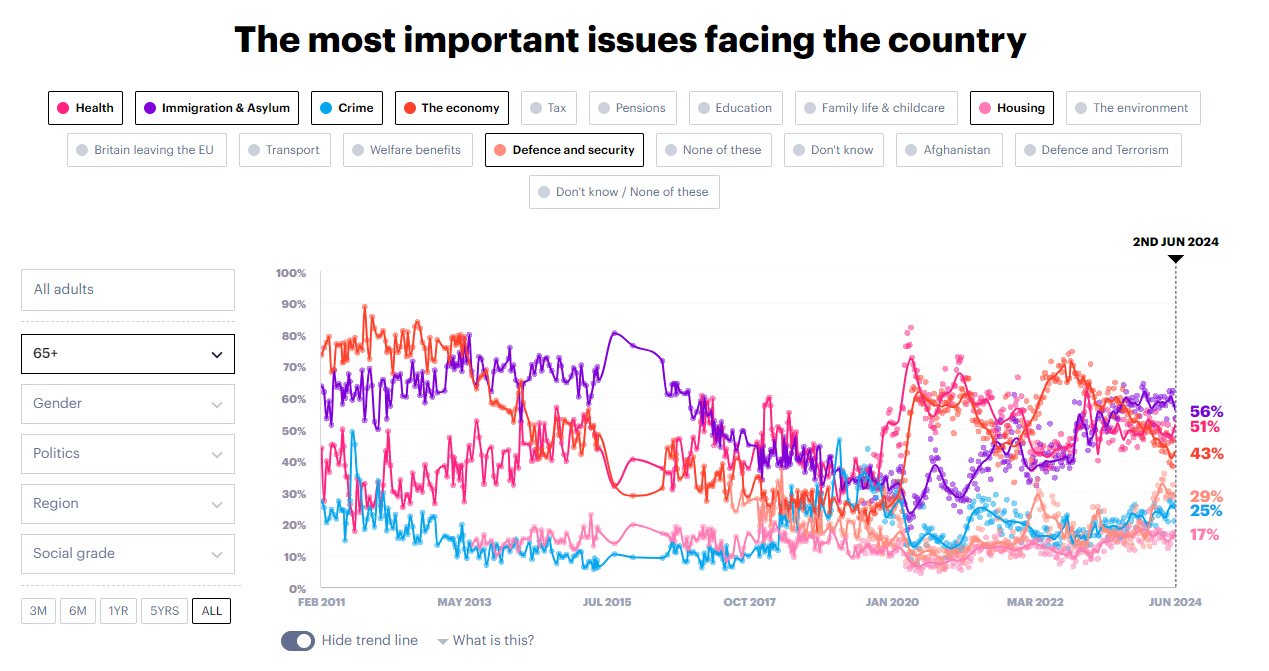

During the Brexit referendum, the issue that was most important to people, by far, was immigration. However, once people got what they voted for, control of the borders, they turned towards other issues, like the economy and health.

For voters over 65, however, according to YouGov, immigration remains a top issue, along with Health.

So another answer to what happened yesterday is, possibly, by and large, demographics. An ageing population, more conservative in nature, has a bigger sway in the electorate than ever before. Baby boomers not only hold a significant amount of wealth in savings, curbing growth as that money could have been invested, but they are a potent political force.

It makes perfect sense. Multilateralism, experimentation, technology, and cultural integration are a young person’s game. Older generations tend to be more conservative. And this generation of baby boomers has never shied from politics.

So what is the answer to that particular problem? Do countries dismiss an ageing demographic as irrelevant and move on? Even if we want, democracy doesn’t give us the right to do so. Do they yield and wait for that demographic to naturally shrink? The economic repercussions could be significant.

“Demographics are destiny” Auguste Comte, a French nineteenth-century philosopher said. The West’s economic and political problems are very much a function of its demographic make-up. Given Europe’s fragility, due to the common currency, its particular convulsions could reverberate across all the global economy, and the financial world.

A fourth and final case is simply that the European Election doesn’t matter enough for voters, who either ignore it (50% participation), or they use it as an internal tool to send messages to their governments.

Whatever the answer, a deep Maastricht-like discussion is way past due.

Yesterday’s result is another wake-up call for Europeans. Investors are watching. They have never been overly comfortable with the Eurozone’s set up. Weak governments and rising Euro-scepticism probably add on those worries. It may not take much to challenge the ECB’s resolve. The longer Europe doesn’t talk about its problems, the higher the risks for all stakeholders.