Looking ahead, recent high-frequency indicators suggest that the recovery of global trade has persisted into early 2024, albeit with fragility and a strong reliance on the performance of key economies such as the United States and China.

The first trading week of May a couple of years ago was a rather choppy one, with Federal Reserve making headlines. In fact, Fed raised the target for the Fed Funds Rate by half a point to 0.75-1 percent - aiming to tackle soaring inflation. It was the first time in 22 years that the central bank had hiked rates up this much. In his postmeeting press conference, Fed Chairman Jerome Powell stressed that additional half-percentage-point rate hikes would be on the table for the next few meetings, after acknowledging that inflation is much too high. Two years later, the Federal Reserve has signalled this week that US borrowing costs are likely to remain higher for longer, as it wrestles with persistent inflation across the world’s biggest economy. Tighter monetary conditions are still exerting pressure, particularly in housing and credit markets, yet global economic activity is displaying resilience.

In light of the current global economic landscape, while growth remains modest, there are encouraging signs of a brighter outlook, as highlighted in the latest OECD Economic Outlook. Notably, inflation is declining at a faster pace than initially anticipated, accompanied by a marked increase in private sector confidence. Furthermore, labor market imbalances are gradually easing, with unemployment persisting at or near record lows, and real incomes starting to ascend amidst moderating inflation. Moreover, trade growth has shifted towards positive territory. Nevertheless, significant divergences persist among countries, with softer economic performances observed in Europe and many low-income nations, juxtaposed with robust growth in the United States and several major emergingmarket economies.

According to its latest economic outlook report, the Organisation for Economic Cooperation and Development (OECD) forecasts that global economic growth will hold steady at 3.1 percent this year and accelerate to 3.2 percent in 2025. This marks an upward revision from the OECD's February projections, which anticipated growth of 2.9 percent for this year and 3 percent for 2025. Headline inflation experienced a rapid decline across most economies in 2023, attributed to restrictive monetary policies, lower energy prices, and alleviation of supply chain pressures. In addition to positive global economic growth, the report anticipates a decrease in headline inflation to 5.03 percent in 2024 and further to 3.43 percent in 2025. Core inflation is also expected to decrease, reaching 5.25 percent in 2024 and aligning with headline inflation at 3.43 percent in 2025. The projected continuous decline in both headline and core inflation should pave the way for central banks in many economies to initiate policy rate reductions this year, although real rates are anticipated to remain restrictive, surpassing estimated neutral levels for some time. Simultaneously, fiscal policy is projected to undergo modest tightening in most OECD countries, contributing to an overall restrictive macroeconomic policy stance.

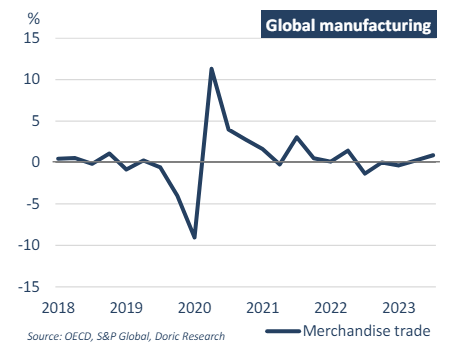

Regarding international trade, annual volume growth decelerated markedly in 2023 to 1 percent, following a robust increase of 5.3 percent in 2022. Inventory reductions and a shift in consumption towards less trade-intensive services were key contributors to the slowdown, notably in the United States and Europe. Import volumes in the United States contracted by 1.7 percent in 2023, after experiencing growth of 8.6 percent in 2022, thereby significantly dampening export growth among trading partners. China stood out as a notable exception to this global trend, as reopening efforts bolstered trade growth following a decline in 2022. This helped cushion the moderation in external demand for many other emerging-market economies. The fourth quarter of 2023 saw a rebound in aggregate global trade growth, driven by robust growth in China, Korea, and the United States, despite enduring weakness in Europe. Overall, while 2023 saw a marked deceleration in international trade growth compared to the previous year, the rebound in certain key economies helped mitigate the slowdown and contributed to a modest recovery in the fourth quarter.

Looking ahead, recent high-frequency indicators suggest that the recovery of global trade has persisted into early 2024, albeit with fragility and a strong reliance on the performance of key economies such as the United States and China, as outlined by the OECD. Echoing this sentiment, economists from the World Trade Organization emphasized last month that global goods trade is poised to gradually rebound this year. Projections indicate that the volume of world merchandise trade will increase by 2.6 percent in 2024, followed by a further acceleration to 3.3 percent in 2025, following the contraction in 2023. These forecasts offer cautious optimism regarding the path of global trade recovery over the upcoming years. However, uncertainties persist, particularly concerning factors such as energy prices, inflationary pressures, and geopolitical dynamics, which could shape the pace and direction of trade growth.

Data source: Doric