The Baltic Dry Index retreated by nearly two per cent yesterday, extending losses into a fourth consecutive session. Continued weak demand in the capesize segment provided most of the downward pressure, while the supramaxes delivered some limited offset. Among the commodities, most ended the day in the black as a combination of more robust demand and supply restrictions contributed to higher prices.

By Ulf Bergman

Macro/Geopolitics

Yesterday’s batch of US economic data did not exactly help anyone looking to predict the timing of the Federal Reserve’s first interest rate cut in the current cycle. On the one hand, growth during the first quarter failed to match expectations, with an actual quarterly expansion of 1.6 per cent rather than the 2.5 per cent projected by market consensus. While the weaker-than-expected could be supportive of an early interest rate cut, a second release of economic data highlighted continued elevated inflation in the world’s largest economy. The latter data set offset the weaker growth and provided some support for the narrative that US interest rates may remain higher for longer, with some traders now expecting the first cut to take place in December.

Commodity Markets

Crude oil gained yesterday as the demand outlook remained bullish following suggestions by the US Treasury Secretary that the first quarter GDP may be revised upwards in the coming month. The June Brent futures ended Thursday’s session a shade above 89 dollars per barrel, following a 1.1 per cent gain for the day. The contracts have continued to rise in today’s trading amid gains of around half a per cent.

Supply disruptions pushed European natural gas prices higher for a second session on Thursday. The front-month TTF futures recorded a daily gain of 2.6 per cent as they ended the day at 29.77 euros per MWh. The contracts initially gained in today’s trading but have since retreated into the negative territory amid losses of around one per cent.

After several days of losses, the coal futures for the European and Asian markets staged a modest rebound yesterday. The contracts for delivery in the port of Newcastle in May edged up by 0.2 per cent, ending the day at 135.75 dollars per tonne. The front-month futures for delivery in Rotterdam rose 0.7 per cent, settling at 111.85 dollars per tonne.

Following two sessions of significant price swings, iron ore stabilised yesterday. The May futures listed on the SGX recorded a marginal daily loss and settled at 117.84 dollars per tonne. Today’s session has seen a small improvement in sentiments, with the contracts gaining a fraction of a per cent.

Continued concerns over tighter global supplies contributed to gains for most base metals yesterday. The three-month copper futures listed on the LME ended the day 0.9 per cent higher, while the zinc and nickel contracts advanced by 1.5 and 1.1 per cent, respectively. However, the aluminium futures went against the flow and ended the session with a 1.5 per cent loss.

Dry weather across parts of the US continued to support wheat prices yesterday. The May futures listed on the CBOT rose by 1.3 per cent, extending the recent winning streak into a fifth session. The corn contracts advanced by 0.7 per cent, while the soybean futures shed a third of a per cent.

Freight and Bunker Markets

Most of the Baltic Exchange’s dry bulk indices retreated yesterday, contributing to the Baltic Dry Index declining for a fourth consecutive session. The headline indicator shed 1.7 per cent, with the capesizes continuing to provide most of the downward pressure. The sub-index for the largest vessels dropped by 4.9 per cent as cargo order volumes remained weak. The gauges for the panamaxes and the handysizes shed 0.7 and 0.1 per cent, respectively. The supramaxes stood out from the crowd, with their freight index rising by 2.2 per cent amid robust demand in the Indian Ocean and the Pacific.

The Baltic Exchange’s wet freight indices had another session of relatively minor changes on Thursday. The gauge for the dirty tankers edged up by 0.4 per cent, while the clean tankers saw their indicator shed 0.8 per cent. The spot indicator for the LPG carriers advanced by 1.3 per cent, but the gauge for the LNG tankers remained unchanged for a second day.

Despite rising crude oil prices, the trading in VLSFO and MGO experienced diverging fortunes yesterday. The VLSFO recorded modest gains across the world’s leading ports, with Houston leading the way with a 0.8 per cent gain. In Singapore and Rotterdam, the fuel only recorded marginal gains. On the other hand, the MGO retreated by 0.8 per cent in Rotterdam and by 0.4 per cent in Houston. Still, in Singapore, the latter fuel rose by 1.1 per cent.

The View from the Shipfix Desk

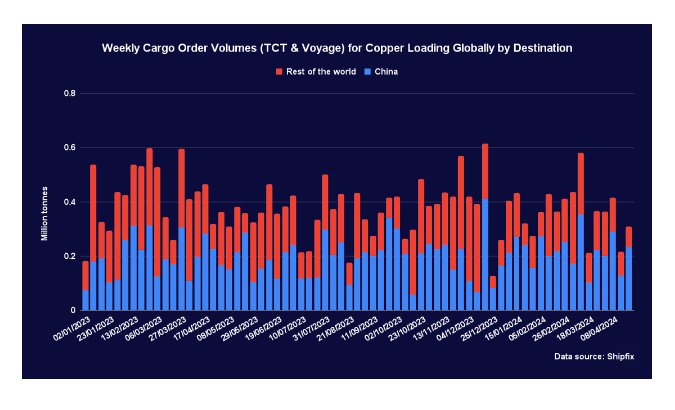

Since early February, copper prices have advanced by around twenty per cent and reached the highest levels in over two years. Robust demand as the energy transition gathers momentum globally has supported the higher prices. At the same time, concerns have been growing that global supplies will be insufficient to cover future demand levels. Hence, in the long run, copper prices can be expected to rise further.

However, copper prices may stabilise in the short term after substantial gains in the past months. While cargo order volumes for copper loading globally have staged a rebound this week, recent demand for seaborne transportation of copper concentrate has been under some pressure. The total for the current month is on course for a ten to fifteen per cent decline compared to March, suggesting softer demand for the red metal, especially outside China.

Still, demand from Chinese buyers remains stable, with volumes broadly in line with the past few months. Also, cargo order volumes for discharge in Chinese ports are higher than during the same month last year. As copper demand is often seen as a bellwether for economic activity, more robust demand for the metal in China could herald a period of improvement for the world’s second-largest economy. Should such a development materialise, it would support Chinese demand for other commodities but could also weigh on Chinese steel exports.

Data Source: Shipfix