In the current economic landscape, the International Monetary Fund has emphasized that geoeconomic fragmentation could exert pressure on global trade and income growth in the forthcoming years.

Throughout history, some things have undergone rapid change while others have remained steadfast. Remarkably, the sixteenth trading week opened with a decline in oil prices on Monday following Iran's weekend attack on Israel. Just a few years ago, such an event would have had significant repercussions not only on oil prices but also on the global economy as a whole. Oil benchmarks had surged on Friday in anticipation of Iran's retaliatory strike, reaching their highest levels since October. However, Israel's interception of Iran's attack eased concerns of a regional conflict disrupting oil traffic through the Middle East. Additionally, Iran's declaration that it considers its retaliation to be concluded has further tempered geopolitical tensions. In the midst of this, China prepares for another escalation in the trade war as tensions rise following the US's proposal of tariffs on metals. President Biden advocated for tripling import tariffs on Chinese steel and aluminum on Wednesday during his re-election campaign in Pittsburgh, a city once revered as the heart of the American steel industry. Analysts predict Beijing will respond with retaliatory measures, signaling the onset of a fresh trade battleground between the globe's two largest economies.

In this economic landscape, the International Monetary Fund has emphasized that geoeconomic fragmentation could exert pressure on global trade and income growth in the forthcoming years. Data reflecting bilateral goods trade before and after Russia’s invasion of Ukraine substantiate that fragmentation is already in progress. Trade among economies situated in politically distant blocs has decelerated more noticeably than trade among those within blocs. Another facet of this fragmentation is the weakening trade ties between China and the United States. Since the initiation of trade tensions between China and the US in 2017, accompanied by escalating tariffs on bilateral trade, China’s portion of US goods imports has diminished by nearly 8 percentage points. Concurrently, there is evidence suggesting that US sourcing has been partially redirected away from China and towards other nations during the period spanning 2017 to 2022, including Mexico and Vietnam.

World trade growth, overall, is forecasted to reach 3.0 percent in 2024 and 3.3 percent in 2025, marking a downward revision of 0.3 percentage points for both years compared to the projections made in January 2024. This trajectory indicates that trade expansion will persist below its historical annual average growth rate of 4.9 percent over the medium term. Against the backdrop of a relatively subdued economic growth outlook, this projection suggests that the ratio of total world trade to GDP (in current dollars) will average around 57 percent over the next five years. This figure aligns broadly with the trend observed in trade since the global financial crisis. Moreover, the medium-term growth outlook is at its lowest in decades, projected at just 3.1 percent in 2029.

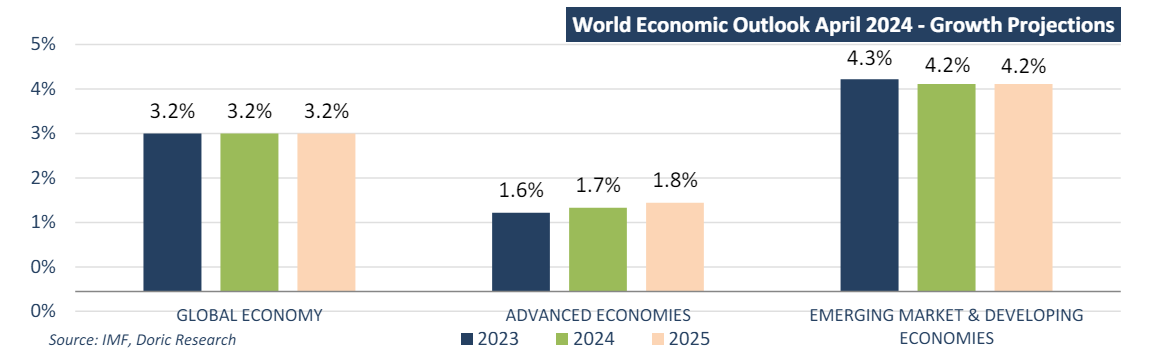

Putting aside the medium-term trends, the global economy has demonstrated remarkable resilience thus far, with growth maintaining stability as inflation gradually returns to target levels, as reported by the Fund. Despite earlier concerns of stagflation and global recession, economic activity has continued to grow steadily as global inflation receded from its mid-2022 peak. Global growth, estimated at 3.2 percent in 2023, is forecasted to persist at the same pace throughout 2024 and 2025. The projection for 2024 has been revised upward by 0.1 percentage point from the January 2024 World Economic Outlook (WEO) Update and by 0.3 percentage points from the October 2023 WEO. Global headline inflation is anticipated to decline from an annual average of 6.8 percent in 2023 to 5.9 percent in 2024 and further to 4.5 percent in 2025, with advanced economies expected to return to their inflation targets sooner than emerging market and developing economies.

In advanced economies, growth is set to rise from 1.6 percent in 2023 to 1.7 percent in 2024 and 1.8 percent in 2025. The projection for 2024 sees a 0.2 percentage point upward revision compared to the January 2024 WEO Update, while it remains steady for 2025. This adjustment for 2024 is driven by an upward revision to US growth, offsetting a similar downward revision to the euro area in 2025. Meanwhile, emerging market and developing economies are expected to maintain stable growth at 4.2 percent in both 2024 and 2025. This stability is achieved despite a moderation in emerging and developing Asia, balanced by increasing growth for economies in the Middle East and Central Asia. Within this group, China's growth is forecasted to slow from 5.2 percent in 2023 to 4.6 percent in 2024 and 4.1 percent in 2025. This deceleration reflects the diminishing impact of one-off factors like the post-pandemic consumption boost and fiscal stimulus, alongside persisting weakness in the property sector. In contrast, India is poised for robust growth at 6.8 percent in 2024 and 6.5 percent in 2025, driven by sustained domestic demand and a growing working-age population.

The sixteenth trading week wrapped up today with oil prices slipping, following an earlier spike of more than $3, after Iran downplayed reported Israeli attacks on its soil, signaling a potential de-escalation of hostilities in the Middle East. Baltic indices, on the other hand, trended upwards, with all segments reporting weekly gains.

Data source: Doric