With trade data sending mixed signals, Baltic indices have recently reached a certain plateau, lingering well below and slightly under their recent highs for the gearless and geared segments respectively

China's March exports and imports fell short of expectations by a considerable margin, underscoring challenges for the world's secondlargest economy. Exports experienced a sharp contraction, while imports unexpectedly declined, with both registering only a modest 1.5 percent year-on-year increase in the first quarter. Chinese exporters grappled with difficulties throughout the previous year, with the impact of soaring interest rates on overseas demand having a negative bearing.

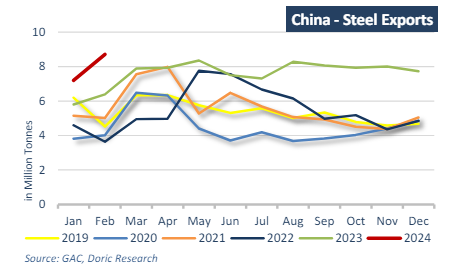

In March, exports from China plummeted by 7.5 percent year-onyear in value, as reported by today's customs data, marking the most substantial decline since August of the previous year. This sharp decrease sharply contrasts with the forecasted 2.3 percent decline in a Reuters poll of economists. The fall in exports can be attributed to declining values rather than surging volumes. Overcapacity in certain sectors, particularly those favored by industrial policies such as electric vehicles and solar panels, has negatively impacted exporting prices. This trend of oversupply, coupled with accusations from the US and Europe of dumping artificially cheap goods on international markets, raises concerns about China's industrial practices. Despite the overall weakening of exports last month, steel shipments reached their highest levels since July 2016, surging by 30.7 percent in the first quarter. March, in particular, witnessed a significant increase in China's exports of steel products, up by 25.35 percent year-on-year to 9.89 million tonnes. This volume brings the total for the first quarter to an eight-year high of 25.8 million tonnes.

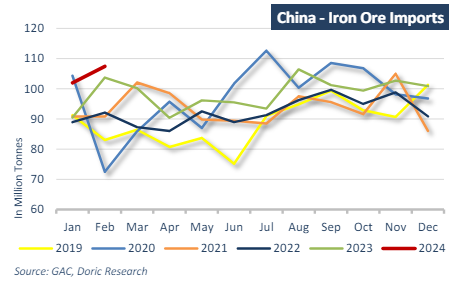

Imports for March also remained subdued, declining by 1.9 percent year-on-year and falling short of the expected 1.4 percent rise. This weak performance reflects lethargic domestic demand, a sentiment echoed by Thursday's data indicating a more significant than anticipated cooling of consumer inflation and persistent factory-gate deflation. Shifting focus to dry bulk commodities, China's iron ore imports in March saw a marginal increase of just 0.5 percent from a year earlier, reaching 100.72 million metric tonnes. There were high hopes for demand to bounce back following the Lunar New Year holiday break, a period typically characterized by increased production by steelmakers. However, last month's demand failed to meet expectations, resulting in an accumulation of portside stocks and a notable decline in prices. According to customs data, in the first quarter of 2024, the world’s largest iron ore importer brought in 310.13 million tonnes, marking a 5.5 percent increase from the previous year.

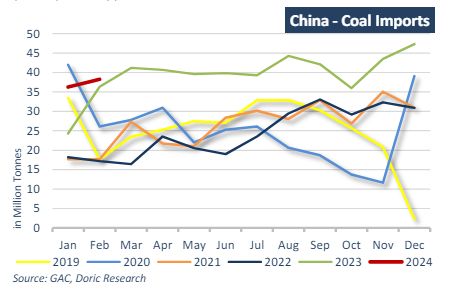

In relation to the less favored commodity, coal imports in March remained almost unchanged year-on-year, as weak demand and decreasing domestic prices put pressure on international shipments. China imported 41.38 million metric tonnes of coal in March, a slight increase compared to the same period a year earlier, as reported by General Administration of Customs data. However, first-quarter coal imports surged by 13.9 percent to reach 115.9 million tonnes, propelled by a 23 percent year-on-year increase in January-February imports. Indonesia, Australia, Mongolia, and Russia stand as the primary coal suppliers to China.

In a notable departure, soybean imports in March plummeted to a four-year low due to high prices and unfavorable hog margins, dissuading crushing for feed consumption. Total imports for the month amounted to 5.54 million metric tonnes, nearly 20 percent lower than the same period last year. Soybean arrivals in JanuaryMarch totaled 18.58 million tonnes, reflecting a 10.8 percent decline from the same quarter last year and marking the lowest first-quarter import figure since 2020. Looking forward, soybean imports are anticipated to pick up in the second quarter post the harvest season in Brazil. However, this growth might be restrained by subdued feed demand in the key Chinese market.

China's economy has indeed set out on a relatively robust trajectory this year, thanks to the implementation of support measures by policymakers in the latter half of 2023 aimed at revitalizing household consumption, private investment, and market confidence. This positive trend is evident in the performance of the Baltic Dry Indices during the first quarter. However, growth in the Asian powerhouse remains uneven, and the majority of analysts do not anticipate a comprehensive resurgence in the near future. Against this backdrop, and with trade data sending mixed signals, Baltic indices have recently reached a certain plateau, lingering well below and slightly under their recent highs for the gearless and geared segments respectively.

Data source: Doric