This week, in the East, we discuss falling VLCC average voyage mileage and the outlook for MEG LR freight rates. Over in the West, we focus on the changing fortunes of Aframaxes in the Atlantic Basin, and we examine why TC2 is failing to ignite despite vessel supply constraints.

By Mary Melton

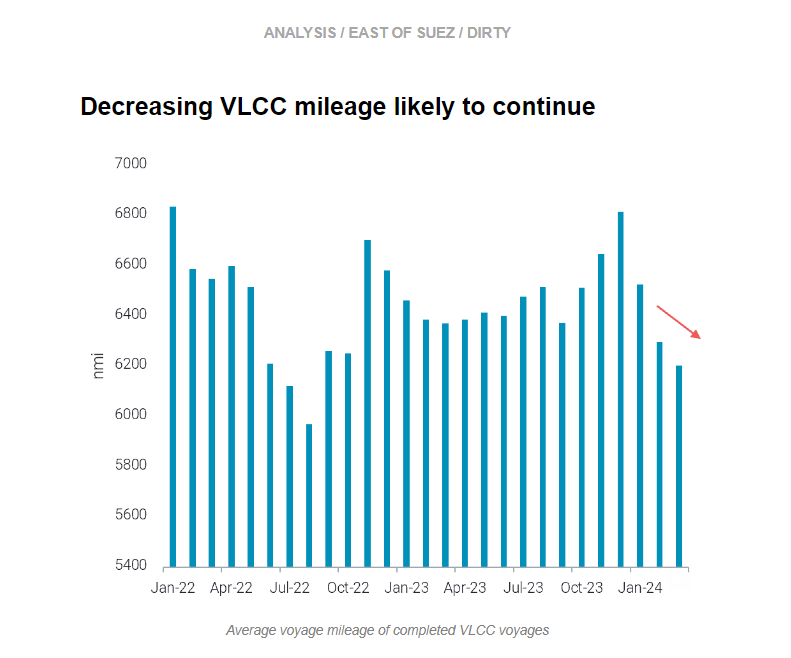

VLCCs are travelling shorter distances as a result of less Atlantic Basin crudes going to Northeast Asia. Through March, average voyage mileage for completed voyages on VLCCs fell for the third month in a row.

Mileage declines are likely to continue in April, because the number of total VLCC departures out of the Atlantic Basin to Northeast Asia fell slightly m-o-m, which is more significant when considering February had two fewer days than March.

At the same time, China is increasing its exposure to Middle East crudes. Departures to China of mainstream MEG crude grades (excl. Iran) increased 15% m-o-m in March, increasing shorter-haul VLCC voyages. This was driven by lower than expected Saudi OSPs, but China’s exposure to other mainstream MEG crudes (incl. Iraq and Oman) also increased m-o-m.

LR voyages on a departures basis reached an all-time high in March. Record-setting utilisation on the Pacific Basin-to-Europe route - which includes the Cape of Good Hope rerouting – is boosting tonne-miles and keeping freight rates volatile.

In the run up to the Eid holiday in the last few weeks, there were higher intra-Saudi and intra-Middle East flows on LRs. These flows have decreased so far in April, and fixing activity has declined now that the pre-holiday rush is over. As a result, LR freight rates in the region (TC1, TC5, TC8) are under pressure from reduced demand and high prompt vessel supply.

Moving forward, weakening naphtha margins in Northeast Asia means demand on TC1 and TC5 is unlikely to revive and alleviate some of the tonnage build-up. However, long voyages for middle distillates MEG-to-Europe - which are currently supported by a slightly open arbitrage - could continue to keep LR demand elevated.

According to our Aframax freight basket, freight rates are currently below 2023 averages. This is partially due to increased vessel supply in mainstream trade as increased sanctions enforcement sent tonnage from the Russian trade back to other markets. However, the main factor contributing to the recent downturn in Aframax rates is less tanker demand on the transatlantic route USG-to-Europe.

Utilisation on this route reached a 10-month low in March 2024 because of a few factors. The end of US refinery maintenance means more domestic crude consumption, and European demand for WTI is reduced due to its higher crude stocks and refinery maintenance. At the same time, Europe has imported more sour crude from the Middle East, and these voyages have been realised on Suezmaxes.

In the short-term, it is unlikely that Aframax employment will pick up on the US-to-Europe route, as a widening spread between Aframax and Suezmax rates (source: Argus) will prompt charterers to fix on Suezmaxes. For more about the outlook for Aframax rates read our latest insight (here).

The upside for TC2 rates is currently capped by narrow transatlantic arbitrage opportunities. European gasoline prices remain relatively high and have kept a lid on transatlantic gasoline exports, even with the expected seasonal peak in US gasoline demand around the corner.

The lower freight rates have led to a combination of a lack of MR2 vessels ballasting into Wider Northwest Europe (WNWE), along with limited ballast tonnage (monthly average) already in the region, which is constraining the overall fleet supply for gasoline exports from the region.

The vessels already in the region are seeking opportunities elsewhere, with voyage counts from WNWE to the Wider Mediterranean rising.

Data Source: Vortexa