By Daniel Hynes

A risk off tone across markets weighed on sentiment across commodities, compounded by further economic weakness in China.

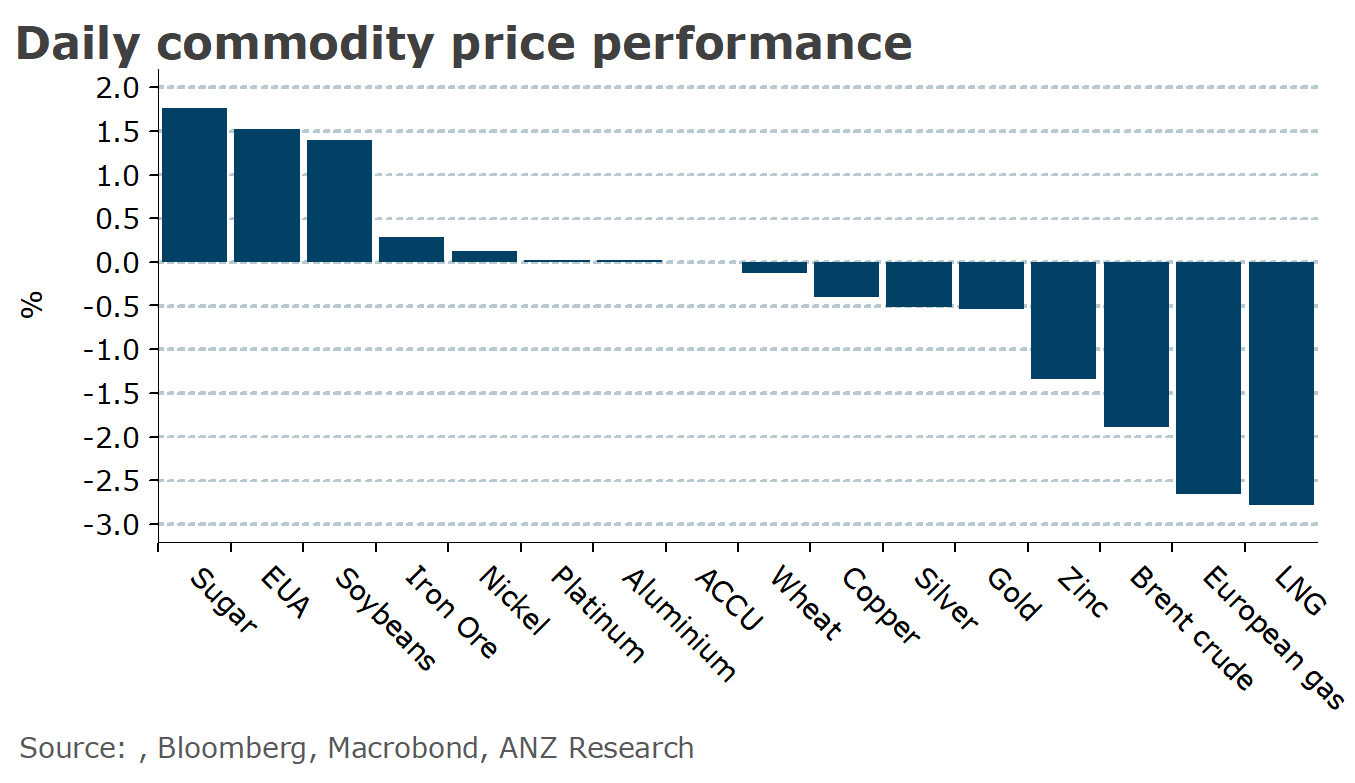

A lack of liquidity left crude oil at the mercy of broader market moves. A selloff across equity markets triggered a risk-off tone across the energy sector. Sentiment wasn’t helped by signs of further monetary tightening by central banks. FOMC minutes showed most officials noted significant upside to inflation means we may see more tightening. The market also shrugged off another large drawdown in inventories. US commercial crude oil stockpiles fell 5,960kbbl last week, according to EIA data. The only blight in the EIA weekly report was a fall in implied gasoline demand, which dropped 451kb/d to 8.85mb/d. Nevertheless, signs of tightness in the physical market continue. Strong demand continues to drive up premiums. Differentials for spot cargo from the Middle East have surged in recent days amid strong buying from China. Asian refineries are also snapping up all available cargo from the North Sea.

The recent rally across gas markets paused as traders await the outcome of labour negotiations in Australia. European gas edged lower, paring some of the gains achieved this week. This was matched by a similar fall in North Asian LNG prices. A new round of talks between Woodside and union officials is expected on 23 August. This helped cool some market jitters which, earlier in the week, sparked a rush for available cargo on the spot market. A ballot of workers at Chevron’s Gorgon and Wheatstone facilities must be completed by 24 August. The relatively full storage facilities in Europe also helped eased concerns of supply shortages. Gas Infrastructure Europe data shows they are about to reach 90% capacity. Nevertheless, any disruption to LNG supplies from these facilities will likely cause gas prices to surge higher.

Copper inched lower, while other base metals struggled to stay above water amid signs of stress in China’s property sector. New home prices in 70 cities fell 0.23% m/m in July. This is likely to keep pressure on property developers, including Country Garden Holdings, which faces a potential default after missing bond payments earlier this month. Iron ore futures were also under pressure in early trading. The prospect of curbs on Chinese steel also weighed on sentiment. Plants in Jiangsu are reporting they have reduced steel production by 20-30% from H1 levels, according to a report by Mysteel. There have also been media reports that the National Development and Reform Commission has communicated with provincial governments on enforcing steel supply cuts.

Gold dropped below USD1,900/oz after the release of the FOMC’s Minutes. The prospect of further rate hikes saw the USD push to a two-month high, denting investor demand for the precious metal. Better than expected economic data has also weighed on safe haven demand.

Data source: Commodities Wrap