The three things I would tell my clients this morning

This is a very idiosyncratic world. As politicians diverge and compete, so do economies and so will policies. One may expect the Fed to cut rates, but Europe is still facing an uphill battle in terms of inflation, which is now stickier.

Idiosyncrasies will lead to lower growth and productivity and higher inflation.

Idiosyncrasies will also change the way we allocate assets. Returns will now come from the bottom up (security selection à industry selection à region à broader asset allocation) which constitutes a big departure from the QE era. Selecting the best security pickers could be the key to unlocking portfolio performance in the near future.

In this first email of the Carolingian era for the United Kingdom, one can’t but reflect on the symbolisms projected by the glorious anachronism that was the new British Sovereign’s coronation. Charles III has, by all accounts, been outspoken about things that interest him such as the natural and built environment. Even if we forget all the press clippings of the past 50-odd years, the choice of the name itself is telling of the idiosyncratic nature of the new monarch.

Once ascending to the throne, sovereigns sometimes change their names for good fortune and to convey a sense of continuity. His grandfather was called Albert, but became George VI. His uncle was known as David, but took the name Edward VIII. “Charles” was an admittedly peculiar choice. Charles I was decapitated for the grave offence of causing civil war, and, yet graver, losing it. Charles II spent most of his life in exile and died childless, leaving a collapsing throne to his brother James II who ended the Stuart dynasty. Charles Philip Arthur George of the House of Windsor, former Prince of Wales and present Sovereign, could have chosen any of the three other less ominous names at his disposal, other than Charles III. But in doing so he made a statement: that for the remainder of his life he would do things his -idiosyncratic- way.

For us who were born overseas, the UK itself is as idiosyncratic as its new Sovereign. The architecture, customs, everyday habits, the constraints of conversation could not be farther from continental Europe. Seen just from the vantage point of culture, Brexit, made absolute sense.

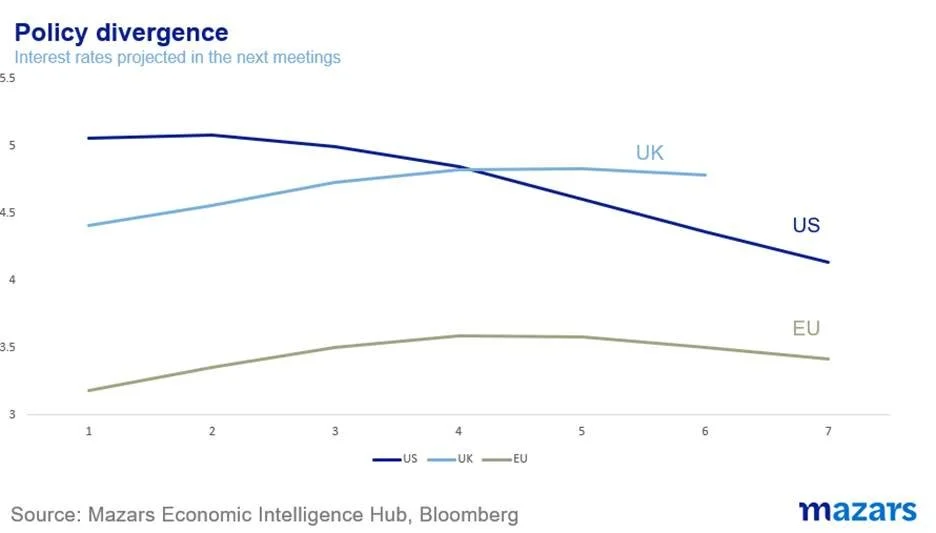

Britain’s largest problem is not its own idiosyncrasies. Rather it’s that the world itself is becoming more idiosyncratic. The US has embraced an “America First” policy for the second successive President. The Inflation Reduction Act, a euphemism for protectionism, is luring industries to the US[1] promising nearly half a trillion in subsidies. China is also acting unilaterally, scaling back its market reforms[2] and antagonising America for global and regional influence.

The post-Soviet order lies in tatters, and the world is becoming more disjoined by the month. The policy divergence has a profound impact on economics. Inflation globally is diverging.

Those who think this is simply a matter of Europe running a few months behind the US, should think again. European growth is slower, and the labour market is tighter and more sclerotic. As a result, where Americans see wage growth falling, Europeans see much stickier wage inflation.

And different inflation means significant policy divergence.

Which in turn means economic divergence, supply chain divergence and, in all probability, economies underperforming their potential (larger output gaps).

This is Entropy at its finest. The Second Law of Thermodynamics states, in essence, that all systems have a much higher chance of being in disarray than operating efficiently. And even when they do work, they are eventually likely to stop working.

We are living in such a world. In this world, “idiosyncratic” is the norm rather than the exception. This has implications for many asset classes and many asset managers. And, unbelievably, the implications are mostly good.

Back in the day of Quantitative Easing, when the Fed was printing trillions on the slightest sight of market volatility, money was made by choosing the correct asset class (equities over bonds), then the correct region (the one that printed the most and where the printed money eventually ended up), then by choosing the correct industry (tech) and then by choosing the right securities.

The opposite now stands. In this world where central authorities break traditional trade bonds, to find winners we need to look at companies first, then sectors. Regions, which antagonise each other, are third, and top-level asset allocation is last. What does this mean in practice? That it’s no longer just about choosing equities over bonds, but rather about choosing the right sub-asset class (for example US Mid Caps vs UK Large Caps) or the right industry or the exact right stock.

This is a world for the best security pickers to get their day in the sun, and the best asset allocators to think as broadly as they hadn’t had to for fourteen years. Choosing the right securities, or the right security pickers, will be paramount for portfolio returns.

All those who would see King Charles’s coronation as archaic theatre, irrelevant to the modern world, should reflect that idiosyncrasies are not constrained to monarchs. They are, in fact, the global state of affairs today.