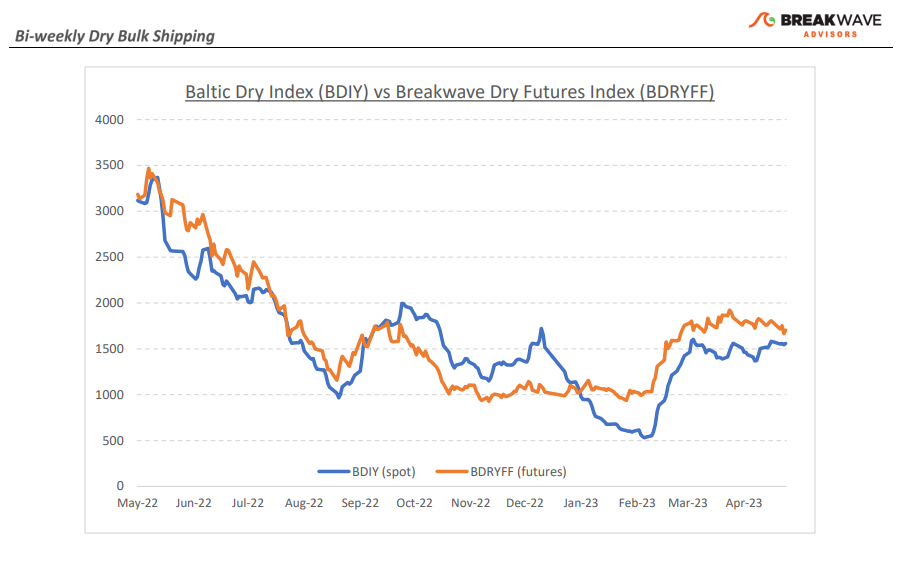

·Stability brings optimism, as Capesize spot rates reach 20,000 – As Capesize rates continue to gently move higher, one can feel an air of optimism amongst market participants. After all, with volatility having abated considerably from the highs of the last few years, the lack of steep drops in the spot market has translated to expectations for stronger rates for the rest of the year. On the other hand, the lack of volatility is also the exact reason why the futures curve has slowly converged to spot, thus flattening the curve, as the “embedded optionality value” has naturally also declined. Our view for gradual increase towards the mid-20,000s for Capesize spot rates remains in place, while at the same time we also feel that the current setup is more characteristic of a “calm before the storm” type, rather than a fundamental shift towards stability in the market balance. As a result, we expect the month of June to be quite volatile, and our initial forecast calls for a jump in spot Capesize rates ahead of the fiscal year-end for some of the major Australian miners. The dry bulk market is better balanced compared to the last decade, and that calls for higher lows and higher highs absent a significant deterioration in shipping market demand. Finally, looking at the smaller size dry bulk segments, we also feel that the bottom for spot rates is near, and although seasonality for those segments would call for a muted summer market, the Capesize sector has its way of supporting that smaller vessels during periods of robust rates, something which we think will be the case this time around as well.

·Iron ore price volatility increases, as sentiment and fundamentals collide – It has been an eventful fortnight for iron ore prices, as volatility increased and wild daily swings in futures have once again reappeared. On one hand, the disappointment over Chinese economic activity so far this year (PMI’s in April was a major disappointment) has led to some aggressive selling by the initial investors who bought iron ore exposure in anticipation of the “reopening” trade. On the other hand, fundamentals are supportive as the market currently remains tightly balanced despite expectations for a loosening in balance in the second half of the year. Historically, there is no correlation between freight and iron ore prices. However, there is a cause and effect when it comes to performance, as low iron ore prices shift volumes from higher cost producers to the more efficient ones, causing trade patterns to constantly change, creating inefficiencies and potentially tighten shipping supply.

·Dry bulk focus shifts back to fundamentals – Following a period of high uncertainty and significant disruptions across the commodity spectrum, the gradual normalization of trade is shifting the market’s attention back to the traditional demand and supply dynamics that have shaped dry bulk profitability for decades. As effective fleet supply growth for the next few years looks marginal, demand will be the main determinant of spot freight rates with China returning back to the driver’s seat as the dominant force of bulk imports and thus shipping demand.