· Chinese New Year celebrations are over, now what? – One of the slowest weeks of the year in terms of Chinese activity is now behind us, and the bulk commodity markets are once again looking forward to what the consensus sees as a solid rebound in physical demand for materials. Whether this is just unrealistic expectations or there is a genuine need to restock is anybody’s guess, but for dry bulk shipping the historical pattern points to gradually higher spot rates for the rest of the year. Such optimism is also built into a steepened futures curve, although the low levels of current spot rates propably exaggerate such a contango. It will be interesting to see whether the dry bulk market can move higher in the month of February that historically has been the weakest month of the year since CNY happened to be early this year, as it is unclear whether such an anomaly can have a meaningful impact on market balance. Although spot rates at almost zero make attractive headlines, the reality in shipping is that only averages matter, and such dips in activity are expected in an industry that is characterized by extreme volatility. We anticipate some revival in spot rates by the middle of next month, as China’s spring construction gets underway and steel demand pushes iron ore imports higher. Yet, any real sustainable push in import demand should come further down the road, reflecting the considerable stimulus already in the pipeline that will require increasing iron ore and steel quantities to support the new anticipated construction and manufacturing activity.

· Do China’s economic numbers point to a recovery? – We believe the bottom of the economic cycle for China is in. The obvious question is now how steep the recovery is, and so far, it does not seem to be a raging one. However, several issues remain in place. First, one of the slowest periods in terms of Chinese economic activity has just ended, namely the Golden Week and the New Year celebrations. Secondly, Covid infections remain an issue, and although the policy around that has been significantly relaxed, the pandemic remains an obstacle to an orderly recovery. Just like the western world, once there is a normalization in the handling of the pandemic in China, we expect regular economic activity to resume, and given the urgency to bring the economy back to growth, we anticipate a considerable boost in construction activity. All the above should begin to materialize in Q2, and thus, we are still months away from such a scenario. Commodity markets have moved higher with the hope of such a demand revival, but we don’t see any evidence just yet, at least not in shipping markets. Economic cycles are long and slow moving, but the impact on the dry bulk market should be steeper and more profound than in other China-related industries.

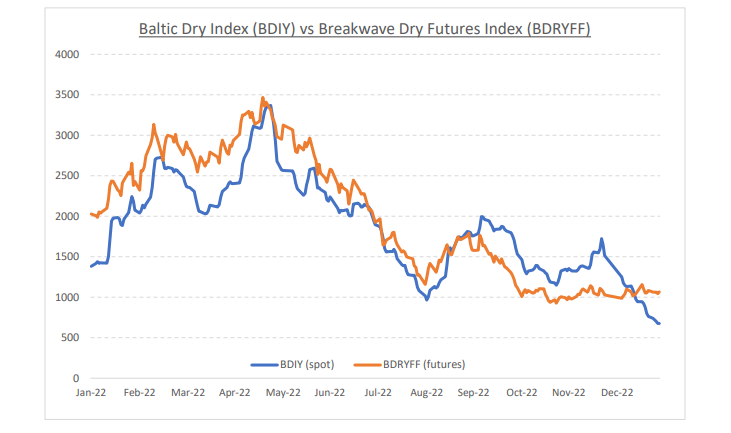

· Dry bulk focus shifts back to fundamentals – Following a period of high uncertainty and significant disruptions across the commodity spectrum, the gradual normalization of trade is shifting the market’s attention back to the traditional demand and supply dynamics that have shaped dry bulk profitability for decades. As effective fleet supply growth for the next few years looks marginal, demand will be the main determinant of spot freight rates with China returning back to the driver’s seat as the dominant force of bulk imports and thus shipping demand.