The freight market continues to lose momentum, while the number of vessels sailing in ballast status has gradually increased in the first days of April. It seems that the growth of demand ton-days has decreased since the first half of March, triggering downward pressure on the spot freight rates.

In the iron ore market, cargo prices with a 63.5% iron content for delivery into Tianjin have suddenly risen above $150/t, a price not seen in the last three weeks. The current price is the highest closing since August 2021, as investors expect robust restocking demand in China once COVID-19 restrictions ease. In addition, there are expectations of additional stimulus to strengthen the world’s second-largest economy. It is interesting to note that despite the recent spike in the iron ore prices, prices are estimated to drop to about $115/ton by June, based on the weak Chinese manufacturing data. China’s official Manufacturing PMI showed contracting activity at an index level of 49.5 for March, versus a consensus of 49.8.

In the coal segment, coal prices remain under $300/t since last week as Chinese demand is easing. Emerging news of a potential ban on Russian coal could play a significant role in the future evolution of prices and demand. Unnamed European officials revealed to CNBC that the European Commission is going to propose coal to be included in the last round of sanctions on Russia.

In the meantime, the grain market continues to face severe challenges in the supply chain from the continued Russia-Ukraine conflict. Ukraine’s railways are backlogged with grain shipments trying to find alternative export routes, and the logistic complications appear as they will very much reduce the level of Ukrainian grain exports. Estimates of grain analysts suggest that Ukrainian grain exports could reach only 1 million tons in the next month, while at the start of the season that number was approximately 43 million tons. In the meantime, the Uzbekistan government announced on the 4th of April that it plans to buy up to 600k tons of grain, mainly from the neighboring country of Kazakhstan, in order to increase stockpiles and ensure food security.

SECTION 1 - FREIGHT - Market Rates ($/t) - Weaker

‘The Big Picture’ - Capesize and Panamax Bulkers and Smaller Ship Sizes

A weaker sentiment of freight rates is mainly reflected in the smaller vessel size categories for this week, while freight rates for Capesize vessels are firmed up.

Capesize Brazil-to-North China freight rates increased above $26/t, while the past peak was Week 50, 2021 at levels of around $50/t.

Panamax Continent-to-Far East freight rates dropped to levels less than $55/t, but still keep robust levels compared to the bottom of $39/t during Week 4.

Supramax Indo-to-ECI freight rates appear in a free-fall with levels below $27/t.

Handysize NOPAC-to-Far East freight rates have continued their accelerated decline of the previous three weeks into the beginning of April and dropped to $63/t, which is almost $7/t down from the peak of Week 11.

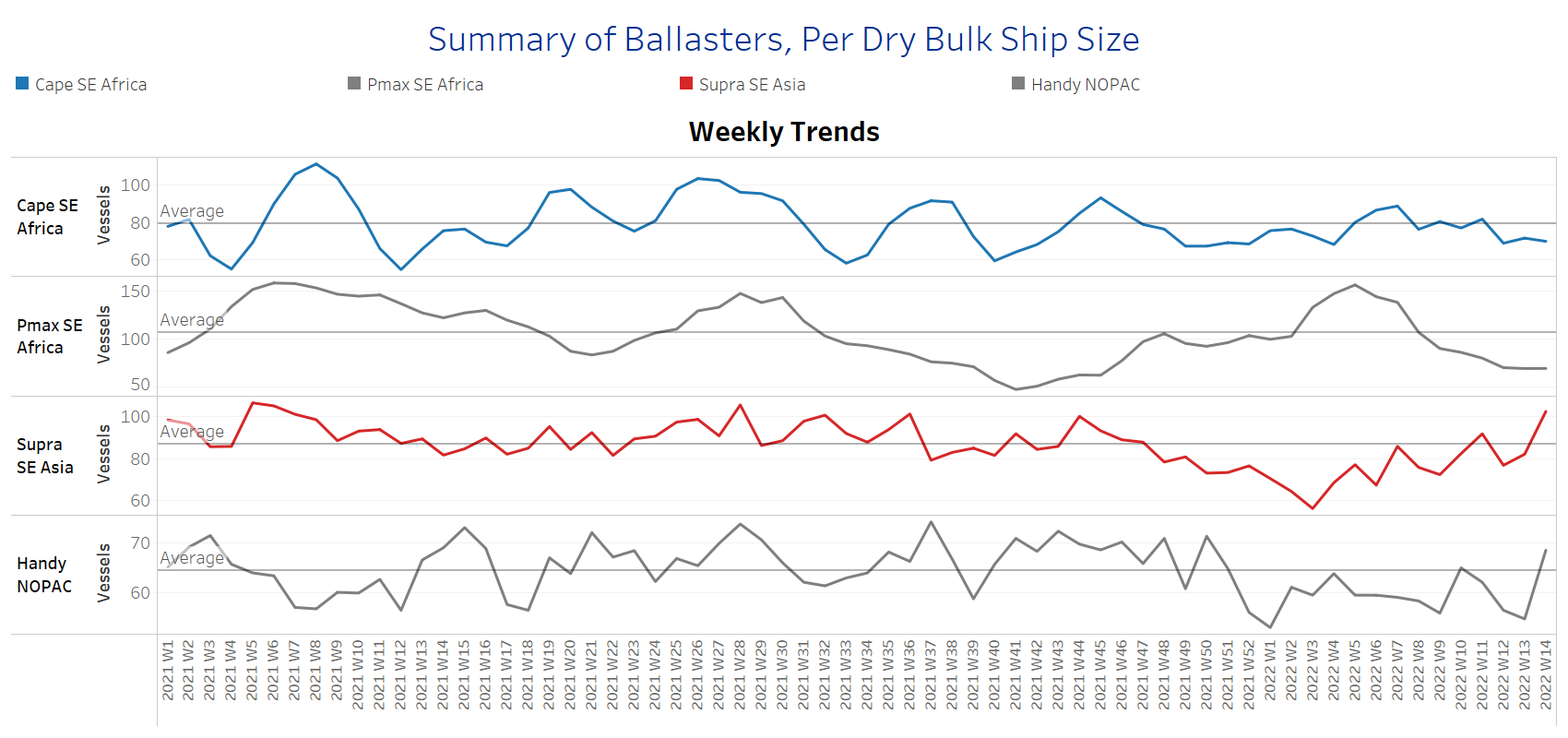

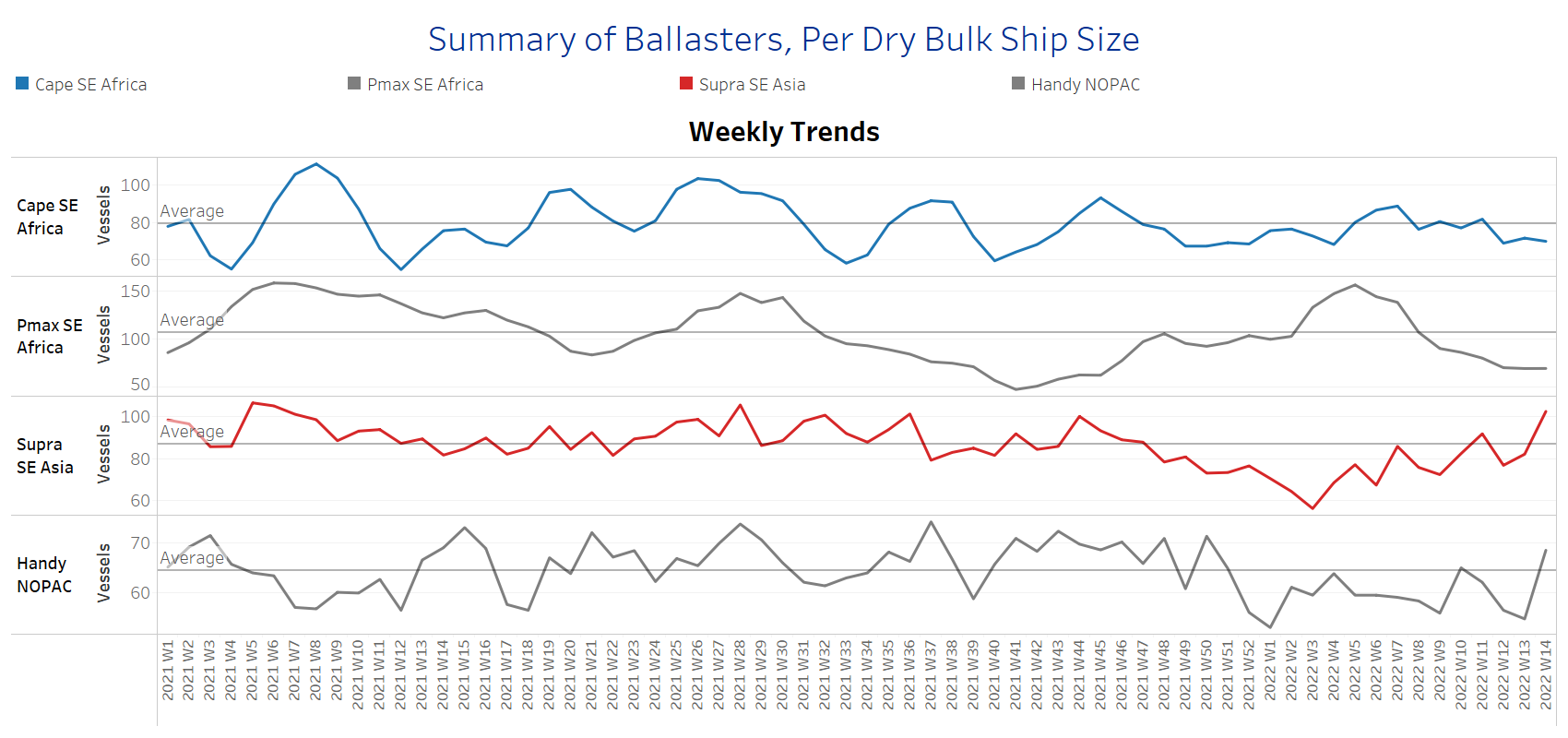

SECTION 2 - SUPPLY - Ballasters View

Number of Vessels - Increasing

Supply Trend Lines for Key Load Areas

The uptick of ballasters signals an increasing trend for all vessel size categories for the first days of April, however, the number of ballasters for the bigger vessels has grown at a comparatively slower pace.

Capesize SE Africa: The number of vessels sailing in ballast increased slightly this week to around 72 vessels, compared to around 69 during the last days of March. The number is now around 8 vessels less than the one-year average.

Panamax SE Africa: The number of vessels sailing in ballast is now around 75 vessels, which is 4 vessels more than the previous week. It remains at significantly lower levels over the last six weeks, however, it seems that the acceleration of decline is almost over, for now.

Supramax SE Asia: The number of vessels sailing in ballast recorded a sharp upward trajectory for the first days of April, with an increase to above 100 vessels, when last week ended with around 83 vessels in ballast status.

Handysize NOPAC: The number of vessels sailing in ballast keeps soaring levels for two consecutive weeks and it is now around 80 vessels, compared to less than 60 during the previous week.

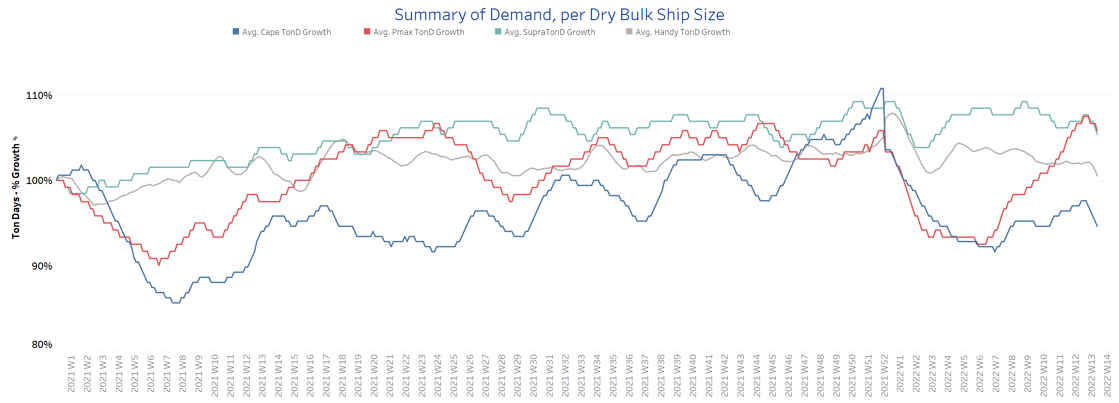

SECTION 3 - DEMAND - In Ton Days

Decreasing

The overall trend of demand ton-days is decreasing, while the accelerated growth evidenced in the Panamax segment during the previous two weeks seems now to have paused.

Capesize demand ton-days: There is a sharp dropdown in the first days of April following the last peak during the previous week.

Panamax demand ton-days: The accelerated growth of March has now paused for the beginning of this week, however, it eventually fetched the percentage level of increase of the Supramax.

Supramax demand ton-days: We see almost stability with no signs of spikes.

Handysize demand ton-days: Ton days growth continues slowing for a second consecutive week and we remain cautious about an increase in the short term.

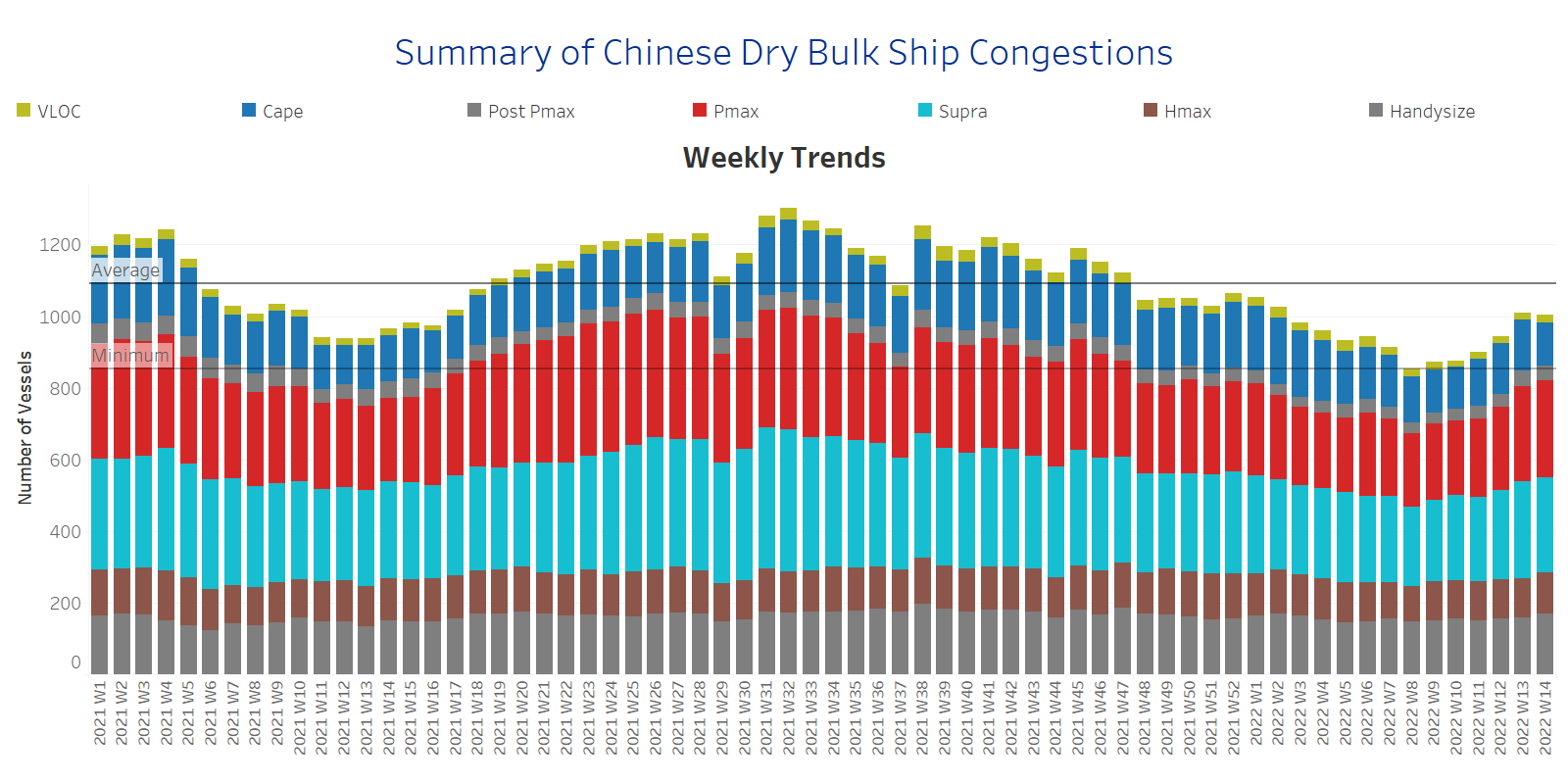

SECTION 4 - CHINESE PORT CONGESTIONS -

Number of Vessels - Decreasing

Dry bulk ships congested around Chinese ports

Dry bulk ships in congestion have shown a slight decrease for the first days of April, but still higher than the lows within Weeks 8, 9, and 10. The downward trend is mainly due to the drop in the supramax segment.

Capesize: The number of ships in congestion dropped to around 126 vessels when last week we saw the figure surpassing 140 vessels.

Panamax: There is a slight increase to 270 ships in congestion, which is eventually almost 5 vessels more than the ending of the previous week.

Supramax: There is a significant drop to 259 vessels when last week we saw numbers above 280 vessels.

Handysize: The number of ships in congestion seems to keep a steadiness at around 160 vessels. The beginning of this week brings 167 handysize vessels in congestion, which is a slight increase of 5 vessels from last week.

Data Source: Signal Ocean Platform