By Ulf Bergman

The Russian invasion of Ukraine has upended large parts of the global trade flow for agricultural commodities, with the grains from the fertile soils of Ukraine and Russia becoming unavailable for most international buyers. For example, around a quarter of global exports of wheat is being affected by the hostilities. However, it is essential to remember that many of the world’s largest consumers of grains, e.g. China and India, also produce significant quantities themselves and only import parts of their domestic needs. Hence, in reality, only a few per cent of the world’s consumption is affected. However, as global food supplies were already tight before the disruptions from the war, prices have been reacting in an outsized fashion.

While soybeans have given up most of the gains from the early stages of the war, corn and wheat prices remain close to twenty per cent higher even as prices have stabilised. The tighter supply situation is likely to keep grain prices higher for the foreseeable future and could lead to shortages in some parts of the world, notably in the third world where affordability is becoming an increasing concern. While the war has effectively suspended all grain shipments from the ports in the Black Sea, the timing meant that large parts of last year’s harvest had already been shipped. However, the longer the war continues, the greater the impact will be on the coming harvest and, hence, the real squeeze on supplies and price increases may lie ahead of us rather than in the past.

Beyond the direct impact that the war is having on supplies of grains and oilseeds from the affected region, the conflict could also have secondary effects on crop sizes globally. Even before the invasion, fertilisers were increasingly becoming “strategic” products, with many countries imposing export restrictions to ensure domestic supplies. Last year’s energy supply squeeze contributed to increasing prices and dwindling supplies. Russia’s growing international isolation in the face of economic sanctions is accentuating the development. Russia and its ally Belarus account for almost a fifth of the world’s fertiliser exports, with the former occupying the top spot in recent years.

The Russian authorities already imposed quotas on nitrogen fertilisers in November last year to ensure domestic supplies and prevent price inflation. However, in a retaliatory move against the Western sanctions, the Ministry of Industry and Trade has recently urged producers to halt all exports of crop nutrients. The initiative has contributed to fertiliser prices surging, with rising energy prices, and in particular natural gas, also playing their part. Hence, the global fertiliser trade is facing the double whammy of a crucial exporter becoming unavailable and a significant feedstock forcing other producers to either raise prices or cut back production.

The rising prices have already translated into a lower supply outlook for fertiliser-intensive crops, such as corn. The US Department of Agriculture’s recently released prospective plantings report suggested that corn sowings would cover four per cent less acreage in the coming season than it did a year ago. Instead, US farmers are opting for soybeans, which require less capital for fertilisers. North American fertiliser prices have increased around thirty per cent year-to-date and have more than doubled in the past twelve months. The development is threatening to exacerbate the tightening supply situation for some crops in the wake of the wake in Ukraine. Should the disruptions remain in place for a long time, reduced use of fertilisers could also see crop yields falling and put further pressure on global supplies of many grains.

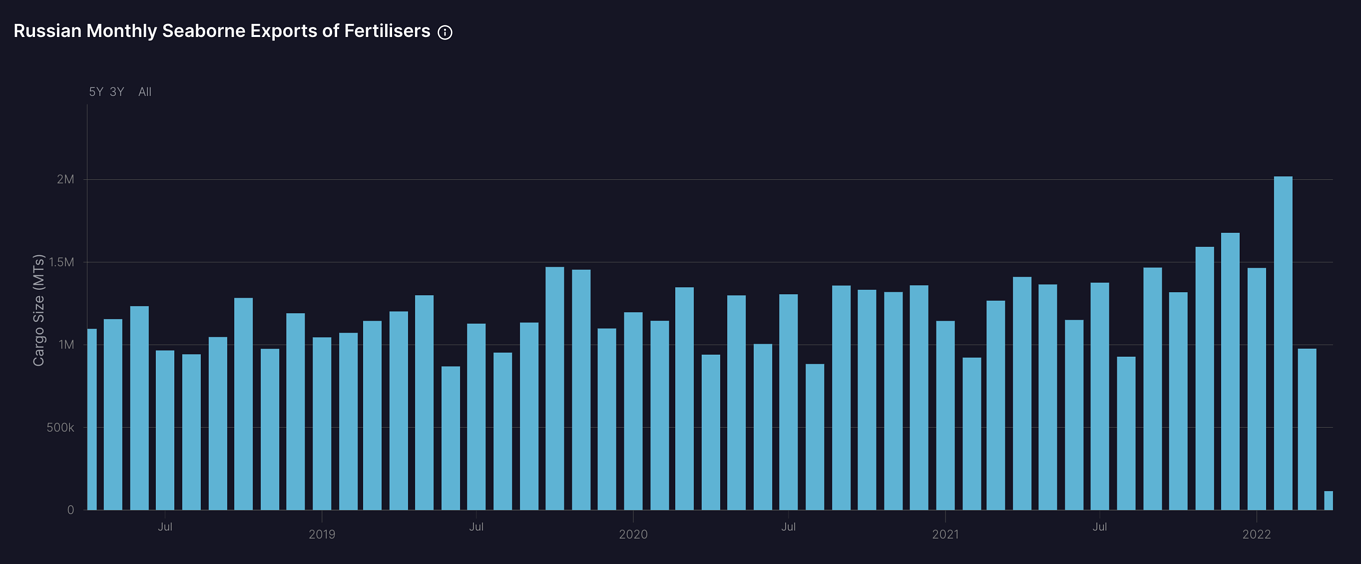

The sanctions on Russian trade and the move by authorities in Moscow to limit overseas shipments appear to have had a rapid effect on fertiliser shipments from the country’s ports. Shipfix’s trade flow data highlight a substantial change in volumes during March. While not excessively low in a historical context, Russian export volumes have fallen significantly compared to recent months. The data also emphasises that those shipments declined as the month progressed.

Source: Shipfix

Our cargo order data also highlight a significant drop in activities towards the end of last month. The early stages of the war saw a brief spike in orders for loading fertilisers in Russia, but the activities have been declining ever since and reached the lowest levels since Christmas 2020. Compared to the same month last year, order volumes were fifty per cent lower at around 1.5 million tonnes in March, as sanctions and export restrictions took their toll

Source: Shipfix

While Russian exports have been taking a nosedive in recent weeks, global aggregate order volumes for seaborne transportation of fertilisers kept up during last month and matched the levels recorded during February. However, the previous month looked less impressive on a year-on-year basis and declined by a third in such a comparison. In addition, the seasonal upswing during the first and second quarters that has developed in recent years shows no signs of materialising this year, with monthly volumes remaining in line with the preceding five. As a result, ordering activities have remained well below the levels recorded during last year’s second and third quarters.

As Russia’s fertiliser exports started to decline in the wake of its military activities in Ukraine, orders for cargo loading in other countries have increased. In particular, the demand for cargo to be loaded in Chinese ports has seen a revival following a period of decline. Still, those volumes are considerably lower than in recent years. With global grains and fertiliser supplies under pressure, Chinese authorities will likely move to ensure that there are sufficient stocks of grain nutrients for domestic use to maximise crop sizes. Hence, a return to the large volumes of Chinese exports seen previously is unlikely to materialise. Beyond China, orders for fertilisers to be loaded in ports in Morocco and Canada have also been on the rise, but to a lesser extent

Source: Shipfix

Data Source: Shipfix