Act IV – "Expectation is the root of all heartache."

The last quarter of this volatile trading year started with Baltic indices hovering at two-month highs. In spite of this positivity of late in the spot market, international organizations and central banks kept revisiting downwards their GDP growth and world trade volume projections. In particular, in early October, World Trade Organization stressed that world trade was expected to lose momentum in the second half of 2022 and remain subdued in 2023 as multiple shocks weigh on the global economy. WTO economists were expecting global merchandise trade volumes to grow by 3.5 percent in 2022 – slightly better than the 3.0 percent forecast in April. For 2023, however, they foresaw a marginal 1.0 percent increase – down sharply from the previous estimate of 3.4 percent.

Furthermore, the new World Trade Organization forecast estimated world GDP at market exchange rates would grow by 2.8 percent in 2022 and 2.3 percent in 2023, with the latter being a whole percentage point lower than what was previously projected. The aforementioned sluggish tone became apparent not only in the spot market of the dry bulk sector during the last three months but also in the container sector. Whilst concerns for the course of global economy kept rising, OPEC plus, with a bold move, agreed its deepest cuts to production in more than two years at a meeting in Vienna in early October. The cut of two million barrels a day represented about 2 percent of global oil production. The move threatened further inflationary pressures in a world economy already burdened by an energy crisis, drawing a sharp response from president Biden.

The US President called on his administration and Congress to explore ways to boost US energy production and reduce OPEC's control over energy prices after the cartel's "shortsighted" production cut. Spot market had not been in good spirits during the forty-first week of this challenging trading year. With Capesize and Panamax sectors setting a rather sluggish tone as early as Monday, the rest of the pack followed suit, pushing the general index lower to a Friday's closing of 1838 points. However, it was not only that week's uninspiring freight market that had a negative bearing on market psychology. In fact, the International Monetary Fund published the latest update of its World Economic Outlook mid-week. And it was among the gloomiest over the last many years.

As storm clouds gather, policymakers need to keep a steady hand, according to the IMF. The global economy continued to face steep challenges, shaped by the lingering effects of three powerful forces: the Russian invasion of Ukraine, a cost-of-living crisis caused by persistent and broadening inflation pressures, and the slowdown in China. Against these unfavourable currents, global growth was forecast to slow from 6.0 percent in 2021 to 3.2 percent in 2022 and 2.7 percent in 2023. This was the weakest growth profile since 2001 aside from the global financial crisis and the acute phase of the Covid-19 pandemic. As far as the largest economies go, US GDP contracted in the first half of 2022, the euro area shrank in the second half of 2022. Prolonged Covid outbreaks and lockdowns in China along with a growing property sector crisis had negatively affected the world’s second largest economy.

In reference to the two pillars of the dry bulk market, a weaker than expected output was projected for both China and India. In particular, growth in China weakened significantly since the start of 2022 and was subject to downward revision since the April 2022 lockdowns in Shanghai and elsewhere. Downside risks to China’s growth recovery dominated IMF's outlook, with signs of a significant slowdown in the real estate sector. Given that this sector constitutes circa one-fifth of GDP in China, the Fund downgraded China's growth to 3.3 percent in 2022 – the lowest level in more than four decades – and to 4.6 percent in 2023. The outlook for India was for growth of 6.8 percent in 2022 – a 0.6 percentage point downgrade since the July forecast, reflecting a weaker-than-expected outturn in the second quarter and more subdued external demand.

Whilst concerns for the course of global economy kept rising, global trade growth was slowing sharply from 10.1 percent in 2021 to a projected 4.3 percent in 2022 and 2.5 percent in 2023. This percentage growth was higher than the one in 2019 – when rising trade barriers constrained global trade – and also higher than during the Covid-19 crisis in 2020. However, it has to be noted that these projections were well below the historical average of 4.6 percent for 2000-21 and 5.4 percent for 1970-2021, according to the IMF. Additionally, the Washington-headquartered Fund stressed that the dollar’s appreciation over the last months was likely to have further slowed trade growth, especially considering the dollar’s dominant role in global trade.

In these challenging times, Chinese President Xi Jinping took the stage to start a historic congress of the ruling Communist Party. With Chinese economy battered by Covid-19 curbs and property sector crisis, countless Chinese citizens as well as investors across the globe were hoping the congress to mark a milestone after which the steam engine of global growth began laying the groundwork to dial back on zero-Covid policy. On the other hand, most of the analysts stressed that the congress was unlikely to trigger any immediate or dramatic. Baltic forward curves seemed to be in perfect alignment with the aforementioned analyst views, as the front end of the curves were in steep backwardation.

In the forty-second trading week, the spot market was trading within a very narrow range whilst China's third quarter GDP data were surprisingly not available on the official website. In fact, the only update from the government’s statistics department came to clarify that the renewed data would be delayed, without providing further explanation or comment. Away from the centre stage of the 20th National Congress of the Communist Party of China, a press conference on Monday addressed the delicate question of economic growth. “The economy rebounded significantly in the third quarter,” said Zhao Chenxin, a senior official at the National Development and Reform Commission. On the other hand, economists had forecast growth of just 3.3 percent – far below its 5.5 percent target for the year. Whilst a divergence of views between most of the economists and Zhao Chenxin became apparent, the latest official data published earlier this month indicated an economy trending sideways. In September, the Purchasing Manager Index (PMI) of China's manufacturing industry was 50.1 percent – up by 0.7 percentage points from the previous month – entering marginally into the expansion range.

As the latest macro data revealed a rather lukewarm picture for the course of the world’s second largest economy and the lack of fresh statistics injected uncertainty in the market, China’s state media emphasised on the previous decade economic progress. In 2021, China's gross domestic product reached 17.7 trillion US dollars, accounting for 18.5 percent of the world's total. From 2013 to 2021, it grew at an average annual rate of 6.6 percent, beating the average global growth of 2.6 percent. During the same period, its contribution to global economic growth averaged 38.6 percent, higher than that of the G7 countries combined. Amid endeavors to open up wider to the world, China's foreign trade had seen a robust expansion in the past decade. Setting aside China’s last decade impressive performance, in the third week of October, industrial metals as well as bulkers were eager for forward-looking statements and answers. In the absence of the aforementioned, iron ore's losses deepened, with the benchmark price of the steelmaking ingredient in Singapore hitting a fresh 2022 low. Steel prices in China – accounting for about half the world's output of the manufacturing material – also fell amid a worsening Covid-19 situation in Beijing. Capesizes, on the other hand, were reluctant to set course, trending sideways to their uninspiring levels and looking for further insights in the foreseeable future.

In the last week of October, China reported, at last, the delayed GDP growth data for the third quarter. Few days after China’s Communist Party 20th National Congress, Beijing stressed that the world’s second largest economy rebounded at a faster-than-expected pace in the third quarter. In particular, gross domestic product expanded by 3.9 percent in the July-September quarter year-on-year. The aforementioned performance stood above the 3.4 percent pace forecast in a Reuters news agency poll of analysts, and quickened from the 0.4 percent pace in the second quarter. The utilization rate of national industrial capacity balanced at 75.6 percent, down 1.5 percentage points from the same period last year, but 0.5 percentage point higher than the previous quarter. In spite of the marginal increase of utilization rate of national industrial capacity quarter-on-quarter, the power production was decreased in September. In fact, the power generation was 683 billion kwh the previous month, or a year-on-year decrease of 0.4 percent. From the perspective of sources, in September, the growth of thermal power and wind power slowed down, the decline of hydropower and nuclear power expanded, and the growth of solar power accelerated.

As far as the dry bulk commodities are concerned, China imported 99.71 million tonnes of iron ore in September, or up 3.5 million tonnes or 3.6 percent on the month. The total amount of imported iron ore in January-September decreased by 2.3 percent year-onyear to 822.54 million tonnes. Conversely, China’s coal imports rose 12.2 percent in September from a month earlier, with the imports from Indonesia being on a rise. Coal imports totalled 33.05 million tonnes last month, up from 29.46 million tonnes in August. Reporting a significant increase, China’s soybean imports in September rose 12 percent from a year earlier to 7.72 million tonnes, reversing a multi-month trend of low arrivals. Even though the September imports were higher, overall imports for the first nine months of the year remain down 6.6 percent compared to last year at 69.04 million tonnes.

Whilst Chinese economy seemed to have built a certain momentum in the third quarter, albeit not comparable to those of recent past, all eyes were on the reverberations of the 20th National Congress of the Chinese Communist Party. Since the meeting was mostly about personnel changes, the absence of much-anticipated growthsupporting measures echoed across most markets. Hong Kong and mainland China stock markets fell sharply while other major AsiaPacific markets rose. Iron ore extended its rout to the lowest level in more than two years on mounting concerns over global steel demand. In tandem, Baltic indices were also in the red in the last trading week of October, losing more steam within the typically sturdy fourth quarter. The forty-fourth week was one of those uninspiring periods taking place in the conventionally seasonal weakest first quarter of every trading year.

In fact, with all sub-indices being in the red, Baltic Dry Index concluded on the first Friday of November at 1323 points. Reporting circa 20 percent weekly losses, the leading Baltic Capesize index was flirting with the four-digits, before bouncing back at $11,139 daily just before the closing of the week. In a similar vein, Baltic Panamax 82K index moved further south, yet still managing to close with a positive tone. Conversely, this was not the case in the Supramax spectrum, with the respective Baltic Supramax Index losing some 14.5 percent week-on-week and ending at multi-month lows of $13,945 daily. Being trapped in a downward spiral, the Baltic Handysize Index finished at twenty-month minima of $15,043 daily, last seen in February 2021. Better reflecting the cloudy macroeconomic environment, Handies have this unique “privilege” to mirror the course of the global economy on their balancing levels.

Further challenging an already sputtering global economy, the Federal Reserve raised the target range for the federal funds rate by another 75bps in early November to 3.75-4 percent. Being in line with market forecasts, the aforementioned rise marked a sixth consecutive rate hike and the fourth straight three-quarter point supersized increase, pushing borrowing costs to a fresh high since 2008. Policymakers anticipated that ongoing increases in the target range would be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. Additionally, Federal Reserve chair Jay Powell warned interest rates would peak at a higher level than initially expected even as he held out the possibility of the Federal Reserve slowing the pace of its campaign to tighten monetary policy. The comments of Jerome Powell that it was "very premature" to be thinking about pausing its rate hikes sent stocks lower as US bond yields and the US dollar rose. The Dow Jones Industrial Average slid 505.44 points, or 1.55 percent, to settle at 32,147.76. The S&P 500 dropped by 2.5 percent to close at 3,759.69, whilst the Nasdaq Composite took a 3.36 percent dive to finish at 10,524.80. While inflation remained high, stocks began to rally in October in the hope that the Federal Reserve would start to pivot away from aggressive interest-rate hiking in December. However, the latest developments on the monetary policy front had a negative bearing on November’s opening.

On the other side of the moon, iron ore futures climbed in the first week of November, solidifying their weekly gains initially driven by earlier speculations that top steel producer China would ease its draconian Covid-19 rules, and further fuelled by Beijing's fresh progrowth rhetoric. After suffering its steepest monthly fall in almost two years in October, the market reversal during the forty-fourth week came despite China's National Health Commission denying knowledge of a rumoured committee being formed to assess border reopening in March 2023.

The market of the steelmaking ingredient decided to focus on People’s Bank of China Governor Yi Gang reassurance that China would be able to maintain normal monetary policy as he steered for a resilient domestic economy, and expressed hopes for a soft landing in the suffering property sector. Whilst concerns had been expressed by various financial institutions and associations that the Chinese steel sector along with global steel demand was remaining in a quite uncertain and fragile phase, Capesizes turned a Nelson's eye to these warnings and pledged allegiance to the iron ore futures trend. Setting aside the spot market of the geared segments, the forty-fifth week was anything but dull. Risk assets rallied the previous Friday amid speculation that China was preparing to relax its pandemic restrictions.

However, over the weekend, health officials reiterated their commitment to the “dynamic-clearing” approach to Covid-19 cases as soon as they emerge. Against this backdrop, US stock futures and commodities slipped in Asia on Monday. In sync, Oil prices reported $1 a barrel loss, with Brent crude futures dropping as low as $96.50 earlier in the day. Following a 7.5 percent increase last Friday, copper prices also traded lower as the reality of China’s “Zero-Covid” policy weighed on the industrial metal outlook. Capesizes, on the other hand, started the week on the right foot, with the BCI 5TC balancing at $11,648 daily on Monday's closing after reporting daily gains of $509. On Monday November 7, Norwegian Prime Minister Jonas Gahr Store and the US Special Presidential Envoy for Climate John Kerry chaired the launch of the Green Shipping Challenge during the World Leaders Summit of COP27. Countries, ports, and companies made more than 40 major announcements on issues such as innovations for ships, expansion in low- or zero-emission fuels, and policies to help promote the uptake of next-generation vessels. Additionally, international zero-emission shipping routes came one step closer to becoming a reality, as the UK made a major pledge alongside the US, Norway, and the Netherlands to roll out green maritime links between them at this year’s COP27 conference in Sharm el Sheikh, Egypt.

The headline economic news in mid-November though was neither related to the COP27 climate summit nor to the US midterm elections which dominated mainly the political press. Being the main theme of the front pages, the US inflation rate inched down in October at last! The all-items index increased 7.7 percent for the 12 months ending October, this was the smallest 12-month increase since the period ending January 2022. The all items less food and energy index rose 6.3 percent over the last 12 months. As expectations mounted that the Federal Reserve would increase interest rates by a lesser percentage in December compared to the previous increases, stock futures soared. The S&P 500 surged by more than 5 percent after the data were published. The Nasdaq Composite surged by 7.35 percent – its best since March 2020 – closing at 11,114.15. Global stocks rose on hopes for less aggressive interest rate hikes from the Federal Reserve, an outlook that has the dollar facing its biggest two-day drop in almost 14 years.

Nevertheless, the week was not over yet. On Friday November 11, Beijing eased some of its stringent Covid-19 rules, shortening quarantines by two days for close contacts and for inbound travellers and removing a penalty for airlines for bringing in too many cases. Additionally, China would stop trying to identify “secondary” contacts. Markets were cheered by the loosening of the curbs, albeit many sources stressing that these measures were only incremental and reopening possibly remained way off. Soever, oil prices reported strong gains in the last trading days of the week, on rising hopes of improved economic activity and demand in the world’s top crude importer. In tandem, industrial metal prices jumped, following a rise the day before in anticipation of a dovish pivot by the Fed. A weaker US dollar also supported commodity prices as it makes them relatively cheaper for buyers holding other currencies. Whilst short-term positive emotional factors are dominating most of the markets, dry bulk shipping seems to take small notice thereof.

The forty-sixth week started with the IMF stressing that global economic growth prospects were confronting a unique mix of headwinds, including Russia’s invasion of Ukraine, interest rate increases to contain inflation, and lingering pandemic effects such as China’s lockdowns and disruptions in supply chains. With such a demoralizing start, few assets could find the courage to defy the law of gravity. Baltic indices were not among them, with the whole pack being dragged down to multi-month minima. In particular, the leading Baltic Capesize index landed in the four-digits, concluding today at a mere $9,305 daily. Trending sideways, Baltic Panamax 82K index closed the trading week in the red, lingering at $14,343 daily. Echoing concerns for the course of global economy on their balancing levels, geared segments seem to be trapped in a downward spiral, concluding at $12,870 and $13,727 daily for the Baltic Supramax and Handysize Indices respectively.

In the Fund's latest World Economic Outlook, global growth was forecasted for next year to balance at 2.7 percent, a sizeable downward revision from few months earlier. In sync, readings for a growing share of G20 countries had fallen from expansionary territory earlier this year to levels that signal contraction. That was the case for both advanced and emerging market economies, underscoring the slowdown’s global nature. While gross domestic product releases for the third quarter surprised on the upside in some major economies, October PMI releases point to weakness in the fourth quarter – particularly in Europe. In China, intermittent pandemic lockdowns and the struggling real estate sector were again contributing to a slowdown that can be seen not only in PMI data but also in investment, industrial production, and retail sales.

Setting aside the stressed real estate sector, the world’s second largest economy was facing another challenge this November. Covid-19 cases rose significantly, climbing to near their highest of the pandemic. As the country eased some of its draconian Zero Covid-19 rules, authorities signaled that they were preparing to face even more infections. In fact, China reported 24,028 infections on Thursday November 17– the highest since April when Shanghai’s outbreak spurred a surge in the national tally.

Against this backdrop, Asian markets were in cautious mood during the third week of November, with investors preoccupied by the gloomy global economic picture and Covid’s persistence in China. The Nikkei ended the forty-sixth week marginally lower, reversing small gains from earlier. Hong Kong stocks dropped off amid more losses for Chinese property developers. China stocks trended mostly sideways, tracking the cautious mood in regional markets amid concerns of aggressive US tightening and domestic Covid outbreaks. In commodity markets, oil futures regained some ground but still nursed steep losses for the week on worries about Chinese demand and tighter monetary policy in the US. In sharp contrast, iron ore futures advanced and were set for their third straight weekly rise.

Expectations that Beijing would present enhanced policy actions to support the economy – after easing some of its strict Covid-19 containment rules and unveiling fresh measures to aid an ailing property sector – added to the buoyant mood. The latter was largely absent though from the spot market for yet another week. In a sea full of reds, the forty-seventh trading week painted our screens with few brushstrokes of green at last! In fact, on the early side of the week, Capesizes took the lead, revisiting the five-digit territory on Wednesday and concluding on Friday at $13,373 daily.

Panamaxes made some baby steps towards the right direction on the second half of the week, yet closing the last full trading week of November down at $13,310 daily. In a similar vein but with marginal weekly gains, Supramaxes balanced at $13,004 daily. Moving further south, Handies landed at $13,403 daily, last seen in mid-February 2021. In spite of the mixed signals, Capesizes’ positive reaction, injected some moderate optimism in the spot market of the dry bulk sector. In sharp contrast, on the macro front, OECD stressed that global economy was still facing mounting challenges. In particular, growth lost momentum, high inflation was proving persistent, confidence weakened, and uncertainty was high.

Global financial conditions had tightened significantly, amidst the unprecedented sturdy and widespread steps to raise interest rates by central banks lately, having a negative bearing on interest-sensitive spending and adding to the pressures faced by many emerging economies. Labour market conditions generally remained tight, yet wage increases have not kept up with price inflation, weakening real incomes. In terms of global trade, it continued to recover in the first half of 2022, helped by solid demand and significant easing in supply chain bottlenecks and port congestion. The aforementioned helped to counterbalance a material contraction in China’s imports in the first half of 2022 as its zero Covid-19 policy remained in place. By the third quarter of 2022, the volume of global trade in goods and services was 7 percent higher than in the fourth quarter of 2019, despite the incomplete recovery in services trade. Recent trade indicators were mixed, but there were signals that trade growth was set to slow. Survey measures of new export orders in manufacturing have fallen sharply, particularly in Europe.

Container port traffic volumes continued to rise through to September, but early estimates from the Kiel Trade Indicator suggested that global merchandise trade might had contracted in October. When global economy and international trade appear to be wobbly, Chinese economic data are the focal point. Economic growth of the world’s second largest economy was expected to slow to 3.3 percent in 2022 and to rebound to 4.6 percent in 2023 and 4.1 percent in 2024. The emergence of the omicron variant led to recurring waves of lockdowns this year, disrupting economic activity. Additionally, the Chinese October macro data published in mid-November did not show an improvement in real estate, with both property investment (-8.8 percent Y-o-Y YTD) and residential property sales (-28.2 percent Y-o-Y YTD) remaining dull.

By contrast, infrastructure investment remained strong (+8.7 percent YTD), reflecting the stepping up of government support. China’s central bank announced a relief package for the struggling property sector, consisting of 16 measures. These include a call to banks to step up lending to financially sound property developers, increased access to presale funds for healthy developers, the extension of payment deadlines for distressed developers enabling debt workouts, and additional efforts to safeguard the construction of unfinished projects. Iron ore futures advanced on the last Friday of November and were set for their third straight weekly rise, as the top steel producer’s latest moves to support its flagging economy brightened demand prospects. Capesizes decided to align themselves with this trend, reporting the first significant weekly gains seen in months.

December started with the World Trade Organisation expressing concerns that trade growth is likely to decelerate in the closing months of 2022 and into 2023, according to the latest WTO Goods Trade Barometer. The latest reading of 96.2 was below both the baseline value for the index and the previous reading of 100.0, reflecting cooling demand for traded goods. The drop in the goods barometer was consistent with the WTO's trade forecast of early October, which predicted merchandise trade volume growth of 3.5 percent in 2022 and just 1.0 percent in 2023. Following an expansion of 4.8 percent in the first quarter, merchandise trade posted a 4.7 percent year-on-year increase in the second quarter. For the second half of 2022 materially lower pace of circa 2.4 percent is needed in order for the forecast to be realised.

This downward trend of the merchandise trade volume growth became apparent in both the dry bulk and container shipping markets. During the second half of the current trading year, the container market remained on the path towards “normalisation”, according to BIMCO. The Shanghai Containerized Freight Index (SCFI), which represents spot freight rates for loading in Shanghai, fell another 49 percent during the previous couple of months and lay 74 percent below its peak of early January 2022. The index for average freight rates for all containers loading in China, the China Containerized Freight Index (CCFI) continued to fall, balancing 40 percent lower than two and a half months ago, and 54 percent lower than at its peak reached in February 2022. The SCFI was back to levels last seen in September 2020. In parallel, the time charter rates and second-hand prices for vessels followed the freight rates downwards. Compared to two and a half months ago, average time charter rates and average second-hand prices were down 64 percent and 33 percent respectively, as quoted by the key shipping industry body BIMCO. In a similar vein, Baltic Dry Indices too held their course steady towards “normalisation”, reverting closer to their trailing decade average values. In particular, the general Baltic Dry Index ended the first Friday of December at 1324 points, tick less than the respective average value of the 2016-2020 period and tick above the 1301 points that the leading dry bulk index averaged in the second day of December during the five-year period ended in December 2015.

Just before the closing of the first trading week of December, stock exchanges were looking for answers to the US jobs data at the same time as dry bulk was focusing on China’s mounting bills of the stringent zero-Covid policy. In reference to the former, US stock indices moved south, as higher-than-expected job additions in November reignited investor concerns about the Federal Reserve continuing on its path of aggressive monetary policy tightening. On the other hand, Baltic indices were idly watching China’s attempt to gradually ease zero-Covid policy, awaiting for a substantiation to a broader extent of these measures to earn their attention.

November was a rather uninspiring month for the world's second largest economy, with all main macro data indicating a softer toneacross the board. In particular, the purchasing managers' index (PMI) for China's manufacturing sector came in at 48 in November, down from 49.2 in October, according to data from the National Bureau of Statistics. Additionally, China’s imports and exports shrank at their steepest pace in at least two and a half years in November, with weakening global demand and strict anti-virus controls in major Chinese cities having a clear negative bearing on the reported trading volumes. In fact, exports took a 9-percent year-on-year dive to $296.1 billion, worsening from October’s marginal decline. The downturn was even more severe than markets had forecast, with economists predicting a further period of declining exports. On the same wavelength, imports fell sharply by 10.9 percent to $226.2 billion in November, down from the previous month’s 0.7-percent retreat. Amidst a monetary tightening in the US and the European continent, shipments to the US plummeted by 25.43 percent in November compared to the same period last year, while exports to the European Union fell by 10.62 percent year-on-year. Conversely, imports from Russia, mostly energy-related, rose 28 percent from a year earlier to $10.5 billion at the same time as exports to Russia were increasing by 18.5 percent to $7.7 billion.

In the dry bulk spectrum, a rather mixed picture came to light. On the one hand, on a monthly basis, iron ore and coal imports reported strong gains. On the other hand, they were still remaining considerably lower year-on-year. Particularly, Chinese customs cleared 98.85 million tonnes of iron ore during the previous month, up from an October reading of 94.98 million. However, November arrivals were 7.8 percent lower than the same month in 2021 and year-to-date imports were 2.1 percent down. Symmetrically, coal imports also looked strong in November, rising to 32.3 million tonnes from October's 29.18 million. However, total imports for the first 11 months of the year dropped 10.1 percent compared to the same period last year. Soybean November imports fell 14 percent on the year to 7.35 million tonnes. After slower loading of shipments and longer customs clearance time, the softer number followed October's plunge in arrivals to just 4.1 million tonnes – the lowest level since 2014. For the first 11 months of the year, imports of the protein-rich beans were down 8.1 percent at 80.53 million tonnes.

With the economic outlook coloured by various shades of grey and in the amidst of mass protests, China signaled a shift in its uncompromising Covid-19 stance as it moved to ease some restrictions despite high daily case numbers. Yuan reached a threemonth high early and Chinese stock markets rose as investors looked beyond poor data to growth prospects. There were early signs as well that steel mills were re-stocking iron ore ahead of an expected lift in demand in the new year. However, many analysts and business leaders expressed concerns, expecting Chinese economy to rebound only later next year as the path ahead might be rocky. Few trading days are left before the final curtain and the Baltic Dry Indices are still in search for at least one great victory in the fourth quarter. Setting aside some strong daily gains in the Capesize segment every now and then and a modest mid-November positive Panamax reaction, the tone of the market during this final quarter has been rather soft. The aforementioned trend became apparent especially in the geared segments, with both BSI TCA and BHSI TCA losing more than five thousand dollars quarter to date. In tandem, the UNCTAD nowcast indicated that the value of global trade will decrease in the fourth quarter of 2022 both for goods and for services. Global trade should hit a record $32 trillion for 2022, but a slowdown that began in the second half of the year is expected to worsen in 2023 as geopolitical tensions and tight financial conditions persist, according to the latest Global Trade Update published by UNCTAD.

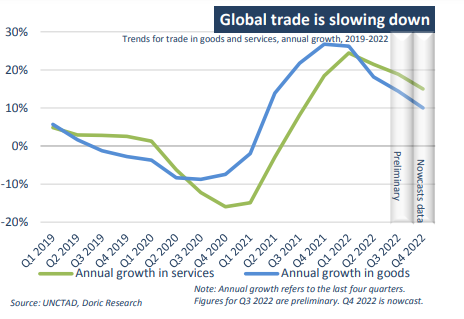

While the outlook for global trade remains uncertain, negative factors appear to outweigh positive trends, according to the intergovernmental organization. In particular, economic growth projections for 2023 are being revised downwards due to high energy prices, tighter monetary policies and sustained inflation in many economies. Additionally, persistently high commodity prices and the continued rise in the prices of intermediate inputs and consumers goods are expected to negatively affect demand for imports. Last but not least, record levels of global debt and the increase in interest rates pose significant concerns for debt sustainability. On the contrary, recently signed agreements such as the Regional Comprehensive Economic Partnership and the African Continental Free Trade Area, as well as improvements in the logistics of global trade are expected to have a positive bearing in the trading volumes of 2023.

As far as the maritime trade is concerned, UNCTAD projects it will lose further steam, with growth slowing to 1.4 percent in 2022. Although freight and hire rates have fallen since mid-2022, they are still above pre-Covid-19 levels. Market levels remain high for oil and natural gas tanker cargo due to the ongoing energy crisis. In an increasingly unpredictable operating environment, future shipping costs will likely be higher and more volatile than in the past. For the period 2023-2027, maritime trade is expected to grow at 2.1 percent annually – considerably slower than the 3.3 percent average recorded during the past three decades.

In a similar vein, Dry Bulk Indices kept trading in a narrow range, bracing themselves for what the ill-famed first quarter will bring.

Curtain Falls On 2022

At the outset of 2022, the current challenging trading year can be considered a tipping point in recent history, characterized by economic, geopolitical, and environmental disruptions. From fighting off what was hopefully the final phase of the pandemic to a full-blown war, a plethora of events and circumstances kept shifting dynamics and balances in most of the markets across the globe.

The tentative post-pandemic recovery was derailed in the second half of the challenging 2022, as the global economy was confronted by a rare convergence of misfortunes. The post-Covid economic boom bequeathed a supply-demand imbalance to the global market. A generous portion of today’s economic distortion derives from unusual disruptions to supply and vast, unpredictable swings in demand. Aggregate demand stimuli were not the optimal medicine for the Covid-related economic issues. Stimulating demand without stimulating supply proportionally generates stubbornly high inflation. Tightening fiscal and monetary policy seems to be the appropriate remedy to tackle galloping consumer price indices, albeit with a substantial adverse effect on economic growth. In this juncture, trade of merchandise goods has to follow closely GDP growth rates on their downward revisions. Additionally, the biggest military conflict in Europe since World War II had also a quite sizeable negative bearing on the course of global economy. In some respects, the 'specific gravity' of Russia and Ukraine in the global economy is relatively small.

However, Russia and Ukraine do have an important influence on the global economy, being key commodity exporters. The Russian invasion of Ukraine pushed commodity prices higher and amplified the aforementioned shift in global financial conditions. Furthermore, China reported a sharp slowdown in economic activity as the world’s second largest economy saw a slow recovery from the widespread Covid-19 lockdowns and a numb downstream demand in its key property sector. Supply shortages,exacerbated by the war in Ukraine and Covid-related lockdowns in China hold back growth during the second half of 2022 to a greater extent than previously foreseen.

Turning towards 2023, the key macroeconomic question of the year is whether inflationary overheating can be tamed without triggering a broad-based recession, given tighter fiscal and monetary policies. On this topic, consensus seems to be in discordance. Under most of the scenarios though, markets should brace themselves for a year of below-potential growth. China has to walk a rather bumpy path in the upcoming months, supporting its recent decision to exit from the stringent zero-Covid policy. With mounting daily cases, the balancing act between opening-up and the social impact of the Covid spread in the country is expected to be quite challenging. Global trade should hit a record $32 trillion for 2022, but a slowdown that began in the second half of the year is expected to worsen in 2023 as geopolitical tensions and tight financial conditions persist, according to the latest Global Trade Update published by UNCTAD. In tandem, maritime trade is projected to lose further steam, with growth slowing to 2.1 percent annually for the period 2023-2027 – considerably slower than the 3.3 percent average recorded during the past three decades. Demand growth in the dry bulk spectrum is projected to be shy of 2.0 percent in terms of tonnes, with the tonne-mile growth being tick above this figure. On the supply side, dry bulk fleet growth is expected to reach 2.8 percent in 2022 and just 2.4 percent in 2023. Additionally, the new IMO regulations are expected to reduce the actual supply of tonnage in the spot market as much as 1.0 percent. When trying to integrate the aforementioned driving factors into next year’s outlook, a less festive tone echoes compared to that in early 2022.

May your sails have good winds in 2023!

-You can find Part1 here

-You can find Part 2 here

Data source: Doric