Tanker - Weekly Market Monitor

Snapshot of Crude and Product Freight Rates, Supply-Demand

Week 34, August 22, 2024

Chart of the Week: Arabian Gulf dirty oil shipments to all destinations

This week’s special focus is on the dirty oil flows from Arabian Gulf origin countries to all destinations, particularly in light of the ongoing Middle East tensions. Below, we examine the evolution of these flows between 2023 and 2024, comparing the monthly volumes. In the first quarter of this year, the flow of shipments from the Arabian Gulf followed a similar pattern to that of the previous year. However, noticeable variations began to emerge from April onward. June saw a significant drop, with volumes falling to nearly 65 million tonnes, a stark contrast to the previous year’s record peak of over 75 million tonnes in May.

In the second quarter of this year, there was a clear downward trend from the levels recorded in the first three months. After hitting a low in June, volumes rebounded in July, showing a notable adjustment. Overall, for the first seven months of this year, there has been a 3% decline in the total quantity of dirty crude oil shipments from the Arabian Gulf to all destinations. Despite the escalating Middle East tensions, there has not yet been significant downward pressure on overall tonnage, as July saw a recovery. It remains to be seen whether the impact will be greater in August and September.

When analysing trends by vessel class, it is noteworthy that large vessel categories like VLCC, Suezmax, and Aframax have maintained volumes close to last year’s levels, however, with a slight downward trend. Interestingly, MR2 tankers have doubled their share of dirty oil shipments from the Arabian Gulf compared to last year.

As August draws to a close, the earlier weakening momentum on the VLCC AG-China route appears to have stabilised to a firmer momentum. Despite this stabilisation, the weekly percentage growth in demand tonne days has not yet surpassed previous weeks, indicating that a strong recovery remains elusive.

On the demand side, the persistently weak Chinese economic environment continues to pose significant challenges. China's sluggish economic performance, marked by slow industrial output and a decline in new home prices, is dampening the demand for crude oil imports. This, in turn, affects the VLCC market, as China is one of the largest consumers of crude oil transported via this route.

The ongoing uncertainty in China's economic outlook adds to the difficulty of predicting a near-term rebound in VLCC demand. As refineries in China continue to operate at reduced capacity due to weak fuel demand, the pressure on the VLCC AG-China route is likely to persist. Market participants are closely monitoring economic indicators and potential policy responses from the Chinese government, which could influence oil demand in the coming weeks. However, without a significant improvement in China's economic conditions, the VLCC market may struggle to regain strong upward momentum in the short run.

Data from last week revealed that China's economy lost significant momentum in July, marked by the sharpest decline in new home prices in nine years and a slowdown in industrial output. In response to weak domestic fuel demand, Chinese refineries have significantly reduced their crude processing rates. This downturn has raised concerns about the broader implications for the global oil market. Goldman Sachs analysts have projected that Brent crude prices could fall to $68 per barrel by late 2025 if China's oil demand remains stagnant through the end of next year. The bank noted that "soft China oil demand and downside risks to China GDP growth strengthen our view that the risks to our $75-$90 Brent range in 2025 skew to the downside." Goldman Sachs estimates that China’s year-on-year oil demand growth sharply slowed to 200,000 barrels per day in the first half of this year, with an expected year-on-year decline during the summer.

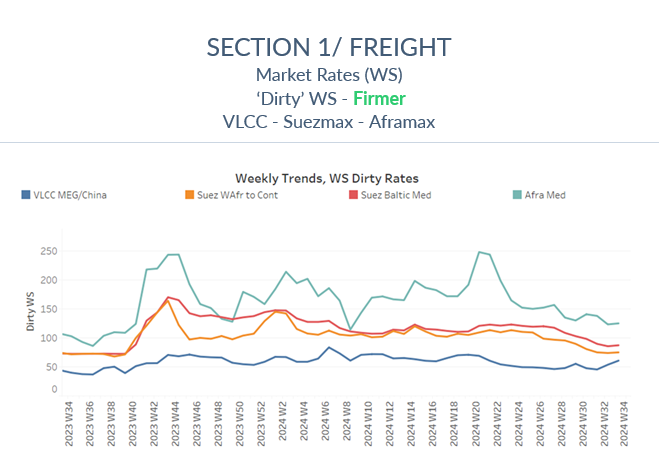

The dirty freight market sentiment appears to be stabilising before the end of August, as evidenced by a recent uptick in VLCC MEG-China rates. These rates have shown an increase compared to the lower levels observed at the beginning of the month, suggesting a potential shift towards a more robust market.

The VLCC MEG-China freight rates rose to 60 WS, reflecting a 27% increase from the previous week and a 36% rise compared to the same week in August of the previous year.

Suezmax freight rates for shipments from West Africa to continental Europe reached 75 WS, reflecting a 7% increase compared to the previous year. Likewise, rates on the Suez Baltic Med route have stabilised at approximately 88 WS, representing a 17% annual rise.

Aframax Mediterranean freight rates are hovering around WS120, marking a 16% increase compared to the same week last year.

The supply trend for crude tankers shows a decline for Suezmax vessels in the West Africa-to-Continent route and Aframax vessels in the Mediterranean and Baltic regions. However, VLCCs from Ras Tanura have experienced an uptick in August, with supply levels close to surpassing the annual average by the end of the third week of the month.

VLCC Ras Tanura: The number of ships is now 72, nearly 17 more than the levels at the end of week 30.

Suezmax Wafr: The current ship count stands at 50, with no signs of an impending increase for the remainder of the month. This week’s levels are 15 ships lower than they were four weeks ago.

Aframax Med: The number of ships has decreased to 4, nearly 10 fewer than the count at the end of week 27.

Aframax Baltic: Since the end of week 32, there has been a downward trend, with current levels around 22, 10 fewer than two weeks ago.

Dirty tonne days: The decrease in the growth of VLCC tonne days persisted throughout August, signalling a continued slowdown in demand. However, the rate of decline appears to have stabilised, suggesting that it may have reached its lowest point for the summer season. As we move into September, the focus will be on whether weekly percentage growth can rebound, potentially establishing a firmer upward trajectory. This recovery could gradually bring growth levels closer to the annual average, but the market’s response to shifting seasonal and economic factors will be crucial in determining the pace and sustainability of this recovery.

Data Source: Signal Ocean Platform