Tanker - Weekly Market Monitor

Snapshot of Crude and Product Freight Rates, Supply-Demand

Week 28, July 11, 2024

The second week of July has seen a continued weakening in crude oil freight rates. However, there are indications of a potential positive turn in the coming days, as the elevated number of vessels in Ras Tanura for the VLCC MEG-China route has begun to gradually decline. The evolving supply dynamics in the near future will be critical to monitor, especially as demand indicators and the growth of tonne days paint a challenging summer outlook for the freight market.

Meanwhile, OPEC has recently released new insights into oil supply and demand dynamics. The organization maintains its forecast for robust global oil demand growth in 2024 and 2025, driven by resilient economic expansion and a strong rebound in summer air travel. According to OPEC's latest Monthly Oil Market Report (MOMR), global oil demand is expected to increase by 2.25 million barrels per day (bpd) in 2024 and by 1.85 million bpd in 2025, unchanged from its initial forecasts in January 2024. On the supply side, OPEC has also held steady its estimate for non-OPEC+ liquids supply growth at 1.23 million b/d for 2024 and 1.10 million b/d for 2025. Notably, growth in non-OPEC+ supply will be largely driven by the U.S., Canada, and Brazil.

In June, OPEC+ crude production, as reported by secondary sources, declined by 125,000 b/d to 40.8 million b/d. This figure remains 2.3 million b/d below OPEC's projected call on OPEC+ crude.

The downward trend in VLCC MEG-China freight rates persisted for another week, while there appears to be resistance in the Aframax Med route, although rates remain weaker compared to a month ago.

The VLCC MEG-China freight rates have dropped to 46 WS, marking a 13% decrease compared to rates observed one month ago.

Suezmax freight rates for shipments from West Africa to continental Europe have dropped below 100 WS, indicating an 11% decrease compared to levels observed a month ago. Similarly, rates on the Suez Baltic Med route have decreased below 120 WS, but they indicate an 18% increase compared to levels from the same week a year ago.

Aframax Mediterranean freight rates have remained steady, with indications of an increase to around WS160, marking a 26% rise compared to a year ago.

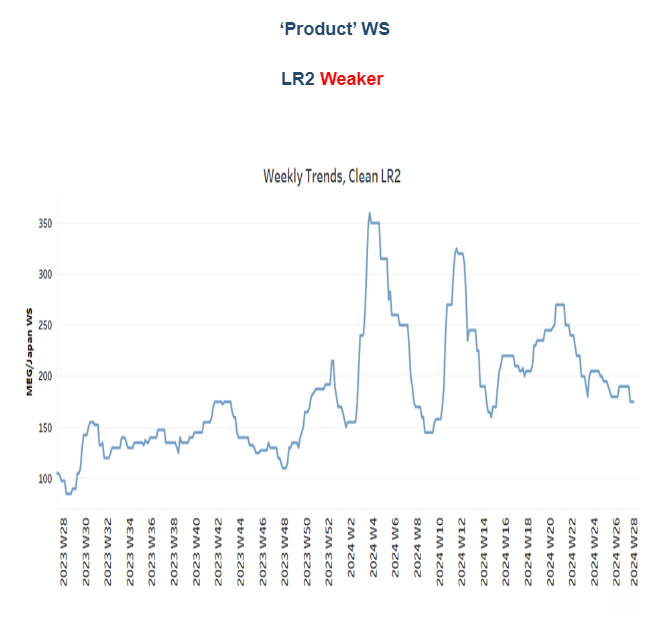

LR2 AG freight rates have dropped to WS180, reflecting a 10-point decrease from rates observed a week ago. Recent sentiment suggests a 7% increase compared to the same week last year.

Panamax Carib-to-USG rates remained unchanged from the previous week, hovering around WS 165, which is 16% weaker compared to rates observed during a similar week last year.

MR1 rates for shipments from the Baltic to the continent have shown weaker momentum since the end of June, reaching nearly 240 WS and indicating an 18% decrease compared to levels observed a month ago. Meanwhile, MR2 rates for shipments from the continent to the USAC climbed to 185 WS, reflecting a 20% annual increase. On the USG-Cont route, MR2 rates eased from last week's peaks to 150 WS, still marking a 30% annual increase.

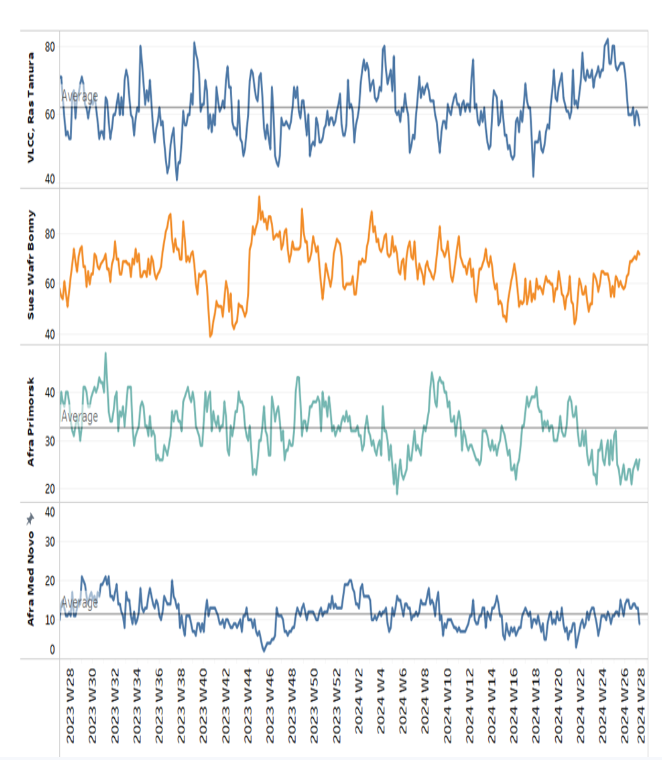

The supply trend for crude tankers at the VLCC Ras Tanura has begun to indicate a decrease below the annual average, while upward pressure persists for the Suez Wafr Bony.

VLCC Ras Tanura: The supply of crude tankers at VLCC Ras Tanura has fallen to 57, which is 5 below the annual average. Notably, the peak three weeks ago surpassed 80.

Suezmax Wafr: The current ship count has risen to 70, marking an increase of 10 compared to the level observed at the end of the previous week. This count is nearly 30 higher than it was six weeks ago.

Aframax Primorsk: For the past five weeks, the number of ships has consistently remained well below the annual average of 30, nearly 10 fewer than the peak recorded at the beginning of week 26.

Aframax Med Novo: Since the end of week 22, the vessel count has consistently hovered around the annual average of 10. Early estimates for the first week of July suggested a slight upward trend, but this was not confirmed in the last days.

Clean LR2 AG Jubail: The downward trend in the number of vessels observed in the last days of June has reversed to an upward movement in the first two weeks of July. The count is now nearing 12, indicating a potential increase above the annual trend in the coming days.

Clean MR: Vessel activity for MR1 at Algeria's Skikda port has increased to 29, marking a rise of nearly 6 from the low observed last week. Meanwhile, MR2 activity in Amsterdam climbed above 40 but has since shown signs of a downward revision to nearly 30, still higher than the low point observed in week 18.

Dirty tonne days: The growth of VLCC tonne-days slowed, though there are signs of a slight upward shift in the second week of July. In the Suezmax segment, early indications of a potential upward reversal at the end of June were not confirmed, resulting in a downward correction in the first half of July. The Aframax segment, which saw a potential upward trend reaching a peak two weeks ago, has since decreased. It remains to be seen how this growth will evolve for the rest of the month.

Panamax tonne days: Despite signs of improvement, growth rates remain significantly weaker compared to the peak observed in week 13.

For Clean MR tonne days, MR1 vessels appear to have reached their lowest growth point and are now gradually recording a firmer pace, although this remains weaker than the growth seen four weeks ago. Meanwhile, the growth in tonne-days for MR2 vessels continues to follow a similar trend as observed in the previous weeks of June

Data Source: Signal Ocean Platform