Dry bulk spot rates were mixed last week, with capesize and panamax rates declining. There has remained a lot to be bullish about in the dry bulk market, though, and structurally we are still just primarily concerned for the capesize market that iron ore exporters could pull back on sales due to the recent plummet in iron ore prices.

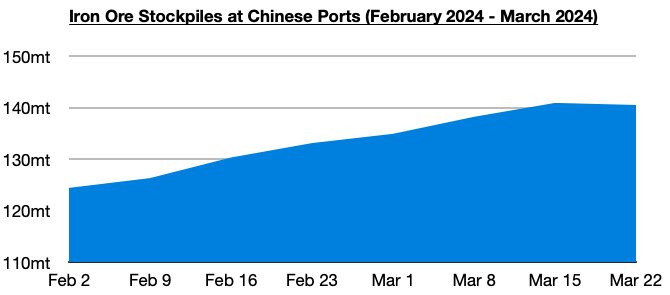

As we have been stressing in Commodore Research's Weekly Dry Bulk Reports, China’s iron ore port stockpile capacity is about 230 million tons. With current levels still at just over 140 million tons, there remains a lot more room to go. Our concern here remains not that China will pull back on buying imported iron ore cargoes, but instead that iron ore exporters will pull back on selling.

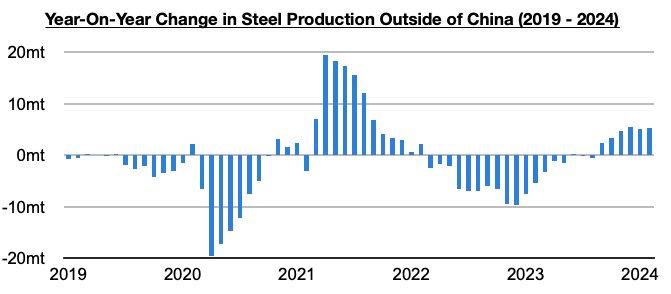

Worth noting in the steel market, though, is that Chinese steel prices finally rebounded last week and steel stockpiles also fell again. Also remaining very encouraging to us globally is that steel output outside of China continues to enjoy a return to growth. Steel output ex-China most recently totaled 67.6 million tons in February. This is 5.3 million tons (9%) more than was reported last year for February 2023’s output. Steel output outside of China has now increased on a year-on-year basis for six straight months.