Energy markets were a touch weaker as tensions in the Middle East eased slightly. Sentiment in the metals sector remains bullish amid supply constraints and a pickup in demand.

By Daniel Hynes

Crude oil edged lower as traders assessed the geopolitical backdrop. Israel said progress had been made in negotiations for a ceasefire in Gaza. However, this was rejected by Hamas. Moreover, Iran’s Revolutionary Guard made a veiled threat, warning it has the option of disrupting trade through the Strait of Hormuz but chooses not to. This should keep the risk of disruption to oil supply high. Meanwhile the broader fundamental outlook remains positive. A new Chinese mega-refinery received an import quota for this year. The volume would equate to about 167kb/d of additional crude import demand. This comes amid an improvement in its manufacturing sector. Sentiment out of the FT Commodity Summit has been bullish. Vitol, the world’s largest independent trader, expects demand growth of 1.9mb/d this year, which is more than 30% higher than IEA’s estimate.

European gas fell after hitting a two-week high as ample inventory levels weighed on sentiment. The weakness across the oil market also weighed on the broader energy complex. However, it’s now in competition with Asia for spare LNG cargoes. North Asian LNG prices have been edging higher in recent days as buyers start to take advantage of the recent price falls. Future supplies may also be tighter, with the US focused on ensuring Russia cannot develop any new projects that would give the country future export revenue. The Artic LNG 2 plant has already begun to close off some gas wells as US sanctions prevent exports.

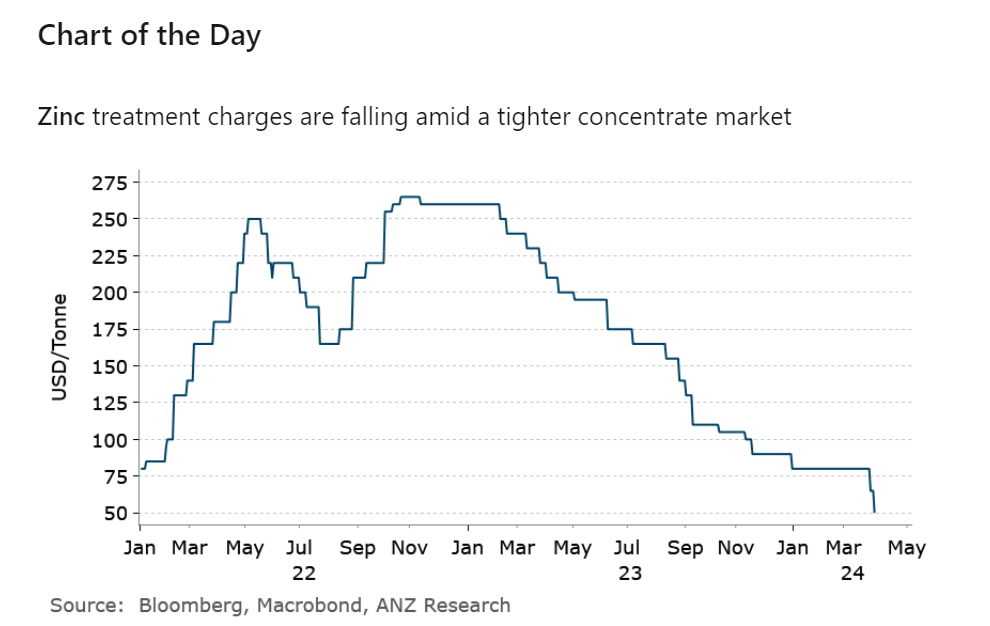

Copper traded near a 15-month high as supply concerns amid brighter demand prospects boost sentiment. Prices are up more than 15% over the past two months as mine disruptions force the Chinese smelting industry to slow down. The same issue is now facing the zinc market, with treatment charges on imports hitting a six-year low. Daily production of refined zinc has already fallen since hitting an all-time high of 22kt in November. Reports suggest many smelters are scheduling out of season maintenance and upgrades, which could impact output further. Lithium continues to struggle to recover from the recent price falls. Miners, refiners and EV battery makers are still working through surplus stock which is clogging up the supply chain.

Iron ore extended recent gains as expectations of a brighter outlook for consumption boosts sentiment. April and May are China’s busiest period for construction. Output from some blast furnaces is already starting to pick up in anticipation. Inventories at Chinese ports have also fallen slightly in recent weeks.

Gold set a fresh record high of USD2,365/oz in a sign the market is expecting lower inflation to trigger a rate cut by the Fed. Heightened geopolitical risks are also providing some support.

Data source: Commodities Wrap