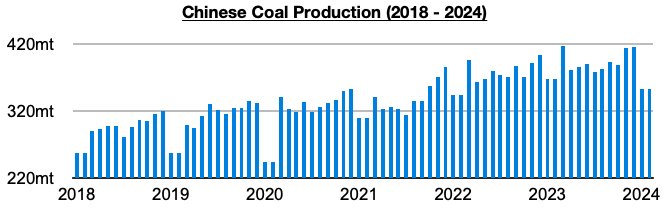

As we discussed in client notes last month and in Commodore Research's March 25th Weekly Dry Bulk Report, China's coal output averaged 352.6 million tons in January/February. This has marked a decline of 61.7 million tons (-15%) from December and is down year-on-year by 14.5 million tons (-4%). Previously, the last time that China's coal output contracted on a year-on-year basis was back in July 2021. The major six-month coal mining safety overhaul that we discussed in our Weekly Dry Bulk Reports and Weekly China Reports last year has been what has led to coal output finally contracting.

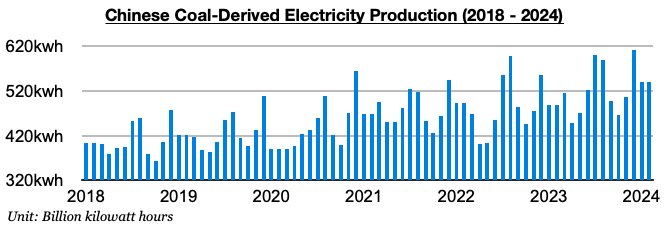

China's coal-derived electricity generation averaged 540.1 billion kilowatt hours in January/February. This has marked a normal month-on-month decline of 70.8 billion kilowatt hours (-12%) from December but is up year-on-year by 52.2 billion kilowatt hours (11%). Remaining helpful for the coal and dry bulk markets is that throughout much of last year and so far all of this year, China's coal-derived electricity generation growth has exceeded coal output growth. This has continued to help support robust coal import demand.

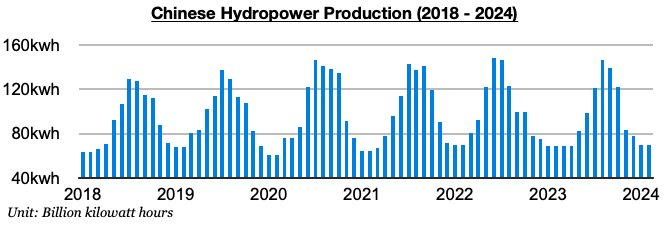

China's hydropower production averaged 69.5 billion kilowatt hours in January/February. This has marked a month-on-month decline of 8 billion kilowatt hours (-10%) but is up year-on-year by 1.1 billion kilowatt hours (2%). China’s hydropower production has increased on a year-on-year basis for seven straight months and remains a headwind in the coal market, but growth has at least continued to slow recently. Last month's 2% year-on-year growth has marked the lowest growth in hydropower production seen during these last seven months.