Dry Weekly Market Monitor - Week 13.2024

Snapshot of Spot Freight Rates, Supply-Demand Trends, Port Congestions

March 27, 2024

In the closing days of March, there has been a discernible softening of momentum in the Capesize Brazil to North China rates, following an upturn recorded in the previous week. Nevertheless, the recent momentum remains notably firmer than levels observed a month ago. Notably, the larger vessel size categories continue to exhibit strength, with a continued decrease in the number of ballasters for Capesize and Panamax vessels in Southeast Asia and Africa. Furthermore, the end of the month has seen a notable uptick in weekly percentage growth for Capesize tonne days.

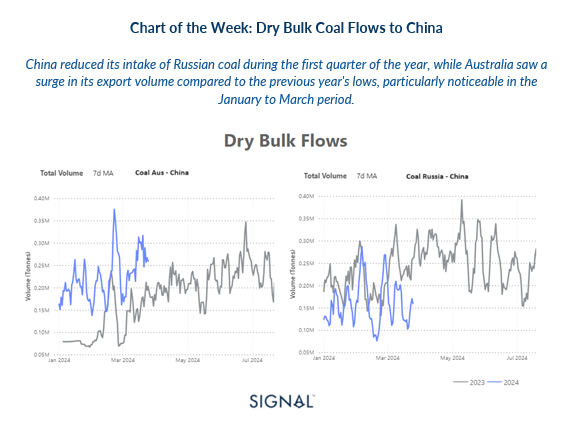

Examining the dry bulk coal flows to China reveals intriguing trends. Russia appears to have reduced its volume of shipments to the world’s second-largest economy, while Australian coal shipments have shown an increasing trend, as indicated by the 7-day moving average depicted in the graph. Meanwhile, the tragic Baltimore Bridge collapse has sparked a wave of logistical concerns over the flow of US coal exports to key markets such as India, China and Europe. This incident has raised concerns about logistical supply disruptions and the impact on a rise in coal prices.

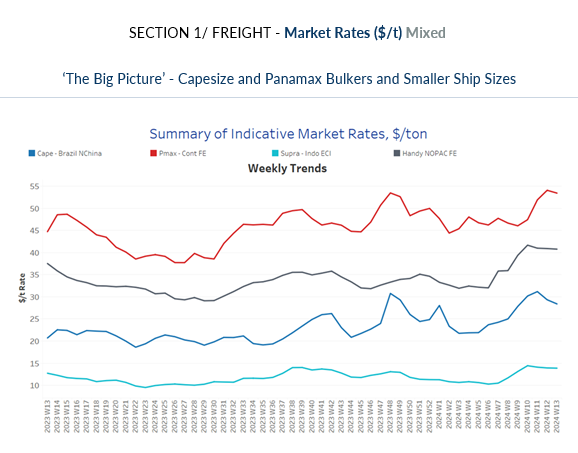

As March draws to a close, the freight market presents a mixed outlook. Sentiment in Capesize Brazil to North China rates has once again experienced a downward revision, contrasting with the steadfastness seen in Panamax Cont Far East rates, which remain firm compared to the previous week.

Capesize vessel freight rates for shipments from Brazil to North China dipped to $28 per ton, marking an 8% weekly decrease. Despite this decline, the current rates reflect a significant 37% increase compared to those observed during a comparable week a year ago.

Panamax vessel freight rates from the Continent to the Far East have maintained their peak, exceeding $50 per ton, signalling a robust rebound in the market. Recent levels indicate a 22% annual increase, painting a promising picture as we approach the end of the first quarter.

Supramax vessel freight rates on the Indo-ECI route have maintained a steady trend around $14 per ton since mid-March, marking a 16% increase compared to a comparable week from a month ago.

Handysize freight rates for the NOPAC Far East route have stayed above $40 per ton for the third consecutive week, reflecting an 8% increase compared to rates recorded during a similar week last year.

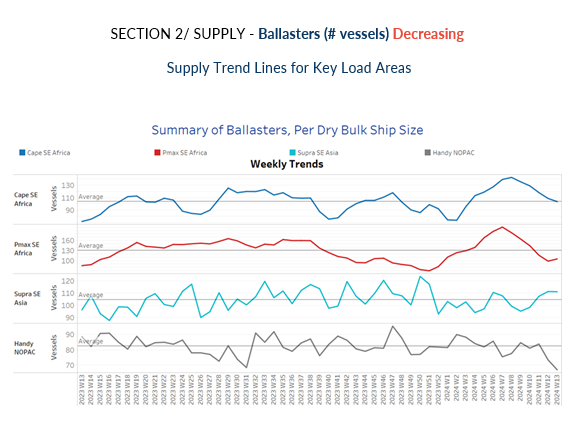

The count of ballast vessels showed a decreasing trend across all vessel size categories except for the Supramax. Particularly noteworthy was the sharp decline in the Handysize NOPAC region, where the number fell below the annual average. In contrast, Supramax vessels have exhibited a consistent upward trend from the lows experienced in week 9.

Capesize SE Africa: The number of ballast ships has dipped close to the annual average mark of 103, nearly 12 lower than the previous week. This decline marks a notable 27% decrease from the peak observed in week 8.

Panamax SE Africa: The count of ballast ships has dropped to 105, maintaining levels below the annual average for the past two weeks. There appears to be a continuing downward trend as we approach the end of the month.

Supramax SE Asia: The number of ballast ships has surpassed the 100 mark, continuing its upward trajectory for the past three weeks. This trend is expected to persist over the next few days.

Handysize NOPAC: The count of ballast ships has fallen below the annual average for the first time since the end of week 8, signalling a trend toward the lowest point observed since the beginning of the year.

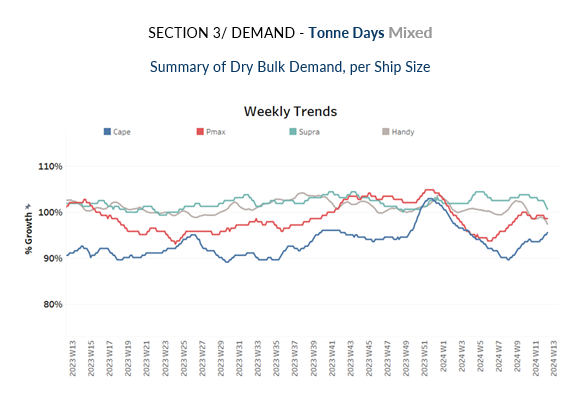

Positive indications for the growth of tonne days for the large vessel size categories, while there is a persistent downward trend in the Handysize and Supramax.

Capesize: Despite indications of a downward trend in the previous week, there was ultimately a positive shift towards stronger growth in tonne days. March gained momentum with a steady decrease in the number of ballasters and improved demand growth.

Panamax: As March nears its end, a positive momentum persists, with the weekly percentage growth of tonne days maintaining a consistent pace compared to the previous two weeks. Moreover, the recent growth remains notably higher than the low points recorded during weeks 5 and 6.

Supramax: The growth rate has shown a further decline, dropping to levels lower than those observed two weeks ago, indicating a weakening momentum as March comes to a close.

Handysize: The growth rate of tonne days has persisted with weakness throughout March, with the recent pace remaining the slowest seen this year.

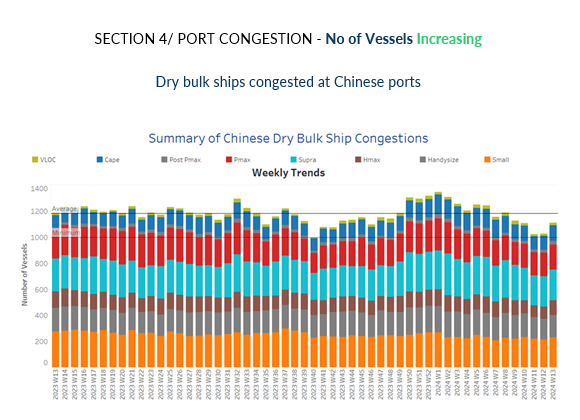

In the final week of March, there was a sudden increase in all vessel size categories following the lows witnessed in the previous two weeks.

Capesize: Capesize ship congestion has risen to 120, marking an increase of 10 from the previous week and signalling a decrease of 40 vessels from the peak observed in week 6.

Panamax: For Panamax vessels, the number returned to around 190, defying the estimates from the previous week that predicted a rise above the 200 mark.

Supramax: Congestion rose to around 240 mark, almost 10 higher than the level recorded in the previous two weeks.

Handysize: Congestion levels settled at around 170, marking an increase of 10 compared to the previous week. Initial indications last week suggested a similar figure, but the number gradually decreased before rising again to exceed 170 once more.

Data Source: Signal Ocean Platform