This week, in the East, we discuss the implications for Aframaxes and Suezmaxes of high crude exports from Sidi Kerir and the fundamentals supporting Pacific MR earnings. In the West, crude tanker mileage declined due to fewer VLCC voyages from the Americas to Asia, and Cross-Med TC6 rates are supported.

By Mary Melton

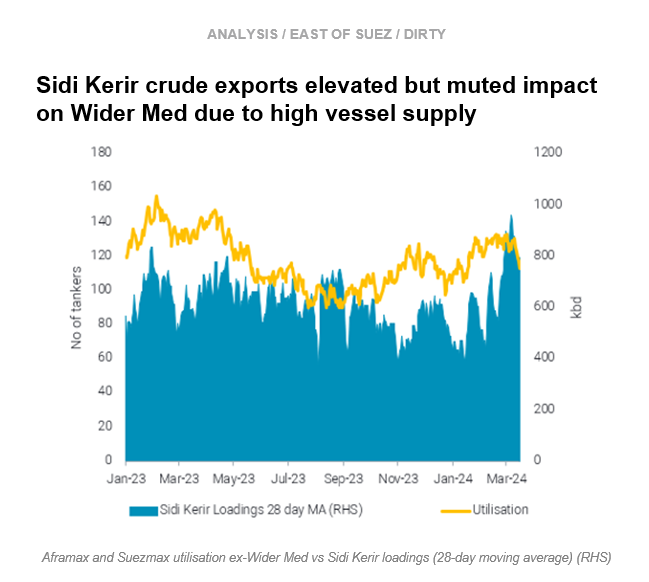

Crude exports from Egypt’s Sidi Kerir remain high so far in March, following on from a multi-year high in February. Rising exports from the Med port are a function of Middle East (mostly Saudi) crude flows along the SUMED pipeline which is regularly fed by the Red Sea port of Ain Sukhna.

Increased exports from Saudi Red Sea port of Yanbu to Ain Sukhna suggest loadings from Sidi Kerir are likely to remain high for the near future, boosting a currently fading Afra/Suezmax employment from the wider Med.

On the supply front, Afra/Suezmax tanker availability in the Med remains high despite high Sidi Kerir loadings, because employment opportunities elsewhere in the Atlantic Basin are limited as European refinery maintenance is underway.

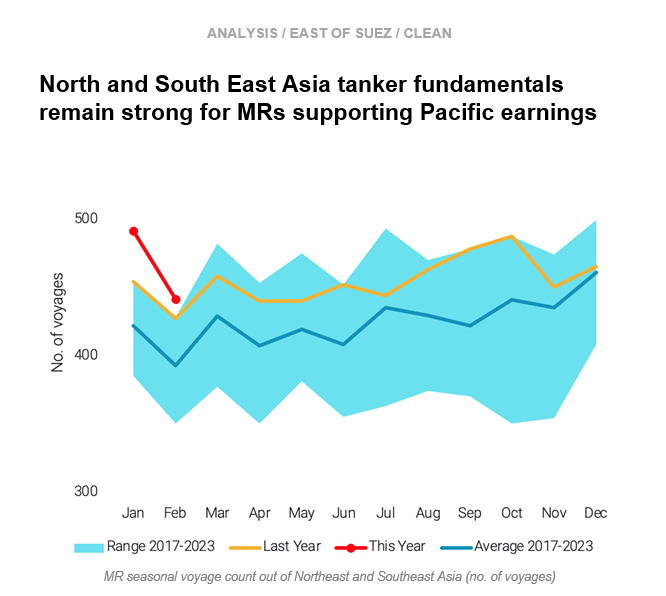

MR tankers operating in the Pacific have lately seen elevated freight rates, which is driven by both supply and demand-side fundamentals. On the supply-side the tonnage flow rigidity imposed by limited Panama Canal transits has left the Pacific Basin overall undersupplied when compared with the Atlantic.

Looking at demand, even though voyages for MRs out of Northeast and Southeast Asia dipped m-o-m in February, these were still maintained above historical norms due to an increase in regional flows amidst a shut East-West arbitrage and expensive long-haul freight due to Red Sea attacks.

Nevertheless, zooming in Southeast Asia, TC7 Singapore-to-East Australia freight rates marked a decline due to a pick-up in available vessels over the past week. This week our dataset indicates a decline in the tonnage list once more, which could propel a bounce back.

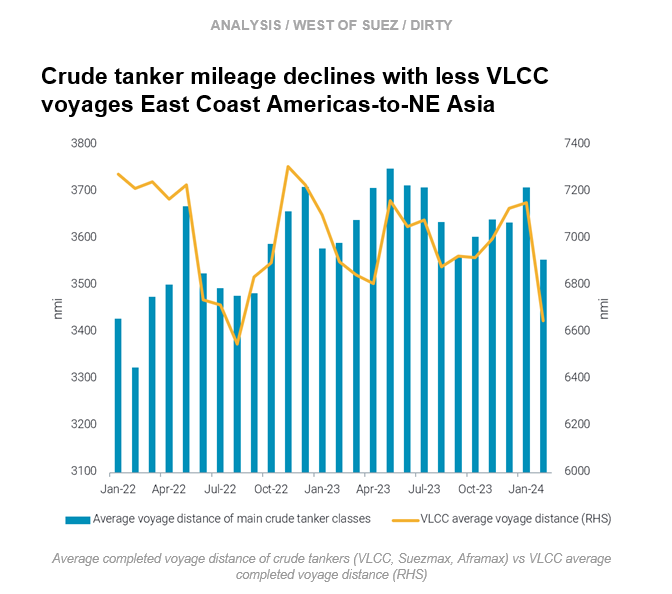

Average laden completed voyage mileage for the main crude tanker classes (Aframax, Suezmax, VLCC) declined 4.2% m-o-m in February. VLCCs saw the most declines in average mileage, at 7.1% m-o-m, while Aframax and Suezmax mileage remained relatively flat m-o-m.

Declines in VLCC mileage resulted from less cargoes originating in the East Coast Americas (USG and East Coast South America) arriving in Wider NE Asia in February. The voyage count decreased 35% m-o-m, significantly weighing on global VLCC mileage. NE Asia sourcing less crude from the Americas is likely to continue, as Saudi crude OSPs may prove attractive to Chinese buyers.

For Aframaxes and Suezmaxes, average mileage for Russian crude voyages actually increased about 8.3% m-o-m, partially driven by more voyages from Baltic/Black Sea ports to China. However, moving forward signs of lessened employment prospects for the fleet trading Russian crude will likely affect global laden mileage for the vessel classes.

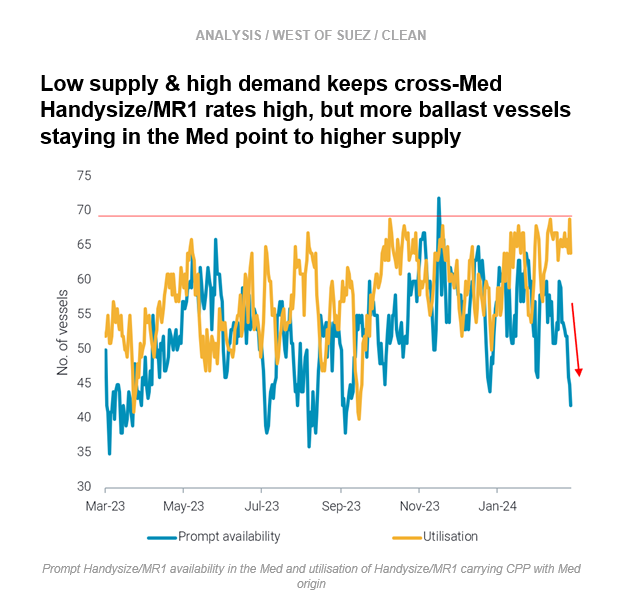

Cross-Med rates (TC6) for Handysize/MR1 have been on an uptick since early February, and are currently at four-month highs. Prompt availability near one-year lows coupled with tanker utilisation around one-year highs drove the increase in rates.

Higher loadings amid the Med’s refinery maintenance are fuelling the demand side momentum, especially higher loadings on Handysize/MR1 tankers from Italy. Importers in the region are likely building stocks in anticipation of reductions in CPP exports.

On the supply side, availability within natural fixing windows is fairly low, but tankers are staying in the Med after discharging, pointing to the possibility of headwinds to TC6 rates if demand fails to materialise as refinery turnarounds continue in the region.

Data Source: Vortexa