Despite a partial lifting of sanctions against Venezuela in October last year, the US is now set to reimpose sanctions on the country’s oil industry in April, due to insufficient progress towards holding free and fair presidential elections; a key condition of sustained sanctions relief. The original deal which was to last for a period of six months, saw the return of Venezuelan crude to the mainstream market and an increase in cargo liftings by largely non dark fleet tankers as traders and charterers became confident in lifting Venezuelan barrels once again.

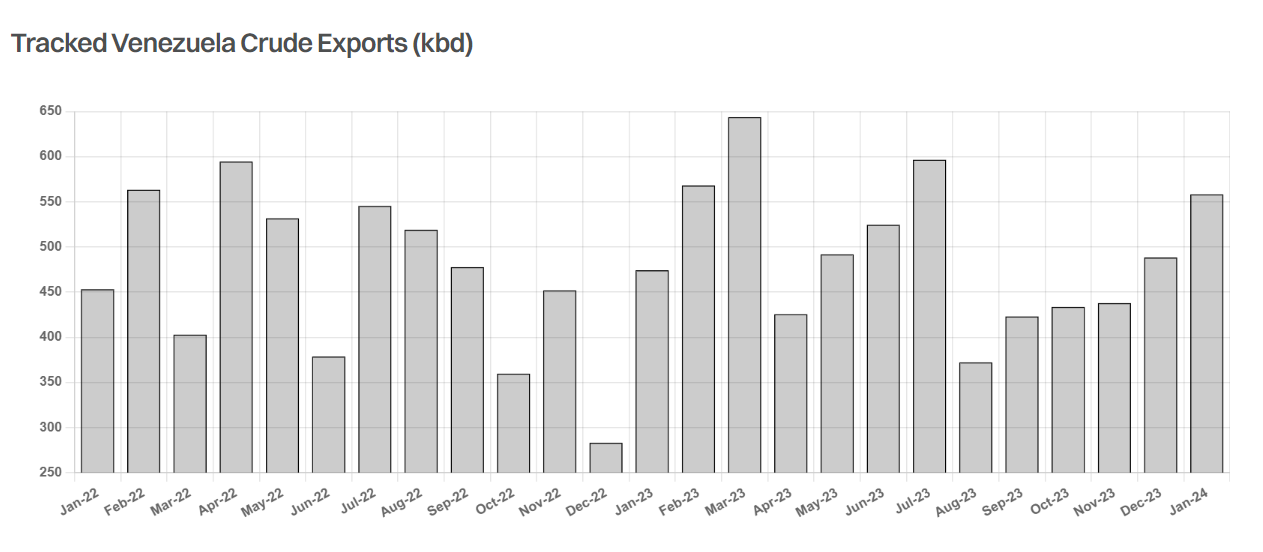

During this period, Venezuelan crude exports have increased but there remains some ambiguity. According to the AIS data, flows have averaged 470kbd over the past three months compared to 370kbd between August and October, whilst the market also saw the return of buyers in India. However, the true level remains opaque, and the actual figure is probably higher than tracked cargo flows, especially to the Far East. A return of Venezuela to the sanctioned market will support the dark fleet once again as mainstream tankers re-exit this trade.

In terms of production, the IEA estimated flat output in December versus November at 800kbd. While PDVSA has signalled its intention of increasing production from present levels, this is likely to prove challenging given current production difficulties and the need to repair existing infrastructure as well as bring fresh investment online. If the country is to head back into a sanctions framework, this will add further complexity in reaching higher output levels given the difficulty of securing international support and investment outside of the nation’s close allies and partners and what has already been provided by Iran, Russia, and China.

However, recent developments related to both the opposition primary elections where the primary winner Maria Corina Machado has been barred from holding public office and the result declared illegitimate. Along with a criminal investigation launched into the primary organisers, this puts into question the prospects of the upcoming Presidential election scheduled for 2024. All of which would have likely added pressure to the deal at a later stage, had the US not announced ending this period of sanctions relief.

Additionally, pressure came towards the end of last year from a December 3rd referendum to annex the Essequibo region of neighbouring Guyana. The results and validity of this referendum have been called into question by the international community, particularly the US, given poll numbers and reported voter turnout figures. This led to an increase in Venezuelan military activity on the border, and an executive order from President Maduro to begin oil, gas, and mineral exploration in the disputed zone. Although recent weeks since have shown a cooling of tensions and commitments to a dialogue instead of force between the countries.

These issues mean Venezuela is now set to rejoin the sanctioned oil market alongside Russia and Iran. Although it is important to note that the US government has left the option open for the Maduro regime to recommit to the original deal, there appears little indication of a significant improvement which would warrant a reversal of the US government’s decision. These developments show the potential fragility of oil sanctions relief deals as well as ongoing US commitment to upholding the other end of the deal in such a case.

Given current oil prices, it is clear that the Biden Administration does not currently feel the pressure to ease sanctions in order to lower fuel prices. This suggests that going forwards, the US is unlikely to make compromises in order to obtain sanctions relief on Iran and Russia, ensuring a large black oil market remains for the time being.

Data source: Gibson Shipbrokers