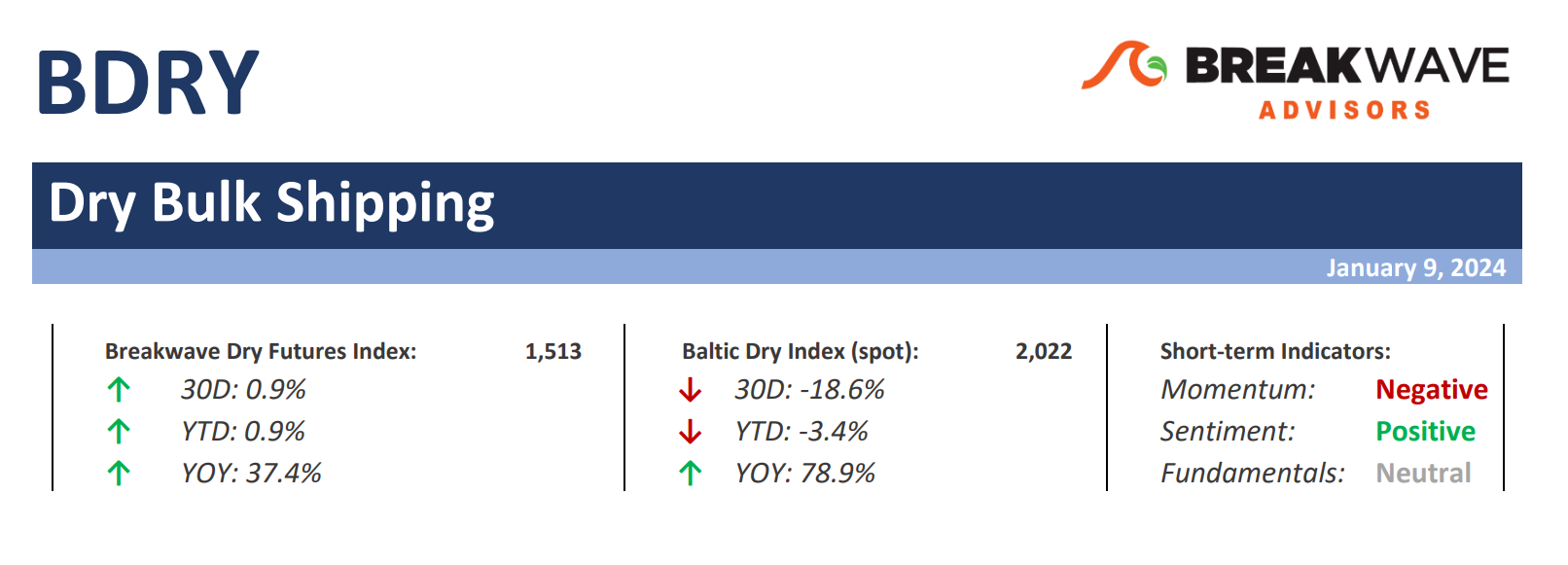

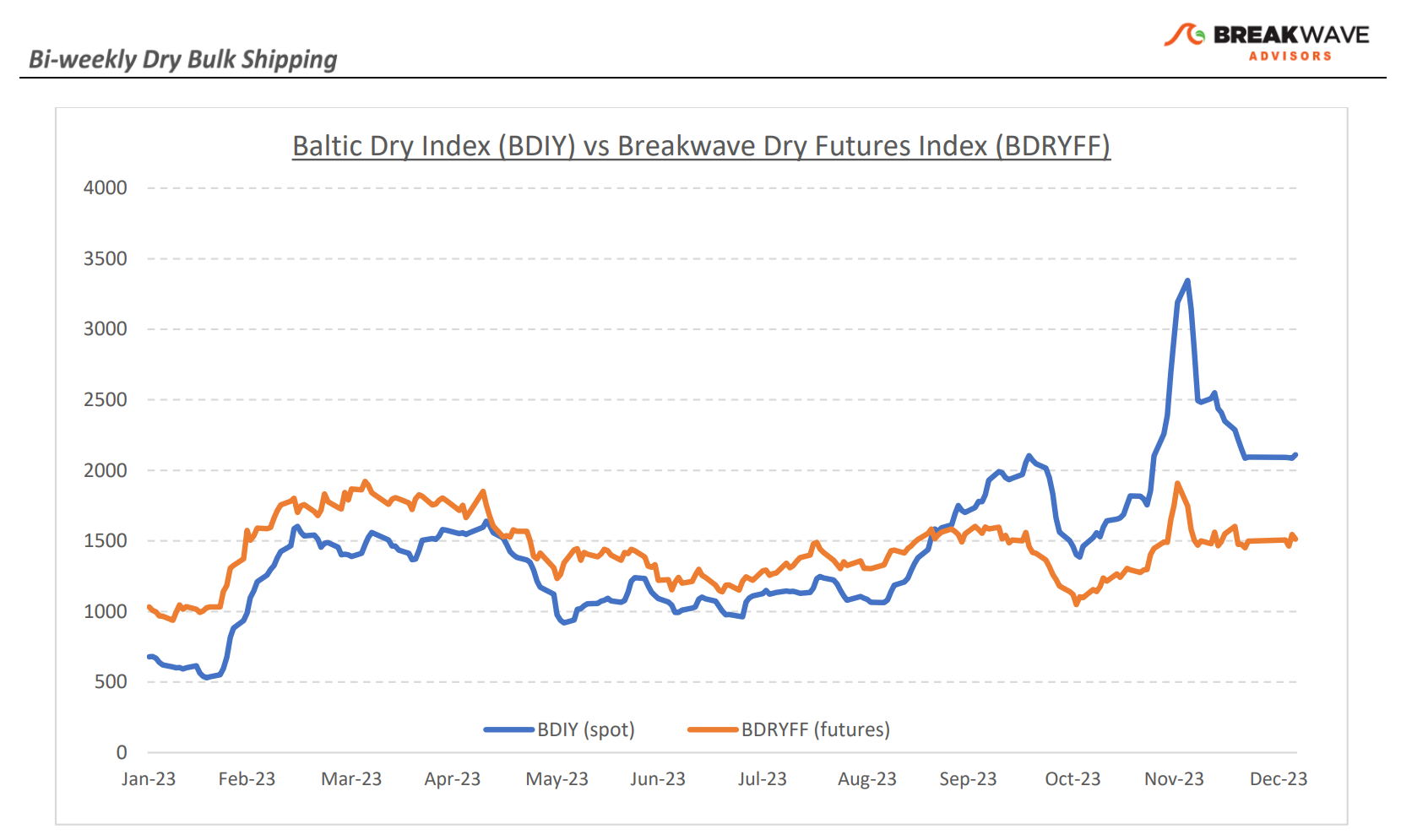

• Despite winter blues, expectations remain high – The first week of the New Year saw limited action as it relates to Capesize fixing. Geographically the tables have turned, with the Pacific spot market having weakened materially to below 20,000 while the Atlantic remains short in tonnage, at least for the month of January, with the respective spot rate sitting above 40,000 for the N. Atlantic routes. Yet, the futures market indicates significant deterioration in the spot average, and although the element of surprise is always at play, we believe this time around it is the spot market that will trend towards futures rather than the other way around. With first quarter contracts indicated at the highest level in more than a decade, and with the full 2024 implied average just short of 18,000, this is not by any means a loss of confidence. Rather, it is a natural progression of the seasonal cycle, reflecting weather patterns (i.e. rain season in Brazil, cold weather in China, potential cyclones in Australia) leading to lower demand for bulk transportation. What is impressive though is the confidence of the market for a strong year ex-Q1, with the implied 9-month Capesize futures sitting at almost 20,000. Although we believe most of the recent increases in spot rates reflect weather-related issues (and some Red Sea disruptions) it seems that the futures market sees improved underlying demand/supply balance for the year. For now, a lot of the potential Q1 decline is priced in the curve, so the spot has a lot of work to do to reach the low teens that the futures market implies in the next 2-3 weeks’ time.

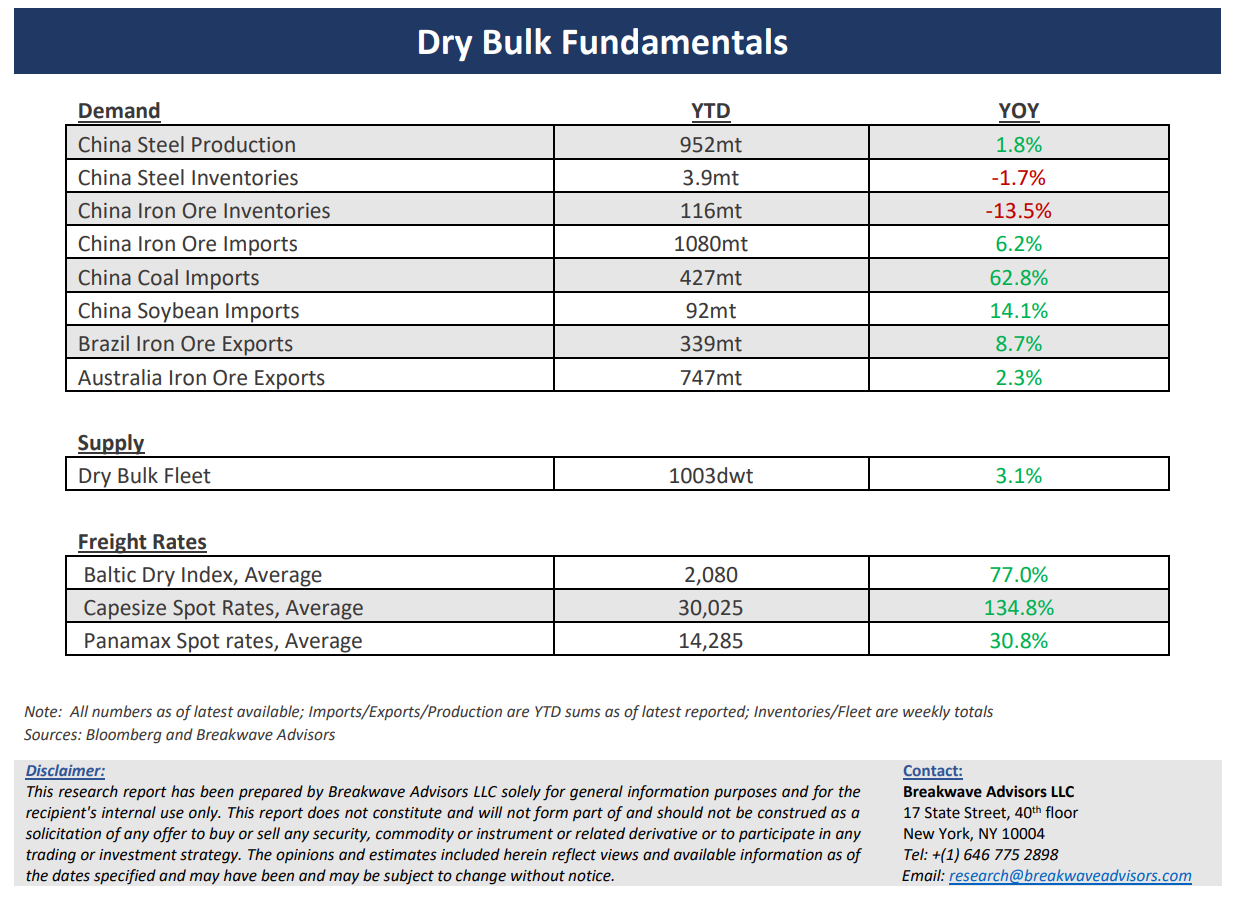

• Chinese steel demand declines as seasonality kicks in – As winter weather settles in the Northern hemisphere, Chinese steel demand has experienced a significant deterioration, recently reaching multi-year lows. Iron ore prices remain firm, anticipating a recovery in demand (as well as tight inventory levels) and once again attention turns to the Chinese government policy as it relates to the real estate market and the broader consumer economy in general. Last year was characterized by numerous policies enacted towards stimulating the economy, but so far, nothing has really had a major impact on economic activity, with PMI numbers remaining in contraction territory and with housing prices trending bottom. Optimism remains high, but evidence is scarce, and although the commodity markets react positively to every piece of news that point to a recovery, we remain skeptical of the ability of China to materially alter the path of the real estate market to any great extent in the foreseeable future. With the Chinese New Year ahead of us, all eyes will soon turn to the annual parliament meeting in March and the signaling from the policy makers as it relates to the future growth targets for the broader economy.

• Our long-term view – The last few years have been characterized by increased geopolitical uncertainty. Going forward, we expect such events to continue to affect global trade and have a meaningful impact on effective vessel supply. Combined with the potential for a multi-year rebound in China’s economic activity, dry bulk shipping should experience higher volatility on top of a secular tightness driven by increasing bulk commodity demand and a slower fleet growth as a result of a relatively low orderbook.

Subscribe: