Examining the current state of seaborne trading in the Red Sea today & assess its influence on freight rates

In recent days, discussions have intensified about the potential impact on the seaborne trade and ton-miles due to the evolving dynamics of market spot rates in various shipping segments. The recent attacks by the Houthi rebels in the Red Sea have already started to significantly affect trading activities, especially in the container segment.

With the start of the new year, the crisis now appears to be impacting Red Sea vessel counts in the crude tanker segment, while spot rates in the Atlantic routes have spiked and piqued the interest of the market, signalling an escalation of the crisis with daily occurrences of new attacks.

In the dry bulk segment, the market has not experienced a significant impact yet. However, as time progresses, the threat of Houthi attacks on both dry and wet seaborne trade appears to be escalating. Figure 1 below, examines which segments were the most exposed to Suez canal crossings in 2023. Suezmax and Aframax and Supramax and Panamax represent more than half of the total crossings in tankers and dry bulk respectively.

Figure 1: % of Voyages that ended in 2023 with a Suez canal crossing per Vessel Class, Tanker & Dry

Using Signal Ocean data, it becomes quickly clear that if we want to look for the most affected trades we need to start with the crude oil Suezmax and Aframax trades and the agricultural commodities transported with Panamax and Supramax dry bulk vessels.

But what happens if the effects already clearly felt in container traffic begin having a deeper impact on wet and dry bulk commodities too? The obvious ramification, namely the detour of ships via the Cape of Good Hope can certainly increase further, even beyond 50%, as we are increasingly encountering and anticipating announcements of suspension of shipments via the Red Sea.

Several major shipping companies have already announced the suspension of shipments, while more are saying they are closely monitoring the situation and are about to make a decision. The shipping associations BIMCO, ICS, CLIA, IMCA, INTERCARGO, INTERTANKO and OCIMF have already issued joint guidelines emphasising the importance of a relevant hazard and risk assessment. This includes considering additional advice from the ship's flag state before transiting the area in question.

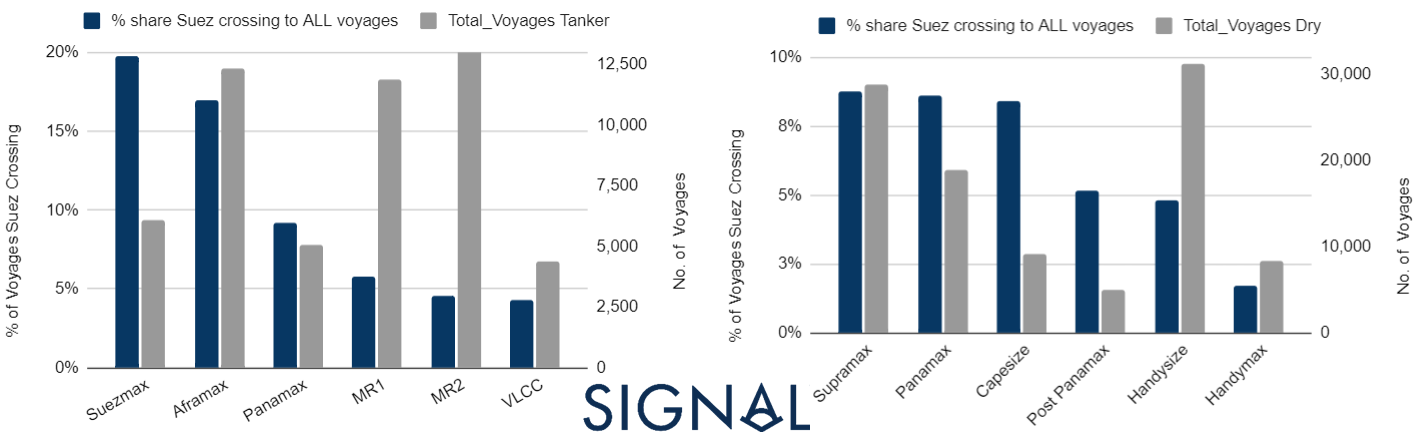

So how much would the various vessel classes be affected if suspension of crossings escalate? We begin looking for an answer by inspecting the exposure of each class to the relevant routes. In Figure 2, we can see the percentage of voyages with a Suez canal crossing for each vessel class and the total number of global voyages. Almost one in five of the approximately 6,000 global voyages for Suezmax crossed the Suez canal in 2023, for example.

So, not only do Suezmax and Aframax tankers, together with Supramax and Panamax Dry, dominate the canal’s time, but it appears that crossing it happens while serving a very substantial part of the total global ton-miles for the trades these vessel segments serve.

Figure 2: % of voyages Suez Crossing ending in 2023 to Total Voyages, per Vessel Class, Tanker & Dry

To read the full article please click on the button below.