Chart of the Week: Dry Bulk Coal flows from India

Brazilian iron ore export volumes increased in August, leading to a boost in Capesize tonne days

Throughout the last week of September, freight rates maintaining the strength observed in previous days. It appears that the third quarter will conclude with higher freight rates than those witnessed in the preceding two months. Notable increases were seen on a monthly basis in the freight market for large vessel sizes, particularly in the Capesize West Australia to China route and the Panamax Far East RV.

There was also a robust sentiment in the Supramax category for the Continent-USG route, while the Handysize segment saw positive developments in the Continent-Brazil route. Moreover, a boost in the freight market sentiment was received from increased coal volumes originating from Indian exporters, reaching various global destinations (see image above). However, it is anticipated that September will conclude at a slower pace compared to the peak levels of August.

An intriguing prospect lies in the evolution of freight rates for October, as the onset of the winter season may affect the energy demands for coal in Asian markets. This could potentially prolong the firmness of freight rates in the Panamax and Supramax vessel size categories.

In the Capesize segment, September witnessed a gradual rise in rates, primarily driven by higher volumes of iron ore shipments from both Australia and Brazil. However, there are still challenges in the market due to an excess of ballast vessels. The decrease in pace that occurred in the final days of September showed some improvement compared to the beginning of the month.

For more information on this week's trends, see the analysis sections below:

Freight Market, Supply, Demand and Port Congestion

SECTION 1/ FREIGHT

‘The Big Picture’ - Capesize and Panamax Bulkers and Smaller Ship Sizes

Market Rates ($/t) Firmer

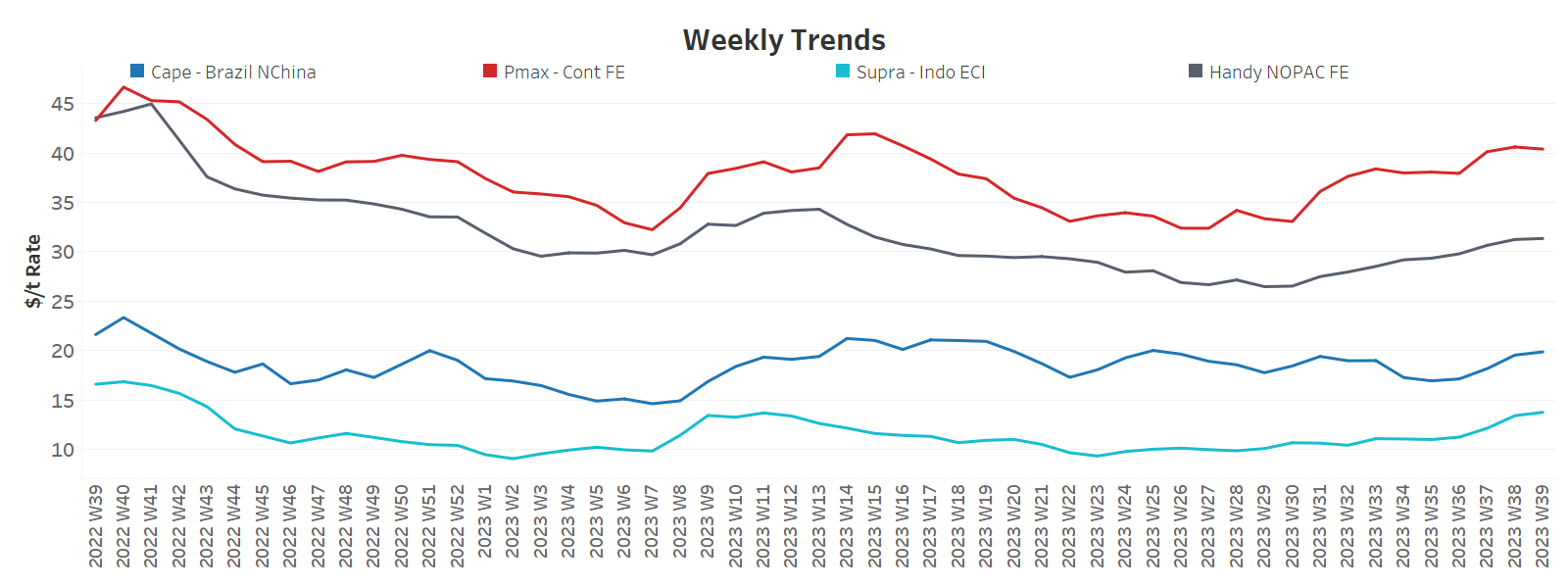

The sentiment in the freight market has improved across all vessel sizes since last week, as shown in the above image for specific routes.

Capesize vessel freight rates from Brazil to North China rose to almost $20/ton, marking a 6% weekly increase and 18% monthly gain.

Panamax vessel freight rates from the Continent to the Far East remained unchanged at $40 per tonne, having peaked after three weeks of consecutive increases. Currently, rates are showing an 8% monthly increase.

Supramax vessel freight rates on the Indo-ECI route increased by 10% per week, reaching $14 per tonne. Rates for this month have risen by 27% compared to the same week in September.

Handysize freight rates for the NOPAC Far East route rose to $30/tonne, up 6% from a month ago.

SECTION 2/ SUPPLY

Supply Trend Lines for Key Load Areas

Ballasters (# vessels) Decreasing

The number of ballast ships shows a decreasing trend, especially in the Capesize segment.

Capesize SE Africa: The number of ballasters dropped to 100, which is 22 vessels less than six weeks ago.

Panamax SE Africa: The number of ballasters held levels of the previous week at around 160, with a tendency of a further decrease at the end of the month.

Supramax SE Asia: The number of ballast ships dropped to 112, four less than the previous week. It seems that the 38th week was the peak of September.

Handysize NOPAC: The number of ballast ships has fallen below 90, which is still above the annual average of 80.

SECTION 3/ DEMAND

Summary of Dry Bulk Demand, per Ship Size

Tonne Days Mixed

There seem to be the first signs of a recovery in the Capesize, while a downward revision persists in the Supramax and Handysize segments.

Capesize: Demand growth in tonnes per day seems to have found a slightly higher pace of growth since the end of the previous week.

Panamax: Growth rates appeared to be relatively stable, with similar momentum to previous weeks in September and beyond.

Supramax: The last week of September confirmed the sharper decline of the previous weeks, and there are still no signs of an imminent recovery.

Handysize: The growth rate of demand has declined significantly from the previous week in September, with weak momentum in September, although prices showed stronger levels than a month ago.

SECTION 4/ PORT CONGESTION

Dry bulk ships congested at Chinese ports

No of Vessels Increasing

The level of ship congestion increased in late September due to the Supramax and Panamax vessels.

Capesize: The number of congested ships decreased to 104, down by 2 from last week, and the trend is still holding lower than at the start of the month.

Panamax: The number of congested ships decreased to 179, the first time it's been under 200 since week 35.

Supramax: The number of ship congestion reached 280, about 30 ships more than a week ago.

Handysize: The number of congested ships stood 186 from a low of 167 in week 34.

Data Source: Signal Ocean Platform