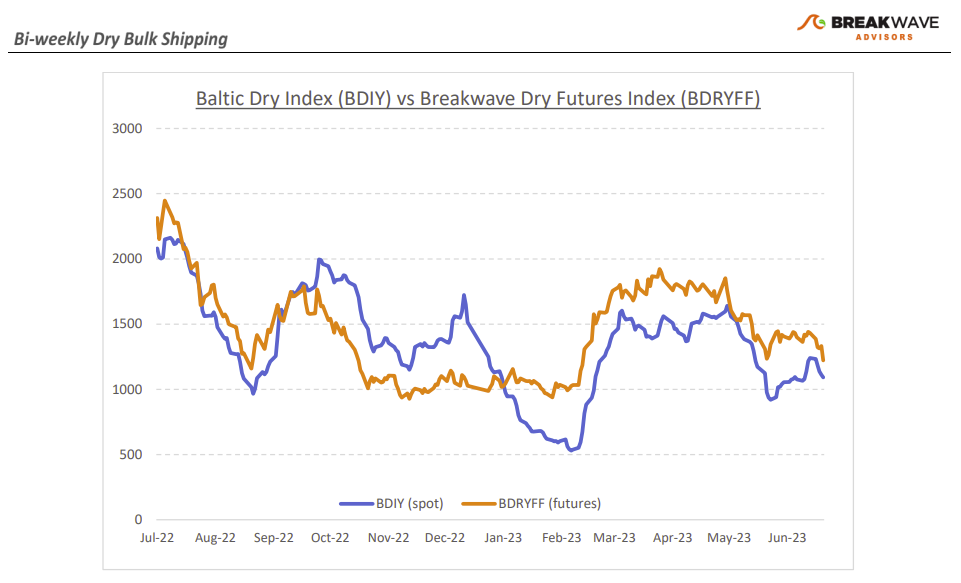

• Dull days usually translate to lower rates as fleet efficiencies prevail – Despite the fact that trade volumes remain strong when it comes to major bulks, the absence of any disruption across the major shipping lanes has translated to lower spot freight rates across the spectrum. This is anything but surprising given that without a tightness in a major shipping hub, demand for spot ships naturally declines as shippers favor dedicated tonnage. Iron ore volumes from both Brazil and Australia have been high, especially versus last year, but once again, dedicated tonnage and prearranged deals have smoothened out the shipment schedules. As we entered the summer months, activity out of West Africa will gradually wane out due to weather, leaving only Brazil as the dominant exporter in the Atlantic basin. Without competition, we expect relatively stable exporting rates, and thus, a steady freight rate environment in that part of the world. In the Pacific, Capesizes have been quite active as of late, and although demand remains strong for iron ore cargoes to China, once again, we are looking for potential disruptions to cause a tightness in that market before any meaningful turnaround in rates. Furthermore, Sub-Cape rates are now back to pre-Covid run rates, having declined considerably in the last 18 months. Overall, the macro picture will play a major role on how the market develops, but without a change in the pace of trade, the main thing bulls have going for is the very low absolute level of spot rates that could potentially translate to high percentage increases when the time comes.

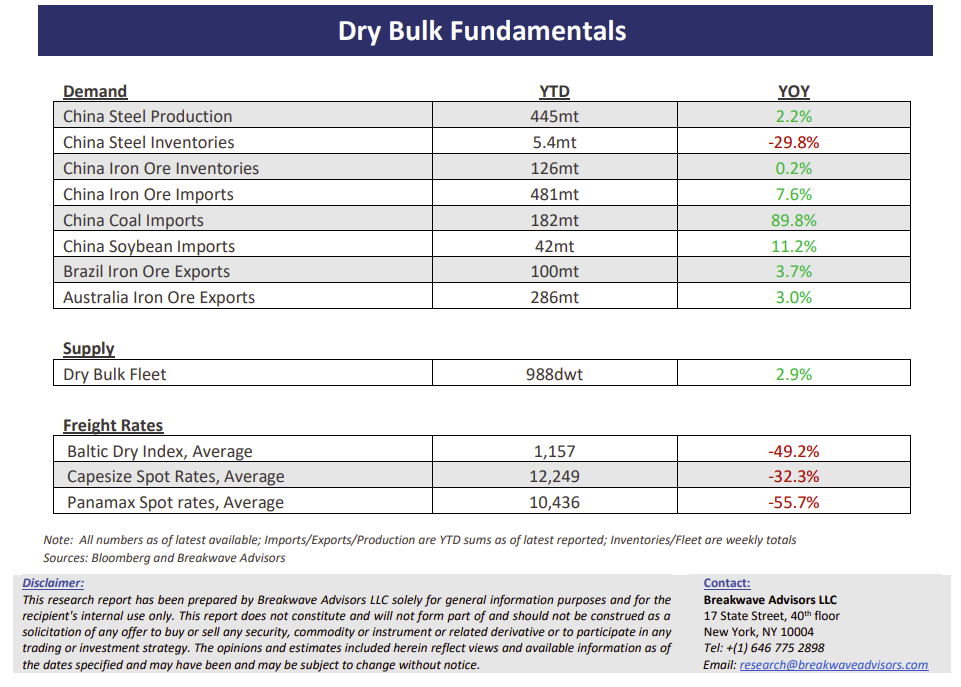

• China’s first half of 2023 was uninspiring – Despite the early hopes for a significant economic recovery, the first half of 2023 has proven lackluster, to say the least, when it comes to economic activity out of China. Although the y-o-y headline numbers look decent, with GDP growth above 5% so far this year, one has to remember that the base effect exaggerates such growth given China’s 2022 GDP growth of just 3%. If the rest of the year does not pick up, the “real adjusted” economic growth in China is more like 3%-4% when one considers last year’s “recession-like” activity. The resulting impact on commodities is naturally disturbing, especially once we account for the hard-hit real estate sector where metrics remain at recession-like levels with little signs of an impending rebound (a recent example being the very weak home sales for Tier 1 & 2 cities). With voices for more stimulus getting louder by the day, will the centrally controlled economy act accordingly and perform better in the second half? Once again, our confidence for a major stimulus package remains low given the constant signaling by officials for ”quality growth” but also the limited scope in terms of size due to the elevated local government debt levels.

• Dry bulk focus shifts back to fundamentals – Following a period of high uncertainty and significant disruptions across the commodity spectrum, the gradual normalization of trade is shifting the market’s attention back to the traditional demand and supply dynamics that have shaped dry bulk profitability for decades. As effective fleet supply growth for the next few years looks marginal, demand will be the main determinant of spot freight rates with China returning back to the driver’s seat as the dominant force of bulk imports and thus shipping demand.