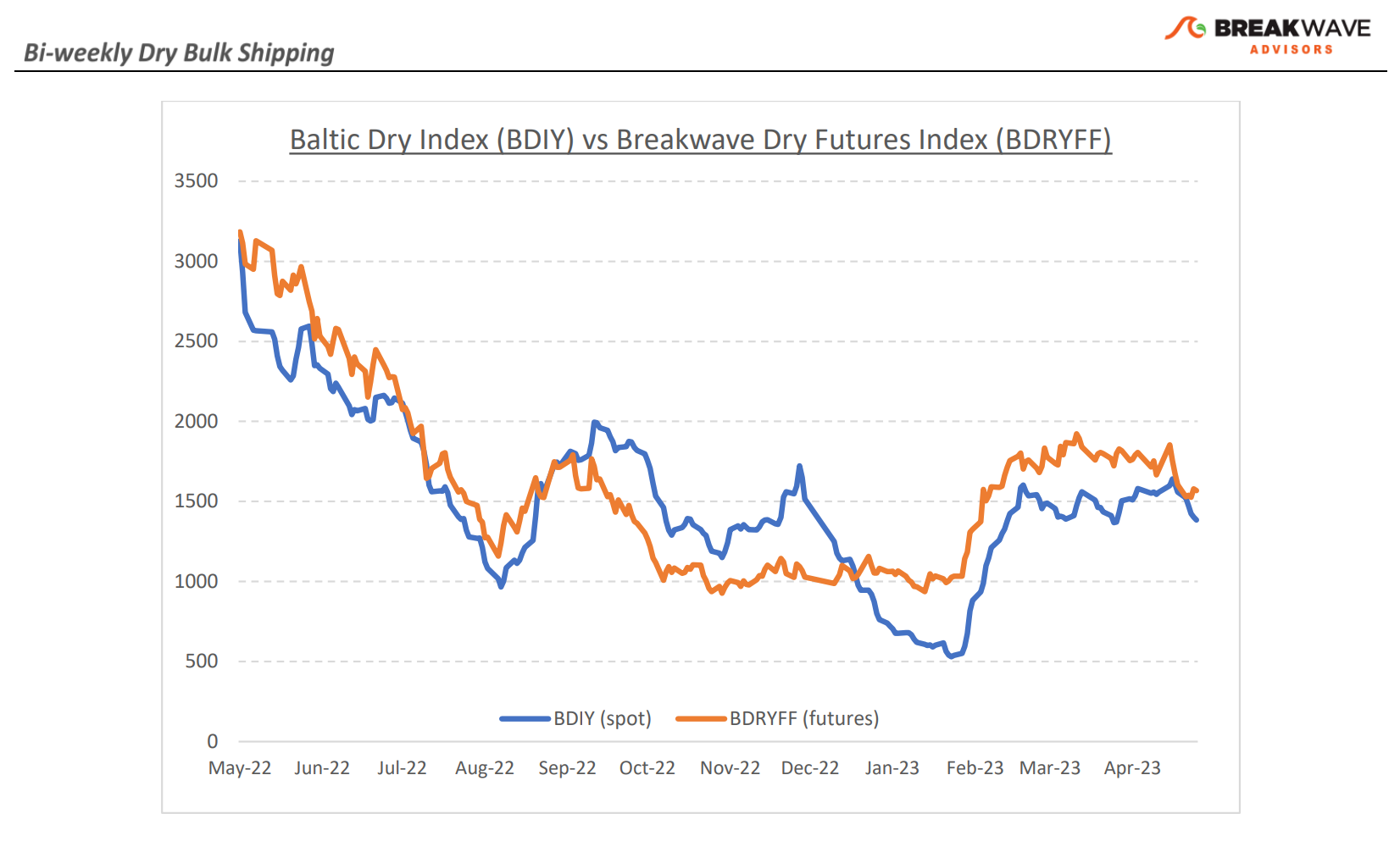

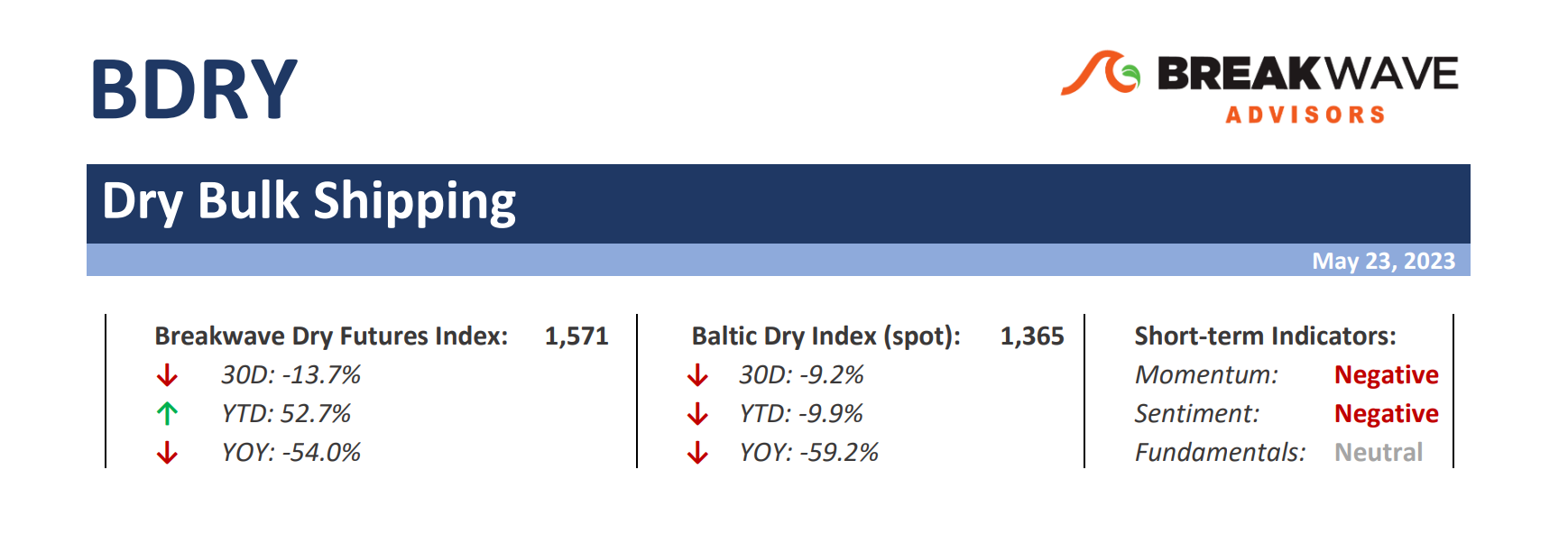

·Freight futures contango evaporates as optimism turns into caution – Not much has changed in the spot market during the past few weeks, yet Capesize futures took a dive and have now erased any premium that was present over the last few months. Although spot rates are trading above mid-April levels, futures are some 20% lower than the comparable period. Clearly sentiment has turned sour, as across the commodity spectrum the relatively weak numbers out of China has taken a toll on any optimism relating to an imminent rebound in activity in that part of the world. Furthermore, the sub-Cape segments remain particularly weak (although versus pre-Covid spot levels are quite comparable) which also weighs on the overall sentiment for dry bulk shipping. What is the potential for dry bulk rates in the near term? On the positive side, the flattening of the futures curve is positive as it has neutralized any option premium previously embedded in the curve: from here, any movement in spot rates should be reflected almost instantly on the futures curve, thus providing a better entry point for investors. In addition, seasonally, June has been a positive month for dry bulk more times than not, and given the fact that in the last three months not a lot has happened in in the spot market, the chances of an early summer rally still look good. On the other hand, the sub-Cape sector has now weakened quite a bit as demand for both coal and grains transportation is soft, and there is little evidence that those smaller size ships are about to experience an imminent turnaround.

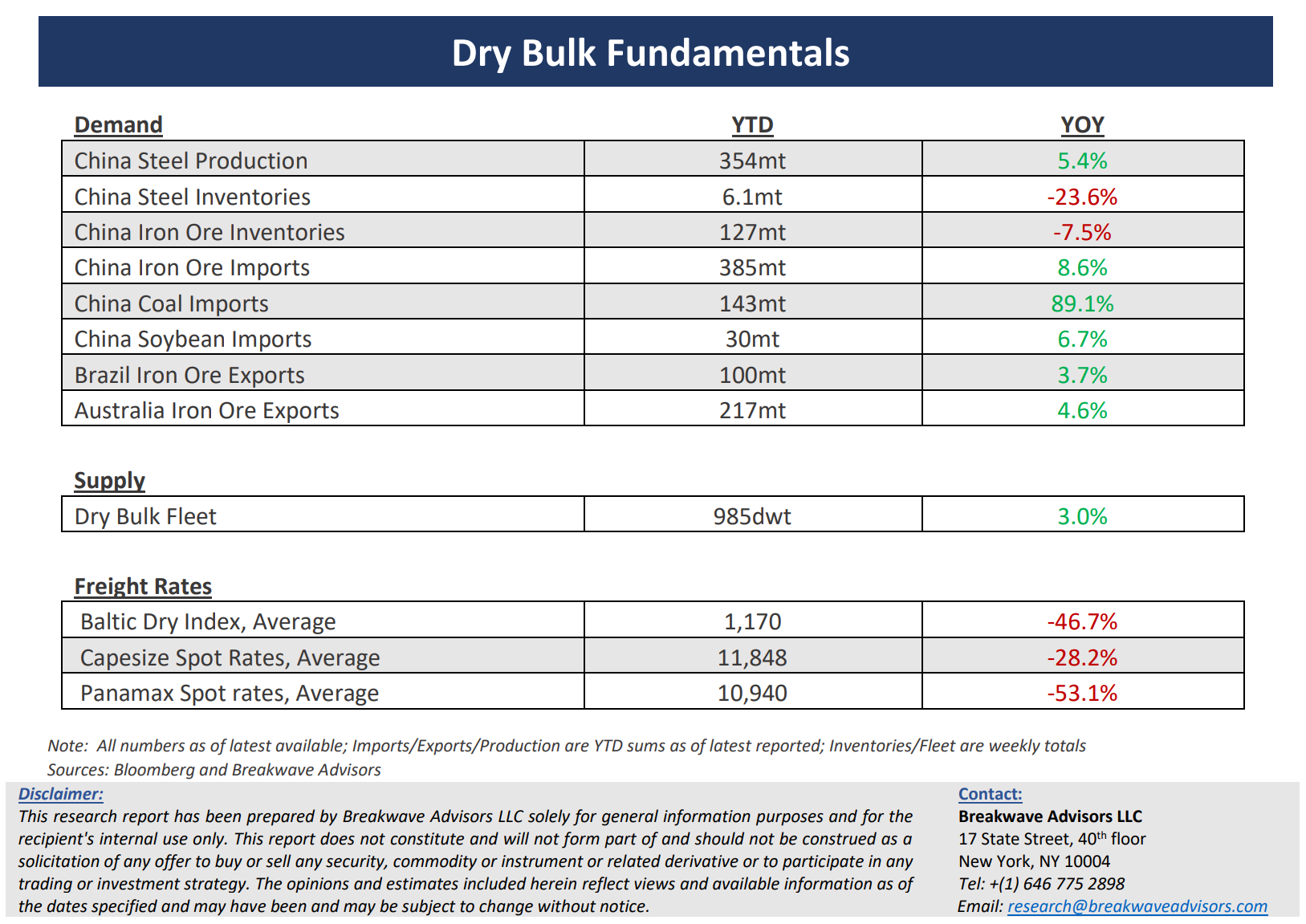

·Chinese data remains stagnant while Beijing is reluctant to add more liquidity – Chinese economic data is running out of steam, even though almost all the pandemic constraints have now been lifted. Commodity prices, that had initially rallied on hopes of a rebound, have been under pressure, reflecting the stagnant demand recovery. Make no mistake, there is considerable credit availability around, which historically should have translated into better demand. However, this time sentiment seems to be the main hurdle, and not liquidity. In the real estate sector, that accounts for some 20% of the overall economy, there have been limited positive developments, mainly reflecting stabilization rather than a rebound. Although the government has already lowered interest rates quite a bit, which haver also driven the Chinese Yuan to relatively low levels (a positive for commodity demand), the need for more direct government intervention to boost infrastructure investment is what could potentially get the commodities market going, and as a result, lead to a recovery in shipping demand.

·Dry bulk focus shifts back to fundamentals – Following a period of high uncertainty and significant disruptions across the commodity spectrum, the gradual normalization of trade is shifting the market’s attention back to the traditional demand and supply dynamics that have shaped dry bulk profitability for decades. As effective fleet supply growth for the next few years looks marginal, demand will be the main determinant of spot freight rates with China returning back to the driver’s seat as the dominant force of bulk imports and thus shipping demand.