SVB is not a Lehman moment, and probably won’t become one.

Summary

The US experienced the second biggest bank failure in its history on Friday when $209bn worth Silicon Valley Bank failed and was taken over by the regulator. However, despite the eerie echoes of 2008, we don’t believe we are in a Lehman moment.

For the time being SVB doesn’t appear to have been involved in any sort of fraud. After registering some “unrealised losses” and raising capital, Silicon Valley CFOs got scared and many lined up to get their deposits out. The bank simply faced an old-fashioned bank run.

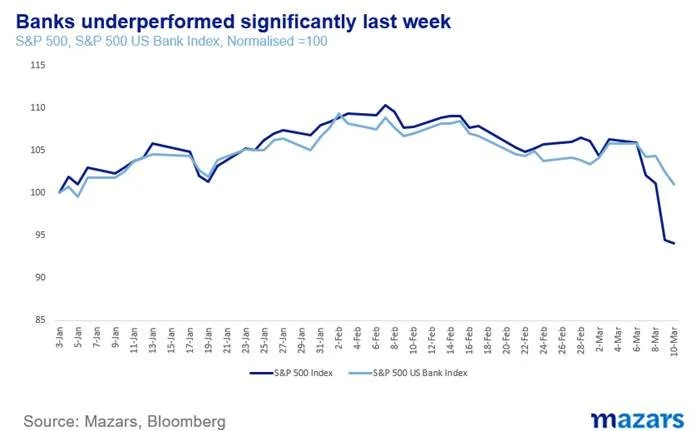

The FDIC stepped in late on Friday, and now the bank is under administration. The US Banking index had two of its worst days in years.

However, we are not in 2008, at least not yet. This bankruptcy echoes across the world, to be sure, and we should expect some volatility in the coming week. But

Unlike 2008, banks are much better regulated and much better capitalised.

We are not facing a systemic credit crunch.

Lehman was a global behemoth. Few people knew of SVB until Friday.

Unlike 2008, the Fed has tools to fight the danger immediately. First, it teamed up with the Treasury and the FDIC to announce that all depositors, whether insured or not, would be made whole. It also announced a new lending facility to cover entities who have lost money on last year’s bond rout, in addition to the many existing lending facilities.

Of course, there are still risks. These, much like 2008, are on the side of policymakers. A policy mistake could happen if Fed officials spend the week advocating a double rate hike on the 22nd of March. Markets, who had been pricing in a double rate hike, are now pricing in less than one hike. Congress could also react. More often than not, Washington is not in tune with Wall Street.

But this is not a Lehman moment. If one is desperately looking for an analogy, it’s probably a Bear Sterns moment. If handled properly, risks should not pile up.

One of the things that puzzled us in the past few weeks, was that despite the sharp rate hikes, the Fed hadn’t broken anything. In the final stretch before an anticipated pause in rate hikes, however, something finally broke.

The US experienced the second biggest bank failure in its history on Friday, when $209bn worth Silicon Valley Bank failed and was taken over by the regulator. Equities fell sharply, especially bank stocks, as investors run towards bonds for safety. In times like these it’s not difficult to attract a following shouting “Lehman”. After all, SVB’s Chief Administrative Officer was Lehman’s CFO (you can’t make this up…).

However, despite the eerie echoes of 2008, we don’t believe we are in a Lehman moment. To understand why we first need to take a step back. SVB was a bank mostly for tech startups in Silicon Valley. The way this works is that when a start-up receives venture capital money, they need to deposit it somewhere as they build up their capabilities. 50% of those companies deposited that money with SVB. When banks receive cash (a liability for them as they need to pay it back), they have to do something with it. From 2019-2021, the deposits tripled. SVB needed to take those funds and acquire assets to pay its costs. It held $212 Bn of assets against $200Bn of liabilities (deposits and short-term funding obligations). SVB chose to invest mostly in long-term US Mortgage Backed Securities and US Treasuries, with some leverage typical for the sector. This is important to understand. For the time being SVB doesn’t appear to have been involved in any sort of fraud.

But last year proved to be apocalyptic for the bond market, which registered its biggest drop in 40 years. Steep rate hikes meant huge losses, especially for longer-dated bonds (shorter-dated tend to have less volatility).

This meant a lot of “mark-to-market” losses for banks holding those bonds. But under post-2008 rules, if one holds a bond to maturity they don’t have to write the asset down. These count as “unrealised losses”.

On Wednesday 8th March, SVB announced it was selling $21 Bn of liquid assets (mostly Treasuries), at a 9% loss to raise money to cover their losses.

The CFOs of startups got wind that the bank was facing issues and knew that they were not fully covered by the Federal Deposit Insurance Corporation (FDIC). SVB has the money Venture Capitals give tech startups. This is a lot of money, usually much more than the $250,000 covered by the FDIC. Some first estimates suggest that 85% of the money is not covered by Federal Insurance.

So they started withdrawing their money. As more and more did that, the bank faced an old-fashioned bank run. On Thursday 9th March, depositors attempted to withdraw $42bn from the bank, managing only $16bn and leaving the bank with $1bn of cash negative position. Because the bank, like all banks, is levered, it can’t return all the money to all depositors who ask for it at the same time. It thus failed. Partly because of the steep drop in bond prices, and partly because of the psychology of their customers, who are not your average depositor.

The FDIC stepped in late on Friday, and now the bank is under administration. The US Banking index had two of its worst days in years.

But this is not a Lehman moment. If one is desperately looking for an analogy, it’s probably a Bear Sterns moment. If handled properly, risks should not pile up.

So this week, we will mostly be monitoring for two things: a) evidence of contagion and b) reactions of US policymakers. Ideally, this is not the week for the Fed’s hawks to insist that further rate hikes are needed to crush inflation (a likely outcome). Instead, they should spend the week silently pondering the futility of trying to reduce the central bank’s balance sheet. It takes years to reduce the Fed’s assets, and days for a crisis to erupt and blow it up again. Nor is it the time for lawmakers to cry foul ahead of next year’s presidential election (a less likely outcome as some probably will). A political debate in one of the most partisan Congresses of all time could make bank rescues harder.