The Big Picture: Panamax market

Slow start to the year

Since the turn of the year, in tandem with the other dry bulk markets, Panamax rates have shed 31% in value. We look at several factors that have caused this move lower.

By Mark Nugent

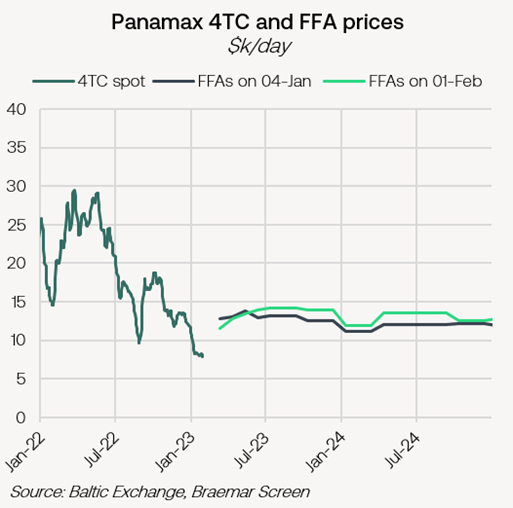

The Baltic Panamax index time-charter equivalent declined by $368/day today, printing at $8,894/day at the time of writing, as dry bulk markets move past the holiday period in the Far East. The Panamax fleet lifted 98.2m tonnes of bulk commodities in January, increasing by 14.5% YoY, while declining by 3.6% MoM. Much of the increase compared to last year can be attributed to the Indonesian coal export restrictions in place at the time.

Compared to the first print of the new year, Panamax FFA prices have moved higher across much of the curve, owed to growing optimism on China’s demand prospects later in the year. The Panamaxes have traded at a premium to the larger Capesizes for much of the year so far, though FFAs are currently pricing in a sharp reversal in this trend for the second half of the year. The Cape v Panamax Q2 contract spread lies at -$250 at the time of writing, whereas the Q3 print shows $4,725, according to Braemar Screen.

Pacific coal

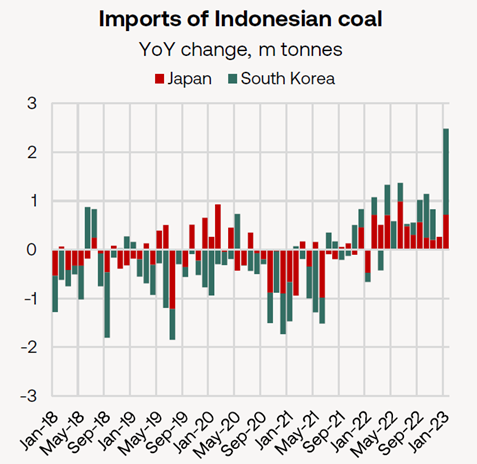

January proved to be a solid month for Indonesian coal shipments which totalled 40.1m tonnes in January, 6.4% above 2021 levels. The Panamaxes lifted 57% of these volumes, at 22.9m tonnes. Liftings destined for China totalled just 9m tonnes in January on the Panamaxes, declining by 24% compared to volumes in January 2021 following a record month for domestic production in the country in December at over 400m tonnes.

As Chinese volumes remain light, Indonesian miners have found buyers elsewhere in the Far East. Indonesian coal exports on Panamaxes bound for Japan totalled 2m tonnes, increasing by 59.4% YoY. To South Korea, Panamaxes loaded 2.9m tonnes of coal in Indonesia, more than double the volume across the same period last year, and the highest monthly total since January 2019. Much of the substitution can be attributed to the sharp rise in Newcastle coal prices following the outbreak of the Russia-Ukraine war, with both countries’ imports from Indonesia largely in growth territory ever since. Also to consider is the greater reliability of Indonesian coal, given the disruptions in Australian shipments in the past 12 months. Most recently this week, a derailment has hindered deliveries to the port of Gladstone.

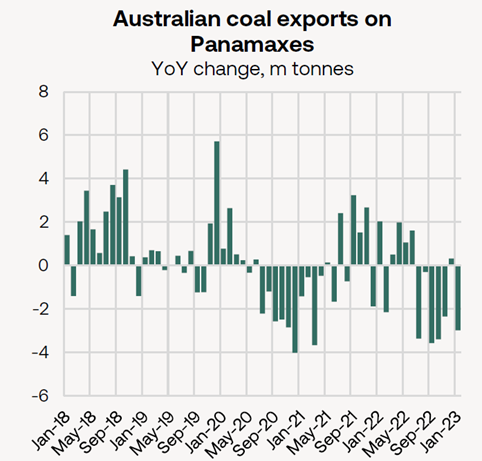

It has recently been reported Japanese utilities are aiming to lower coal import costs by purchasing greater quantities of lower-grade coal. While this is beneficial to the Indonesian miners, it does create a net-negative scenario in terms of Panamax demand, given the much shorter distances travelled compared to a stem from Australia to the Far East. On the Panamaxes, Japanese and South Korean imports of Australian coal declined by 11.4% and 31.2% to 6.7m and 1.2m tonnes respectively.

The Panamaxes have also seen limited benefit from the surge in European demand for Australian coal, as this is done primarily on the larger Capesizes. As a result, total Australian dry bulk exports on Panamaxes have been softer to start the year, amounting to 21.2m tonnes, declining by 11.8% YoY, mostly due to the weakness in coal, while grains have proven relatively steady. Despite the unofficial ban lifted in China, very few cargoes have hit the market so far.

Overall, the lack of activity in the Pacific, has driven a steady migration of tonnage across to the Atlantic basin, which is now facing oversupply pressures of its own.

Slow start in the Atlantic

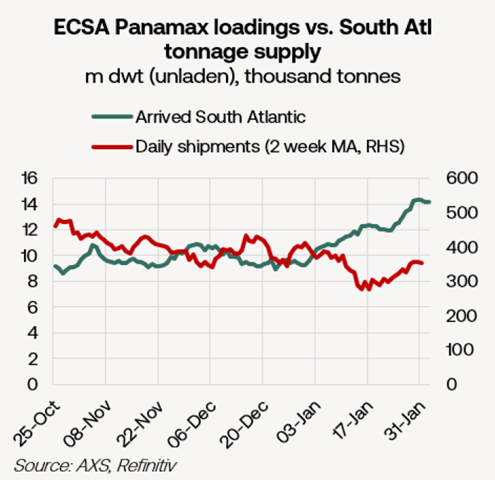

Printing $6,625/day at the time of writing, the Baltic-assessed P1A_82 route is now at its lowest point since June 2020. Fresh cargoes in the Atlantic have been few and far between, with new reports of delays to the Brazilian soybean export season surfacing in the past several days. Following on from last week’s Big Picture, new reports show grain trucks getting stuck on the roads heading to ports due to heavy rainfall. Though this is likely to delay export demand in the short-term, we continue to anticipate a strong soybean season out of Brazil once these issues are resolved. From ECSA, including non-grain cargoes, 14-day average daily Panamax liftings now amount to just 355k tonnes, a decline of 10.5% since the start of the year.

With activity muted in the Pacific for the most part in 2023, the amount of vessel arrivals into the Atlantic basin in recent weeks consistently risen. At the start of the year, 9.5m dwt in unladen Panamax tonnage was positioned in the South Atlantic. This has since climbed to 14.2m dwt at the time of writing, an increase of 48.8%. This has come amidst an already soft period for demand, as Brazil has ben unable to ramp up soybean shipments. In South Africa, Panamax demand has been steady, with these vessels loading 2.5m tonnes of dry bulk commodities (mostly coal) in January, a 12.6% increase MoM, albeit not enough to soak up the supply moving back West.