The headline numbers are telling the story of a strong risk asset rebound and economic soft landing or no-landing on the back of a stoppage in rate hikes. Looking under the hood suggests that the current central narrative, while still very much possible, is on the upper end of potential outcomes.

Rates can still go up, quantitative easing probably makes equity rallies unsustainable and governments are borrowing heavily to sustain growth.

This market is uncertain, and as such, it is very investible. Investors just have to be prepared for the boat to rock often.

I love a good story. I really do. I’m one of those people who love movies not for the effects or the acting but for the quality of the story. Shawshank Redemption, check. Godfather Part II, check. Network (1976), check (if you want to understand today’s economy, one of the best movies ever). Pulp Fiction, Check. Goodfellas, check. Avengers… well, not really. I love good stories so much, that I prefer them to reality, at least for a little. My better half prefers to pause every 20’, to feed the little one, and discuss, and problem-solve, and… ugh.. communicate. The love of my life to be sure, but literally the movie companion F-r-o-m H-e-l-l.

It seems that many people love stories. That’s why we (incredibly) still have bookshops, and the most content ever created. Since 2013 when Netflix’s first in-house series, House of Cards, came out, film and TV content spending has doubled, to nearly $243 billion per annum. And despite that, the book publishing industry is holding its own with a market size of $30bn per annum, nearly as much as a decade ago.

Stories are good for learning too. Yesterday, the little one woke up at 03.00 in the AM because she wanted to hear more about Odysseus and the Cyclops.

Stories are how we learn, and how we entertain ourselves.

But stories aren’t, and should never be, how we invest. Investment and economics are really a boring way to see the world. We invest money based on profitability indicators, on products, on valuations and convoluted interest rate assumptions and derivatives positioning and… you get the picture. It’s very difficult to say a good story about all that. I used to want our financial planners to attend our Monday investment meeting. After some time I figured there was no need for this sort of maltreatment of other human beings. David Baker, my boss, often revels in reminding me that the things that excite me, don’t necessarily excite others.

If one looks at any successful film about finance, it’s all stories about how people broke the system. Wall Street (1987), Rogue Trader (1999), Margin Call (2011), Wolf of Wall Street (2013), Dumb Money (2023), were all stories about quirky people. Not one was a story about how to invest. The only movie that ever made money evangelising investment fundamentals was The Big Short (2015). Still a movie of quirky people by the way.

Which, finally, 370 words into the weekly, brings us to the subject of the day: stories versus reality.

After a bad September and October, we are seeing the first signs of an equity rally. The story is sound.

· Fed and possibly ECB and BoE rates have peaked.

· Inflation is coming down, however slowly

· Recession, if it comes, will be a shallow one

· Cost of money will still come down, as inflation wanes.

· Lower inflation and cost of money should be good for both equities and bonds.

Yes, we can’t have a sustainable bull market while there’s Quantitative Tightening, to be sure, but that should now be just around the corner.

All that is valid, and we have argued as such. But, we have also warned against reading too much into the sustainability of a Santa rally. Let’s look under the numbers for a while. Since the beginning of November, US equities have rallied 5.3%. But this rally is mostly down to the dominance of a few tech companies. The S&P 500 Top Ten actually rallied 8.5%. An equally weighted S&P 500 has only gained 3.6%. And bonds, which should be favoured if investors really feel that rate cuts are coming, have only gained 1.7%.

Interesting fun fact. The heavy outperformance of a few stocks against the rest of the market has been closely linked to financial stress.

Central bankers Jay Powell and Christine Lagarde last week, reminded us that it is not written in stone that their next moves will be rate cuts. This caused some stress amongst traders by the end of the week.

From an economic perspective, things aren’t that great either. On the face of it, the global economy is doing much better than anticipated. About half of economists now predict a recession, versus roughly one year ago.

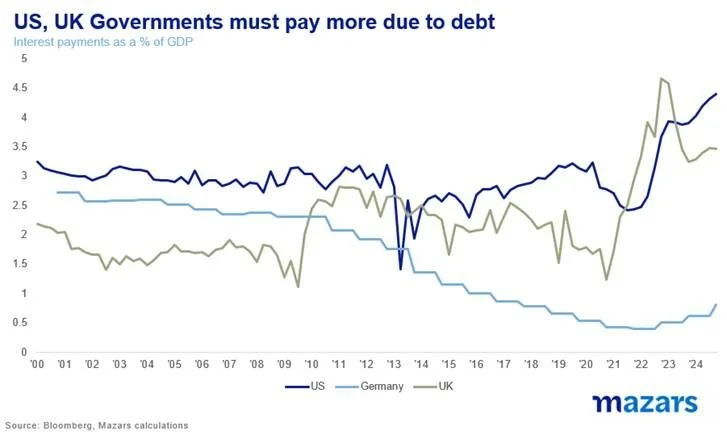

But to achieve this, governments ramped up borrowing. Especially the US government, which is now running a 6.7% deficit and will be making interest payments of 4.4% by the end of 2024, nearly double its projected real GDP.

It’s no wonder that Moody’s followed Fitch last week, downgrading US debt.

And there’s the geopolitical risk premium to think about. Getting an above-zero return in a world of zero-rates and relative geopolitical stability wasn’t a big ask. But now, investors should ask for more. It’s not bad enough that we have two ongoing conflicts with potentially global implications. Last week, the largest bank in China, ICBC, was hacked at exactly the time that it would participate in an auction of the US 30y bond. Failure to show up led to higher yields across the board. Wars are not just bombs. They are hybrid.

If you are looking at UK GDP, then look beyond the 0.2% rise headline. September’s uptick was mostly due to a rise in demand for professional services and healthcare. Consumption, the sustainable driver of GDP, was subdued.

Source: ONS.

There are plenty of reasons to be worried. As investment managers, this is, in fact, what we are paid for. We are paid to question the story, the narrative of the eternal bull market. It’s not the time to sink into the news stories. It is the time for hard metrics and difficult questions. If our scruples are justified, we protect investors. If they are not strong enough, we should up the risk. Make no mistake. Uncertainty is not bad. In fact, it is the best friend to informed and sage investors. The more uncertainty, the more opinions differ the more positioning will differ, and the better the payoff if things work out. An investor who has done their homework, who has a philosophy, who has applied thinking and experience should be ahead of the pack in this market. An investor who asks, “is my portfolio making enough to compensate you for the risk?”, “is it diversified and hedged enough” is asking the right questions.

This market is uncertain, and as such, it is very investible. Investors just have to be prepared for the boat to rock often.