Seasonality is historically favourable during the first half of the fourth quarter but its dynamic usually fades towards the end of the year.

Capesizes made headlines for yet another time. However, this week, it was not because of the meteoric rise of Baltic Capesize indices but rather their steep fall. Justifying once again its reputation of being highly volatile, the leading Capesize index has managed to increase its value from $21,645 to $31,089 daily and then fall back to $18,461 daily in less than one trading month. Losing some 37.4 percent of its daily average within the last five trading days, the capricious Capesize segment hard-landed this Friday at $18,461 daily. In sync, iron ore futures trading was rather dull in early trade on Friday as investors weighed China's stepped-up fiscal support against near-term demand prospects. In fact, concerns about Chinese steel mills' further reducing production to comply with emission control protocols and to minimise losses amid weak sales, capped weekly gains for iron ore spurred by Beijing's additional fiscal stimulus. Trending mostly sideways, Panamax segment concluded this week at $14,448 daily. With mineral Transatlantic rates correcting downward and ECSA FHs losing some steam, the respective Baltic indices were mainly the only ones in the red. After touching multi-month highs last week, both Supramaxes and Handies took a breather during the forty-third trading week, laying today at $13,024 and $12,080 daily respectively.

October has been a fruitful trading month for the Capesizes, with the TCA surpassing the $30,000 mark for the first time over the last seventeen months. In tandem, freight rates for iron ore from both Brazil and Australia to China have increased materially during the same period, with the former pushing to over $26 per tonne and the latter advancing towards $11 per tonne. Fanning the flames of an already robust sentiment, iron ore stocks at the major Chinese ports touched multi-year minima in mid October. In fact, portside inventories slid to 105.2 million tonnes as of October 13, down nearly 20 percent year-on-year, and the lowest level since October 2016, data from consultancy Steelhome showed. However, the last couple of weeks, supported by increased China-bound iron ore cargoes, piles of rich in iron oxides ore grew in size. In fact, inventories of imported iron ore at China's 45 major ports included in Mysteel's weekly survey have grown for the second week in a row to 111.4 million tonnes by October 26, up by another 956,500 tonnes or 0.9 percent from last Thursday.

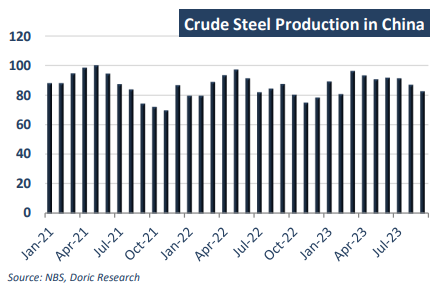

Whilst iron ore port stocks seem to have reversed the previous period downward trend during the last two weeks, China's crude steel output fell 5 percent in September from August, according to official data. The world's largest steel producer churned out 82.11 million metric tonnes of the ferrous metal last month, extending falls for the third consecutive month from 86.41 million tonnes in August, and 90.8 million tonnes in July, data from the National Bureau of Statistics (NBS) showed. In the first three quarters, China's crude steel production reached 795 million metric tonnes, up 1.7 percent year-on-year. On the other hand, crude steel consumption amounted to 731 million tonnes, down 1.5 percent year-on-year." The contraction in steel consumption owes much to the slowdown in new-home construction," according to the vice chairman of China’s Iron and Steel Association, Jiang Wei. He further stressed that "the structure of China's steel industry improved during the last three quarters, as the demand for high-end steel continued to increase in sectors such as shipbuilding, auto manufacturing, home appliance, and photovoltaic power. The exports of high-value-added steel products also gained a greater share in the country's total exports." Looking forward, Jiang said that "steel demand will very likely pick up, thanks to brisker manufacturing activities, the rapid growth of new energy industries and the supporting role of infrastructure."

In spite of the positive tone in China’s Iron and Steel Association comments, the northern Chinese city of Tangshan, China's top steel production hub, will launch a level-2 emergency response from Friday amid a forecast of heavy air pollution raising concerns for the short-term outlook. As for dry bulk shipping, seasonality is historically favourable during the first half of the fourth quarter but its dynamic usually fades towards the end of the year.

Data source: Doric