By Daniel Hynes

A weaker USD helped boost investor appetite in commodity markets. Rising geopolitical risks were also front of mind following damage to energy infrastructure earlier this week.

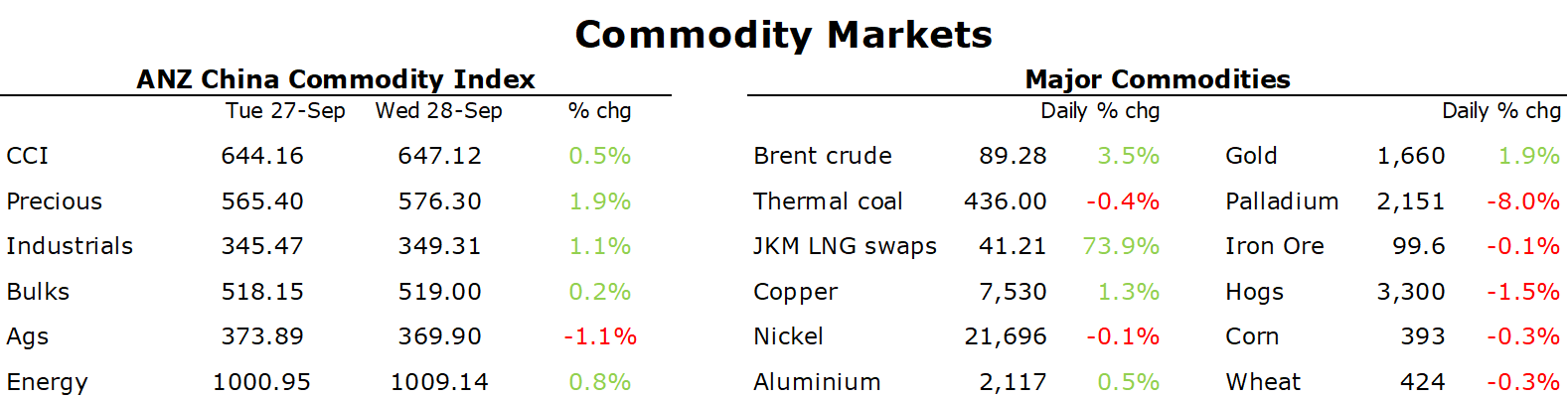

European natural gas extended gains after Russia warned of further risks to supply. The energy market was rattled after damage to the Nord Stream pipelines. European Union foreign policy chief Josep Borrell said the damage was deliberate, and that the bloc will take more steps to secure its major energy facilities. Dutch front month futures rallied 11.3% to break back above USD200/MWh. Adding to concerns were warnings from Gazprom that gas flows were at risk because of a legal spat with NJSC Naftogaz Ukrainy over transit payments. Any disruptions to supply via Ukraine would leave Europe totally reliant on the TurkStream pipeline via Turkey. For the moment, gas flows remain stable, albeit at a reduced level since the start of the Ukraine war. The threat of disruptions to pipeline gas puts more reliance on LNG imports. However, US gas facilities in the Gulf of Mexico have been impacted by Hurricane Ian. The suspected sabotage of Nord Stream pipelines also raised concerns across the LNG market, with North Asian LNG prices rallying sharply. Futures have gained more than 20% since Monday as expectation of increased competition from European consumers rises.

Rising geopolitical risks saw crude oil prices rally. The European Union announced a new round of sanctions against Russia including a ban on European companies from shipping Russian oil to third countries above an internationally set price cap. However, this will require a change in legislation, leaving a risk that it won’t be in place before the current deadline of 5 December. A sharp fall in inventories also helped push prices higher. US inventories of crude oil fell for the first time in a month. EIA data showed stockpiles fell 215kbbl last week, while West Coast gasoline stockpiles fell to their lowest level in 10 years. Disruption to supplies due to Hurricane Ian are also causing some concerns, with US president Joe Biden warning oil companies not to hike prices for the second time this week.

The weaker USD helped reignite interest in the metals sector. Copper led the base metals sector higher after intervention by the Bank of England saw the dollar and Treasury yields fall. It wasn’t all plain sailing, with some metals struggling to hold gains amid concerns of weaker economic activity. Tighter monetary policy across the globe remains a persistent headwind for demand of industrial metals. This was highlighted earlier this week after Norks Hydro said it will cut annual aluminium production capacity by as much as 143,300t at two of its plans in Norway in response to reduced demand in Europe.

The weaker USD was a strong tailwind for the precious metals sector, with gold gaining nearly 2%. The fall in Treasury yields triggered some short covering and bargain hunting in the gold market. Platinum and palladium rallied amid heightened supply risks. The world’s biggest platinum miners, including Sibanye Stillwater, Impala and Anglo American are reducing their output amid South Africa’s deteriorating power supplies.

Iron ore futures fell as doubts over a rebound in Chinese demand persist. While the market is entering peak construction period in China, project developers remain laden with debt and steel mill margins have been languishing near the year’s lows since August. The market is cautious ahead of the People’s Party Congress, which starts 16 October. Any signs that it will maintain strict virus controls could see the outlook for construction activity remain subdued for the foreseeable future.

Data source: Commodities Wrap