By Ulf Bergman

The continued lockdowns and other Covid-related restrictions in China have put renewed focus on the long-term outlook for the world's second-largest economy. While the growth rate for the first quarter of the year surprised on the upside, the better-than-expected data highlighted some potential concerns for the coming months.

Much of the strong economic performance was centred on the first two months of the quarter, which benefited from considerable base-effects in comparison with last year. March on the other hand showed significant weakness as the latest outbreak of the coronavirus extended across several Chinese regions, which suggest that the data for the current quarter may fall well short of the numbers for the beginning of the year once they are released in a few months. Additionally, the first quarter saw significant investments in fixed assets, which provided some artificial strength to the growth data. However, theeffects of the latter may prove fleeting in the face of Chinese consumer spending losing even more steam.

Expectations grew in recent weeks that the Chinese central bank would cut its interest rates to support the flagging growth rates. However, they remained unchanged following the bank’s latest policy meeting, suggesting that the policymakers are seeing increasing threats from rising inflation rates amid high commodity prices. The governor of The People’s Bank of China also stressed the importance of maintaining price stability in two separate speeches last Friday, effectively closing the door for any rate cuts in the near term. Instead, the central bank is relying on structural policies to support weaker sectors and cuts in banks' required reserve ratios. The Chinese central bank is also facing additional complications courtesy of the US Federal Reserve, which restricts its room for manoeuvre. Interest rate cuts at the same time as the Fed is embarking on a cycle of aggressive rate hikes could trigger substantial capital outflows and put the Chinese currency under pressure. Such a development would make dollar-denominated commodities more expensive for Chinese buyers in local currency terms and contribute to additional inflationary pressure.

Even before the latest deterioration of the Covid-situation, which has seen the Chinese capital joining Shanghai and other cities in facing lockdowns and other restrictions, projections for the country’s annual growth have been adjusted downwards by many economists. The International Monetary Fund is in its latest estimate expecting the world’s second largest economy to grow by 4.4 per cent this year, while consensus among economists surveyed by Bloomberg points towards a 4.9 per cent growth rate. However, these projections do not take into account the latest round of restrictions and may face additional revisions in due course. The official Chinese growth target still remains at around 5.5 per cent, a far cry from recent year’s strong numbers.

Since China joined the World Trade Organization twenty years ago, the country has become the dominant buyer of most seaborne commodities. Hence, any weakening of demand due to a plateauing Chinese economy could have repercussions for seaborne volumes and commodity prices. In addition, as part of the country’s dual-circulation policy, Beijing is seeking to reduce its dependence on the global supply chains. Last week’s announcement that Chinese coal production will increase by 300 million tonnes this year could potentially put a significant dent in seaborne import volumes. The measure joins previous policy initiatives to safeguard the country’s food independence by increasing the production of grains and oilseeds. While the country cannot reduce its dependency on imported iron ore, China’s state planner, the National Development and Reform Commission, has said that crude steel output will continue to decline this year. This follows last year’s clampdown on steel production in an effort to control rapidly rising iron prices and reduce pollution levels ahead of the Winter Olympics. Since last year, steel exports have also been discouraged through a change in taxation, suggesting that the new reduction in output is targeting export volumes.

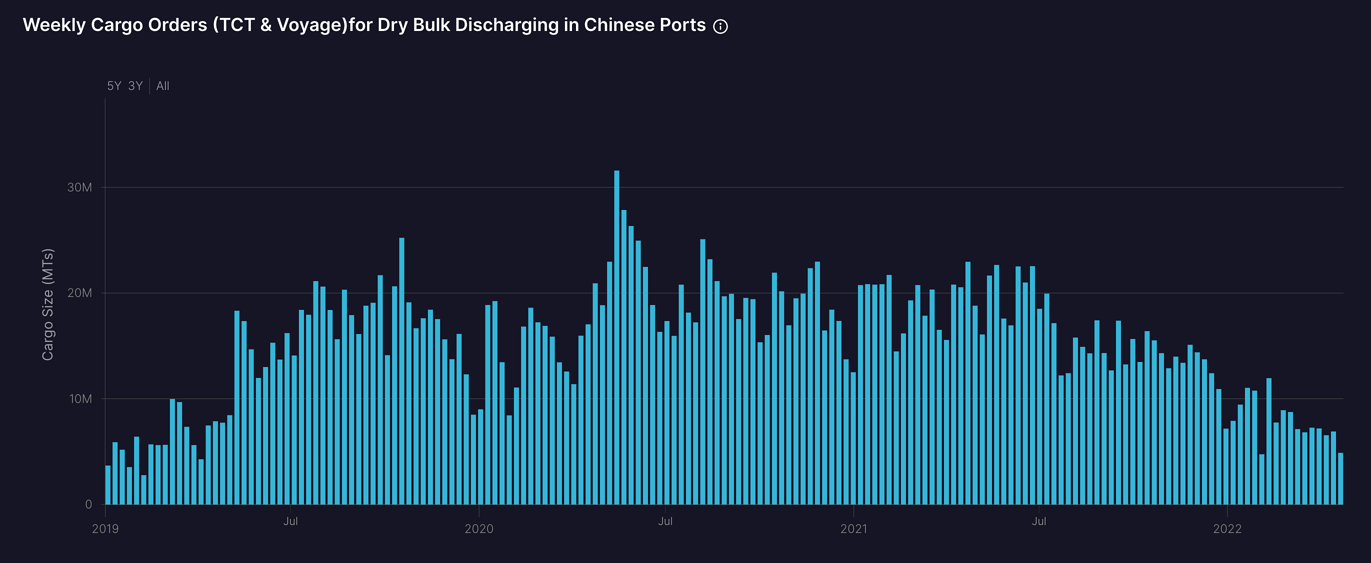

While there has been a reduction in ordering activities and imports in China in recent weeks due to the flare-up in infection rates, it is not the only reason for declining rates. The downward trend started to develop last year as Beijing grew increasingly concerned about pollution levels and increasing commodity prices. Aggregate order data for dry bulk cargoes have seen a steady decline since the middle of last year, with last week’s volumes at par with the runup to the Chinese New Year in early February.

Source: Shipfix

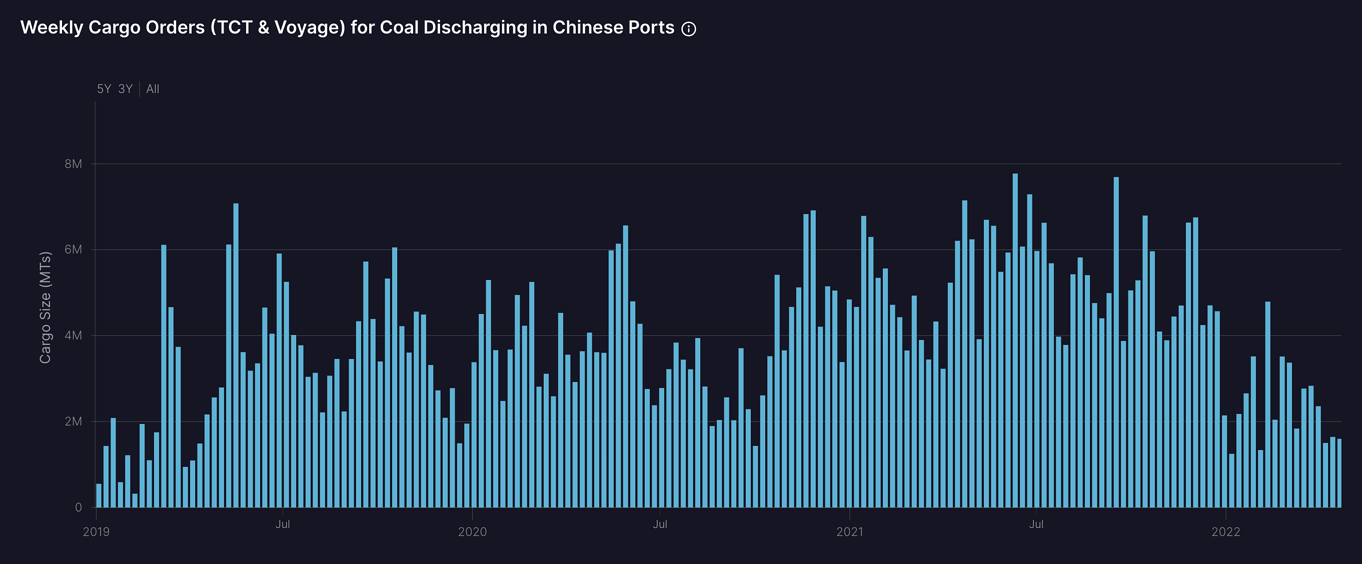

China’s appetite for seaborne coal imports has been in decline as the country ramps up its own mining output. Last month saw a fifteen per cent increase in Chinese production. Price controls on domestic supplies are also putting imported coal at a disadvantage. Hence, cargo orders during the last three weeks are among the lowest recorded in recent years. With Chinese production set to keep increasing during the year, cargo order volumes for coal are likely to remain low for the foreseeable future. However, the development may not be all bad news for dry bulk shipping, as it frees up export capacity for other, more distant customers. While Indonesian coal supplies often are not suitable for European customers, excess supplies from the island nation may find their way to India, re-establishing a previous trade flow. In turn, such a development could see Australian coal increasingly shipped to Europe and Japan to replace banned Russian supplies.

Source: Shipfix

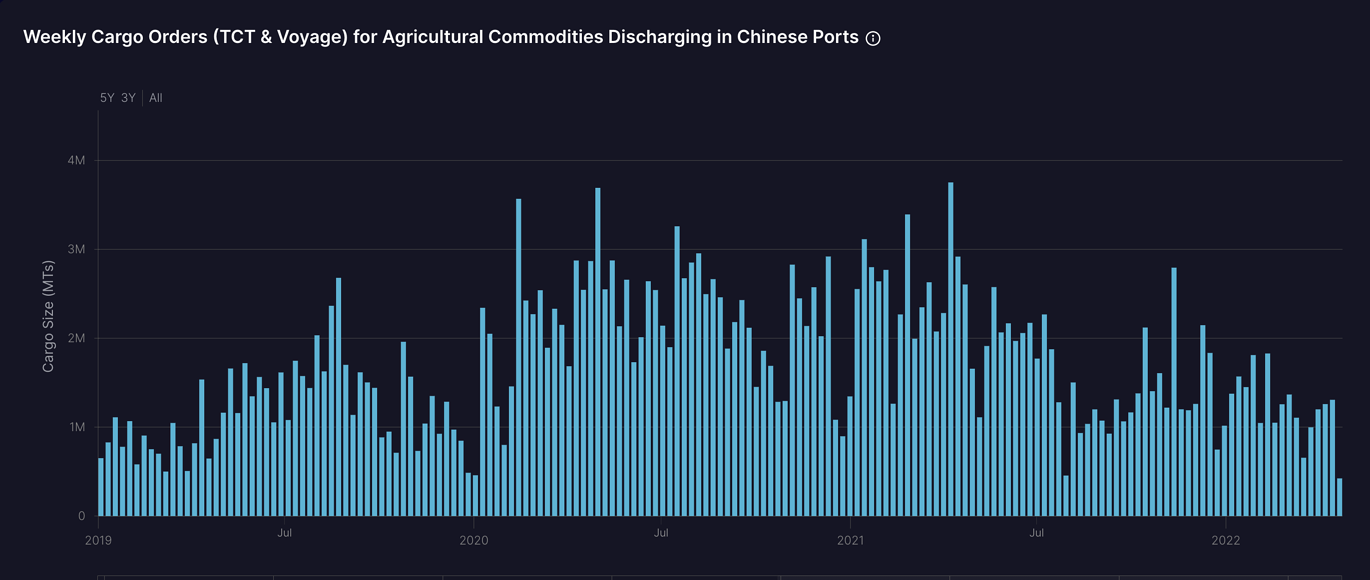

Like for coal, cargo order volumes for agricultural commodities discharging in Chinese ports have pulled back considerably from the dizzy heights observed during 2020 and 2021. In the wake of the African swine flu, the rebuilding of the Chinese pig herd contributed to the country purchasing any available grains and oilseeds, either newly harvested or from inventories. However, with stockpiles depleted and the Chinese economy facing considerable headwinds, the demand for seaborne transportation of agricultural commodities has declined. Recent weeks have seen relatively robust order volumes, but volumes may start to decrease with the Brazilian harvest mostly complete.

Source: Shipfix

The Chinese authorities have committed themselves to support the country’s economy and the flagging growth rates. However, the longer the lockdowns and other restrictions remain in place, the greater the damage to the economic outlook. Hence, imports of commodities may not recover to previous levels anytime soon. However, given the tight supply situation for most raw materials, prices are likely to remain elevated. In addition, dry bulk freight rates should be supported by a thin orderbook and a healthy supply-demand balance.

Data Source: Shipfix