By Ulf Bergman

The European Union formally adopted the fifth package of sanctions against Russian interests on Friday last week. In contrast to previous measures, the bloc will target Russia’s lucrative energy sector, with thermal coal first in line. Under the rules, European companies will no longer be able to enter into new agreements to purchase coal from Russian sources, and any existing contracts will have to be terminated during the second week of August. Hence, European buyers have another four months to find alternative supplies. In addition to coal, an extensive list of commodities and products, ranging from caviar to fertilisers, are facing similar restrictions.

The already complicated race to source alternative thermal coal supplies for European buyers has also become even more challenging as the Japanese government, in a reversal of policy, announced its own intentions to cease importing Russian coal. With the world’s third-largest importer of seaborne coal joining the competition over tight non-Russian supplies, there will be considerable supply concerns going forward, and thermal coal prices are likely to remain high. There have been some suggestions that the current situation will accelerate the switch towards alternative or renewable energy sources. Still, such a development will take time, and in the meantime, coal will, for better or worse, remain an essential source of energy.

The war in Ukraine and the upcoming sanctions on Russian supplies of the fossil fuel are not the only reasons for increasing competition over scarce thermal coal supplies. While coal often is seen as an energy source in terminal decline, it remains an essential part of the energy mix for many countries, notably in Asia. In addition, after some years of declining demand, European utilities were forced to increase their use of the black stuff as a global energy squeeze limited supplies of the preferred natural gas during the second half of last year.

Replacing Russian coal among some of its major importers will require trade flows to change and production to increase elsewhere. However, some of the world’s major producers have suggested that their output is already committed to existing contracts, with minimal capacity to spare. Australia, which for the last eighteen months has faced a Chinese embargo on its coal exports, has successfully replaced its former top customer, with current monthly export volumes broadly in line with what was seen prior to the introduction of the ban. Amid deteriorating diplomatic relations between Beijing and Canberra, the Chinese move led to a change in established trade flows, where imports from Indonesia replaced Australian coal in China. At the same time, India started to source increasing amounts from Australia, while imports from its traditional leading supplier, Indonesia, dwindled.

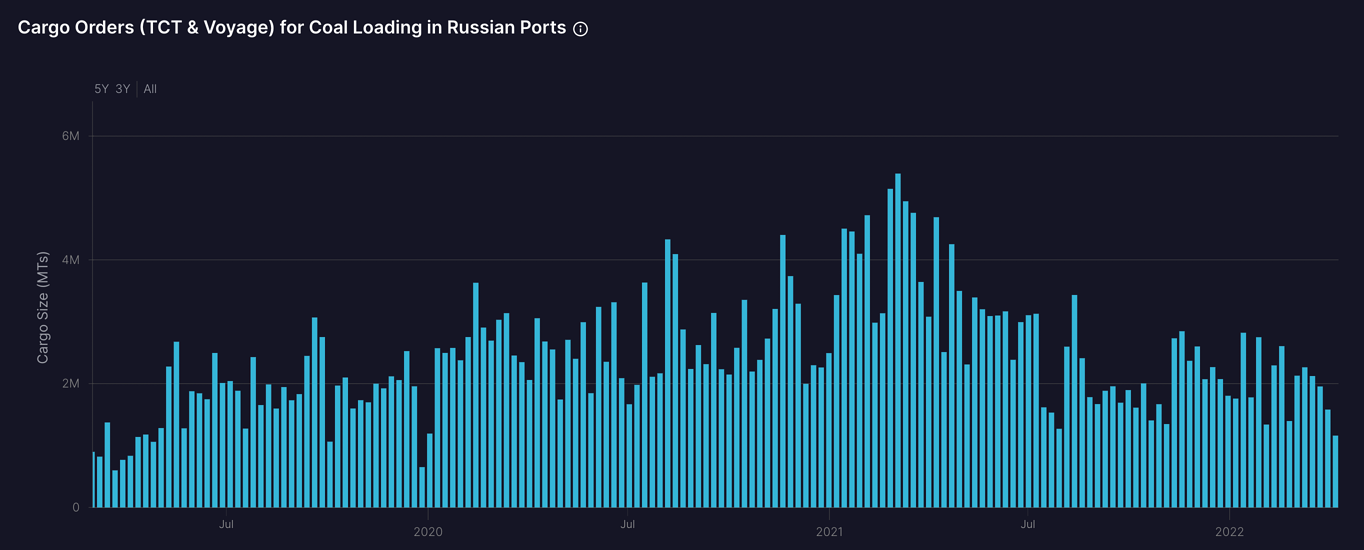

In contrast to the ongoing Chinese ban on Australian coal, the Russian exports of the fossil fuel carry additional political luggage and may struggle to find alternative markets. At this stage, only China and India look to be realistic options, but any imports are likely to incur additional political costs. The US is also leaning diplomatically on India to limit any purchases of discounted commodities from Russia, a traditional ally of the South Asian nation. There have also been reports of Russian thermal coal becoming increasingly hard to sell despite significant discounts. Cargo order data from Shipfix also highlights the diminishing popularity of Russian coal, with volumes trending lower in recent weeks.

Source: Shipfix

Assuming that the European and Japanese bans go into full effect, approximately 75 million tonnes of coal need to be sourced elsewhere annually, according to data from the International Energy Agency. While such volumes account for only a few per cent of the coal shipped across the oceans annually, the lack of investments in new coal mining capacity in recent years meant that global coal miners operated close to full capacity already before any sanctions on Russian supplies were even considered. Hence, no apparent, simple solution is likely to present itself, and the global seaborne trade in coal will face a period of sub-optimal trade flows.

Japanese and European imports of Russian coal have typically benefitted from relative short sea voyages, with exports often shipped from ports in the Baltic Sea and the Far East. Nevertheless, the upcoming import bans will force buyers to look further afield to source their required thermal coal. While Japanese purchasers may shift their focus south, to Indonesia and Australia, with reasonably limited increases in voyage lengths, for Europe, the distances will increase considerably.

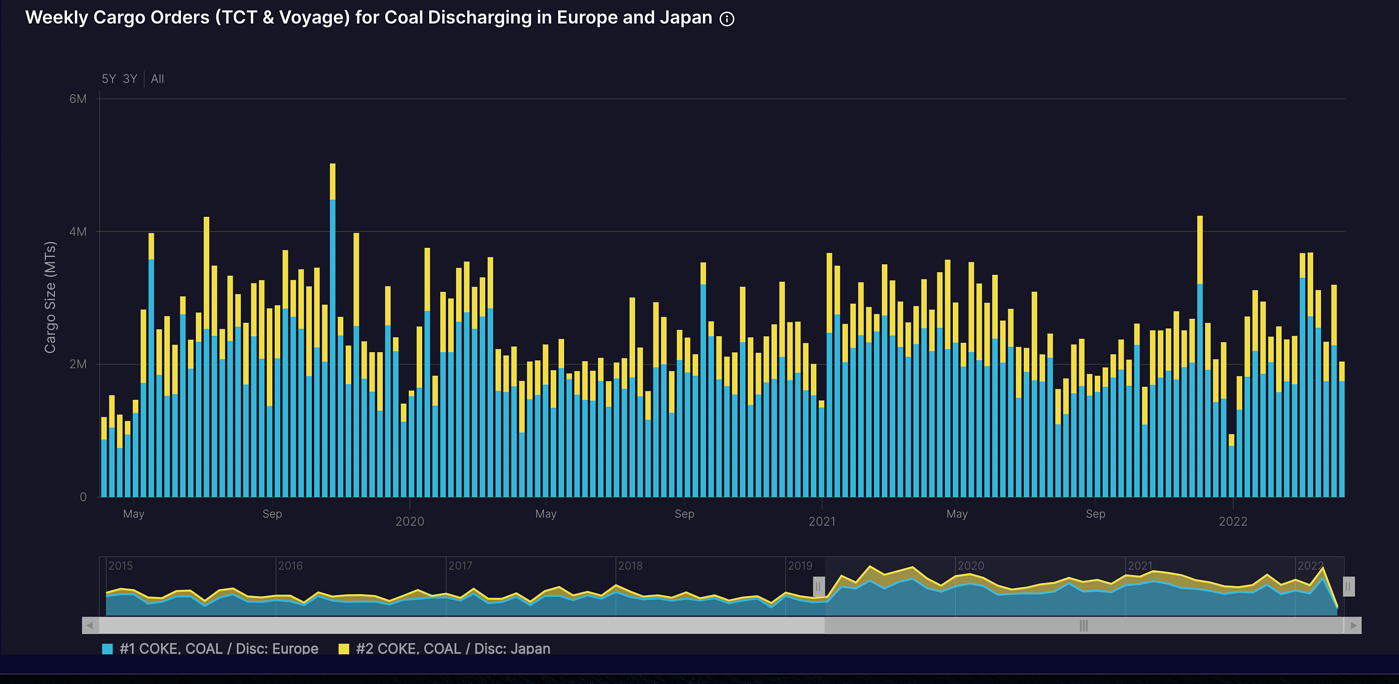

In recent weeks, cargo order data for coal discharging in Europe or Japan have been robust. European volumes have reached the highest ever, possibly in anticipation of sanctions on Russian trade. Likewise, ordering activities for coal to be discharged in Japanese ports have remained firm in recent weeks. However, rising natural gas prices amid limited supplies are also likely to have contributed to the rise in orders, as electricity providers have been forced to increase their thermal coal use.

Source: Shipfix

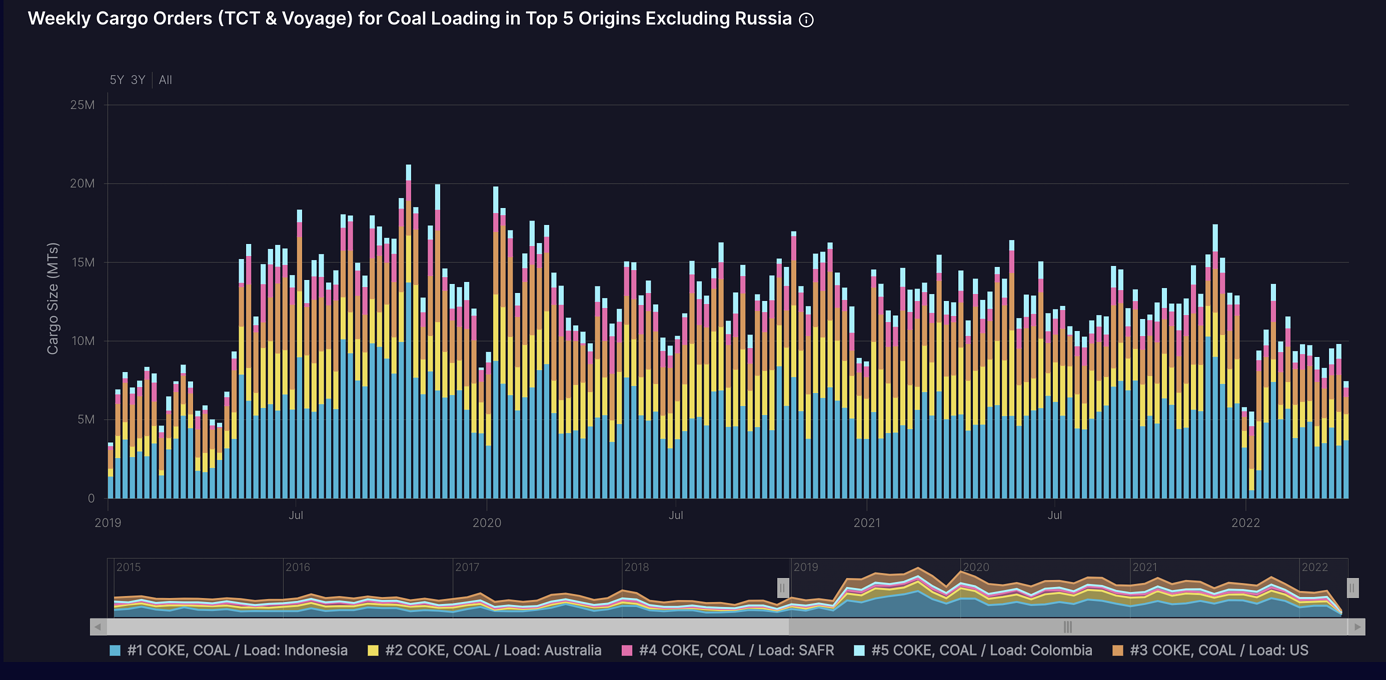

Ordering activities for coal loading in the largest exporting countries have been trending lower in recent months, suggesting that there could be spare capacity for exports to Europe and Japan. However, much of the decline is centred on Indonesia, which is increasingly safeguarding domestic supplies and limiting exports. Should buyers in Japan and Europe be successful in sourcing their coal from the other primary exporters, tonne-mile demand will pick up in the trade.

Source: Shipfix

As previously discussed in Shipfix's weekly blog, India remains the key to how the global seaborne coal trade develops in the coming weeks and months. Should India go ahead and buy discounted Russian coal, despite diplomatic pressures, much of the expected squeeze on global supplies may not materialise, as it could free up export capacity from both Australia and Indonesia. It would also increase the tonne-mile demand in the dry bulk sector. Given India’s current low inventories and rising risks of power cuts due to coal shortages, the proposition of cheap supplies from its longstanding ally may prove too tempting to ignore.

Data Source: Shipfix