By Ulf Bergman

Thermal coal prices have retreated in recent weeks from the dizzy heights they reached in the immediate aftermath of the Russian invasion of Ukraine. Still, and despite losing around of a quarter since early March, at around 325 dollars per tonne prices remain some 250 per cent above what was seen at the same time last year. The dirtiest among fossil fuel also remain about a third higher than just before hostilities commenced.

Prices have been soaring on concerns over global supplies of the commodity, as exports from the Black Sea region has become disrupted and Russian exports from other ports facing sanctions, both formally and informally. However, it is not only the supply side of the equation that contributed to the rising prices. There has been a spill-over effect from price rises and supply problems for other energy commodities, with demand on the rise as power plants have been seeking to substitute other energy sources with thermal coal. While the new deal between the European Union and the US will see increasing flows of seaborne liquified natural gas heading for the former’s terminals, the energy mix is unlikely to see a rapid change. Hence, the previously reported pattern of elevated cargo orders for coal discharging in Europe could remain in place for the foreseeable future.

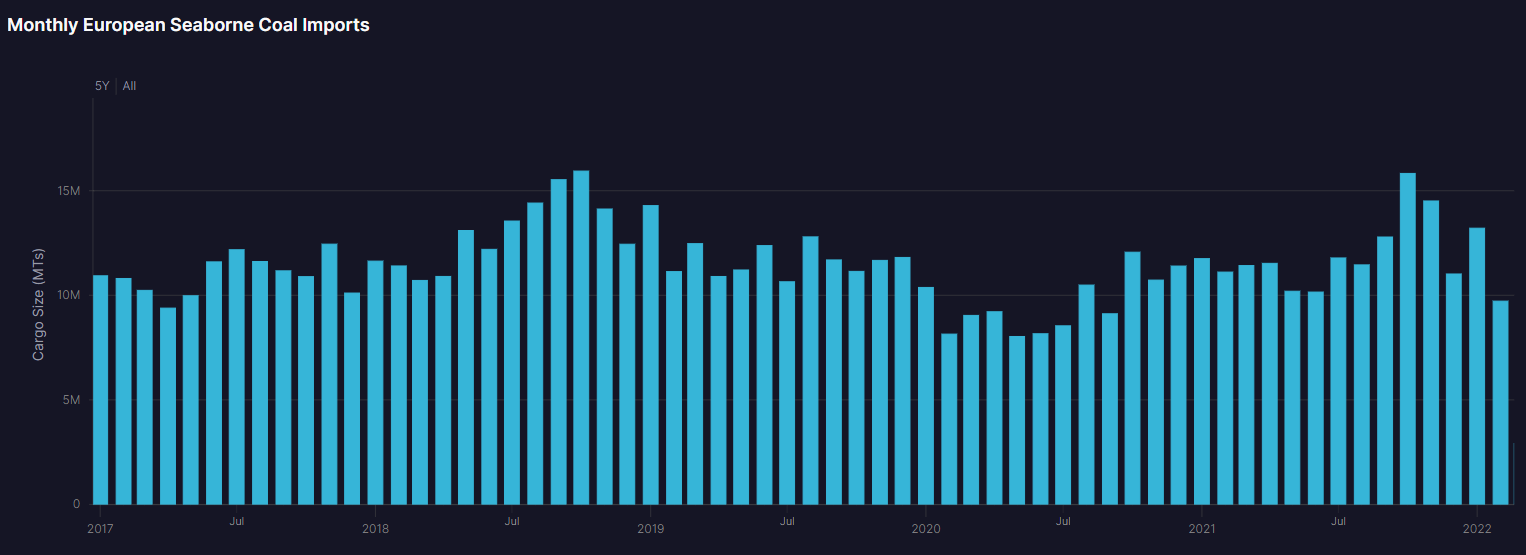

Despite the decarbonization debate topping the global agenda in recent years, seaborne exports volumes of coal have shown no signs of declining. If anything, the numbers have been on the rise since the world started to emerge from the initial effects of the pandemic. An increasingly tight supply situation for natural gas have seen thermal coal becoming more important to many countries’ energy mix yet again. Even in Europe, often seen as the leading force in the global decarbonization efforts, imported volumes of seaborne coal have reached their highest levels since 2018 in recent months. Even before the war in Ukraine, the flow of Russian gas through the pipelines to Europe was unreliable and saw European seaborne imports of coal reaching sixteen million tonnes in October last year, the highest monthly volume for three years. While monthly volumes have receded from the recent high, the early arrival of winter in Europe combined with a legacy of low natural gas inventory levels have kept imports above what has been seen in recent years.

Source: Shipfix

However, it is not only in Europe that the demand for thermal coal is rising. The world's biggest consumer and importer of the commodity, China, has also been driving the global demand higher. While the country is officially committed to reducing its carbon footprint, the current five-year plan implies that its coal consumption will continue to rise until the middle of the decade. It has been widely expected that China's use of the fossil fuel would stabilise and even decrease during the second half of the decade. However, the increasing economic headwinds that the country faces may delay such a development. Many countries, notably in Asia, are also constructing new coal-fired powerplants, suggesting that demand for the commodity will remain robust.

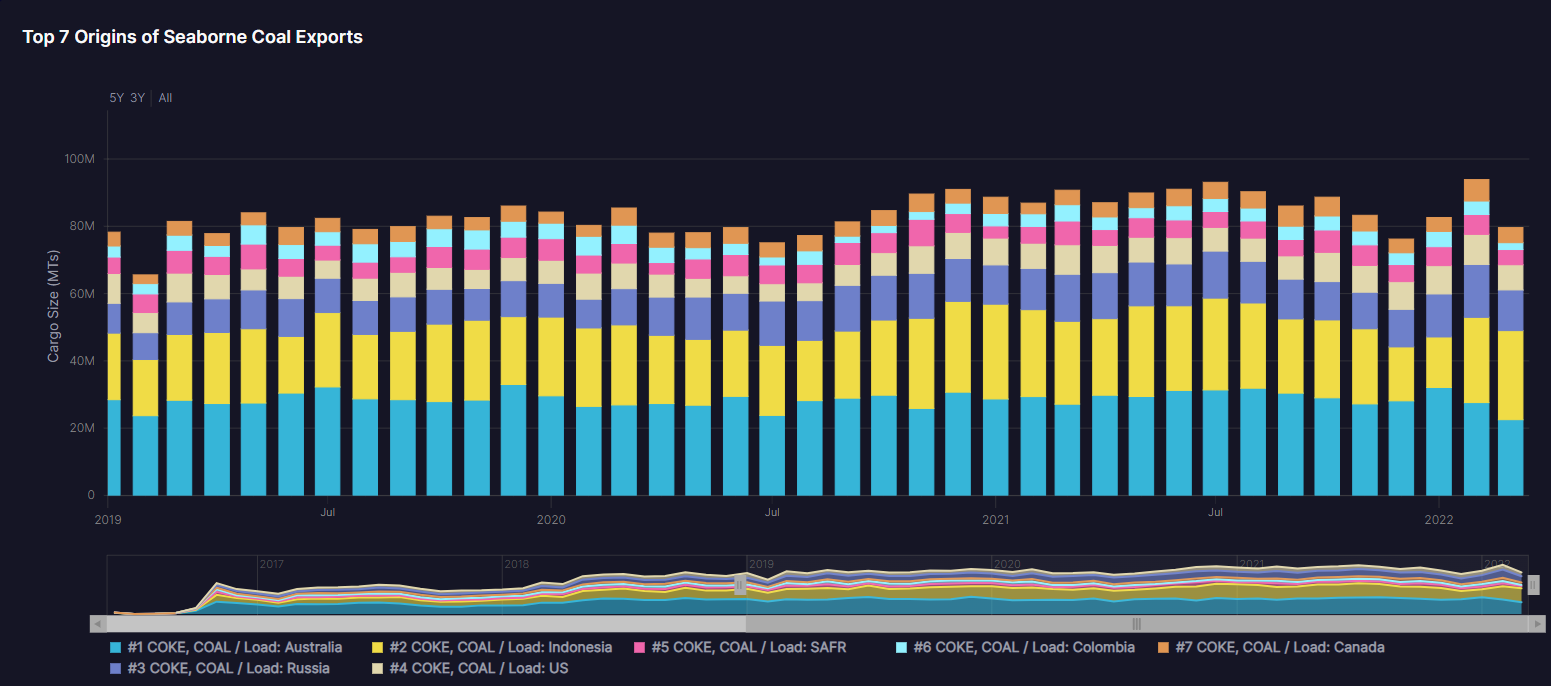

Global seaborne exports of coal are dominated by Australia and Indonesia, which between them accounts for almost two-thirds of total volumes. Another five countries make up most of the remaining third. Apart from a drop in volumes during December and January, mainly due to export restrictions and adverse weather conditions in Indonesia, the average total monthly seaborne volumes have been just below ninety million tonnes during the last year. However, the current month may be heading for levels well above the average. With more than a fifth left of the month, shipped volumes have already reached eighty million tonnes and assuming a degree of linearity for the remainder of March, the total for the month may reach 100 million tonnes. Should the rest of the month evolve along such a path, seaborne exports would be thirteen per cent higher than the same month last year and highlight the increasing importance of the commodity to the global energy mix

Source: Shipfix

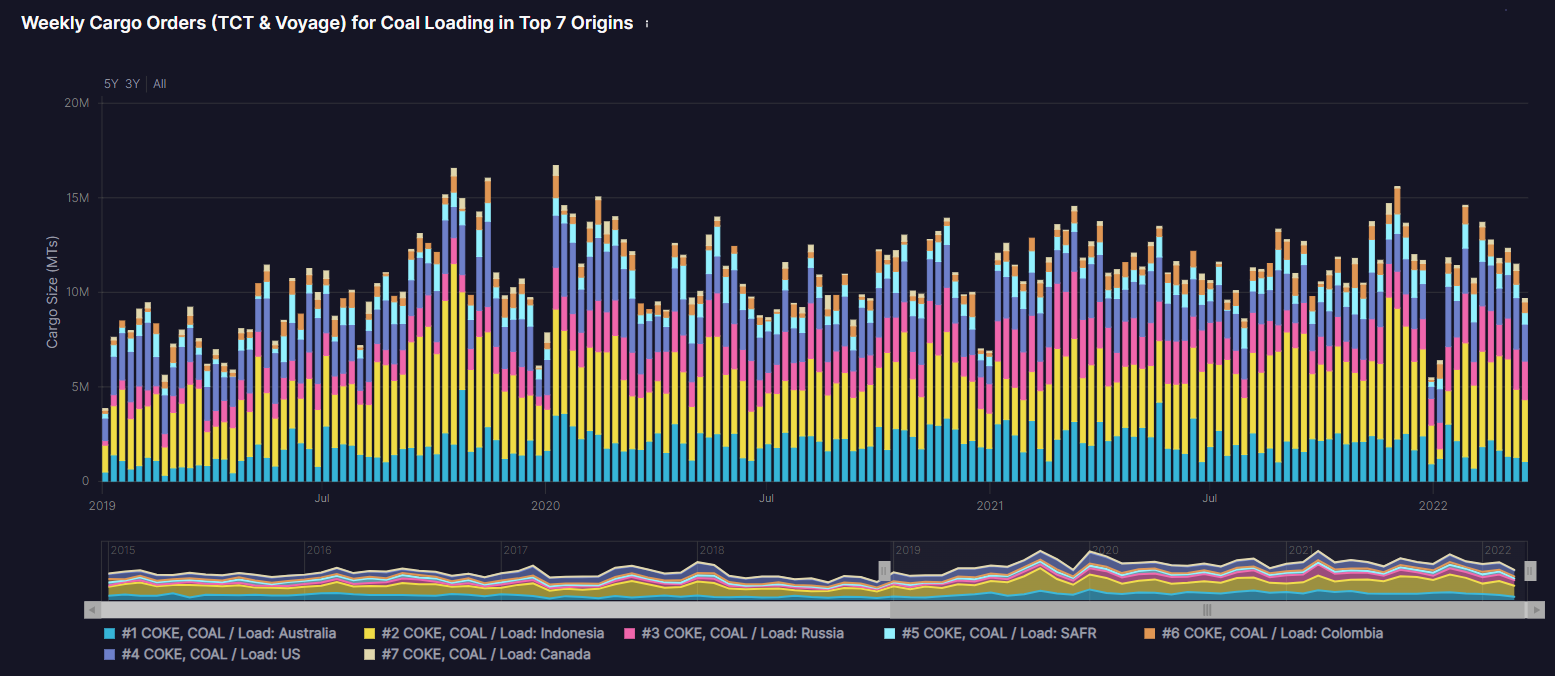

Russian coal exports have held up well on an aggregate level for the month, but the volumes appear to have been decelerating following a solid start to March. Indonesian exports of coal, on the other hand, look set to be on course for one of the best months on record as buyers try to find alternatives to Russian supplies. Likewise, Australian coal exports are poised for a solid month, but without being in contention for a new record.

Shipfix weekly order data for coal cargoes have been declining from recent highs, potentially as a result of surging coal prices. The development may suggest that seaborne coal flows could struggle to match recent record highs in the coming month. However, on an aggregate level, the order data for March looks solid, and in recent days there has also been a tendency towards a recovery in cargo orders. Hence, King Coal’s reign look set to continue for a bit longer.

Data Source: Shipfix