As we have been examining in our Weekly Dry Bulk Reports since the start of the conflict in Ukraine, we continue to stress that a prolonged conflict will continue to increase the likelihood of the dry bulk market being unable to fully offset a loss of Russian/Ukrainian cargoes from other nations. The sooner the conflict ends, the less that total grain export volume is likely to be affected. We still do not see any major replacement for lost Ukrainian and Russian grain cargo volumes. Prior to the war, we were of the opinion that global harvests this year will be what drives global grain trade, and our view has remained in place as fears of fertilizers shortages, global food crisis, etc. have only intensified.

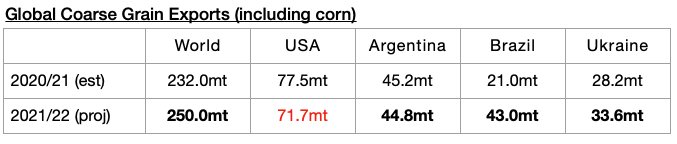

Globally, of note is that expectations for global seaborne coarse grain exports remain robust despite the lower expectations for exports from Ukraine. Global coarse grain exports in 2021/22 are now expected to total 250 million tons. This is 3.1 million tons 100,000 tons (-1%) less than was forecast a month ago but would mark a year-on-year increase of 18 million tons (8%). While the forecast for Ukrainian coarse grain exports has been lowered by 6.2 million tons from a month ago, the forecast for exports from the United States and other exporters has been raised by small amounts.

Global wheat exports are expected to total 203.2 million tons. This is 3.5 million tons (-2%) less than was forecast a month ago and would mark a year-on-year increase of only 600,000 tons.

Ironically, as the forecasts for Ukrainian and Russian exports have begun to be lowered, the forecast for Brazilian soybean exports continues to be lowered as well. This has led to the forecast for global soybean exports being lowered ever further. Global soybean exports (soybeans are not technically classified as a grain) are expected to total 158.6 million tons. This is 6.4 million tons (-4%) less than was forecast a month ago and would mark a year-on-year decline of 5.9 million tons (-4%)

Global soymeal exports are expected to total 67.8 million tons. This is 800,000 tons (-1%) less than was forecast a month ago and would mark a year-on-year decline of 900,000 tons (-1%).