Bi-Weekly Report

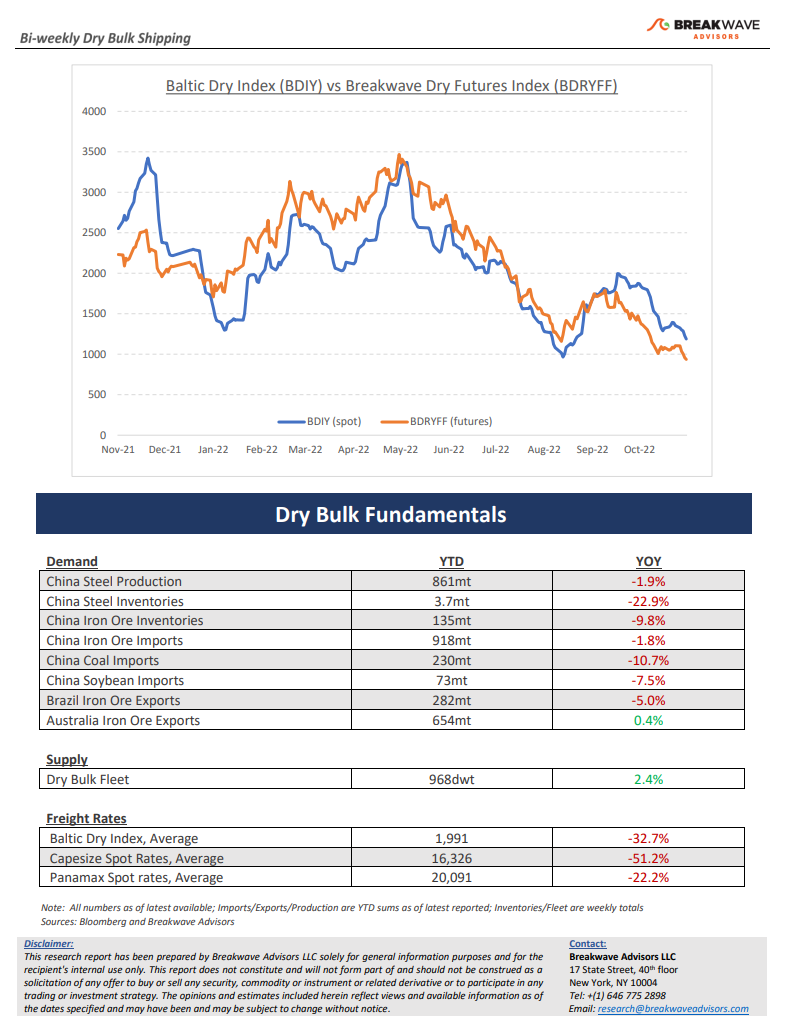

Weakest November for Capesizes in five years – Despite being quite an active month in terms of volumes, November has so far proven particularly weak for the large bulkers. Although the first fortnight of November has historically been relatively soft in terms of rates, so far there is a lack of some urgency from charterers to take cover for yearend dates, which in turn is translating into the current softness in spot Capesize rates. Looking forward, with the next six months priced at ~7,500, Capesize futures are already discounting a distressed market. The extreme caution reflects both historical downturns(the market has experienced depressed rates for months during the 2015- 2016 period) as well as the lack of catalysts that could tighten the current loose supply/demand balance. China, the most important demand center for dry bulk, continues to experience a very fragile recovery when it comes to commodities, while the rest of the world that has provided meaningful support over the past two years, is now faced with a rapidly slowing economy translating into nonexistent demand momentum for bulk goods. It is such a setup that makes market participants particularly concerned about the future. Interestingly, the current consensus outlook is exactly the opposite of what was priced-in this time last year, when expectations were for another very strong year (i.e., 2022). Freight futures are mainly a barometer of sentiment, and thus, spot price levels have a way to change sentiment let alone macro narratives. Although it is increasingly difficult to lay out a more bullish scenario based on current data, the price level of freight futures has already discounted a large part of the bearish outlook, providing an attractive price level for those who have a contrarian point of view about the future.

Covid policy and outbreaks remain the most important obstacle for China-related investments – The “Scottish shower” as it relates to Covid developments in China remains the focus of the commodities markets. On the one hand, some relaxation of the harsh policies seems to be the first step towards a broader reopening. On the other hand, news on outbreaks and lockdowns is an almost daily occurrence. The uncertainty that such an environment creates is evident in the high volatility that the global markets have been experiencing lately. For shipping, which is highly levered towards China, such an environment is also unconstructive. Indeed, for a meaningful recovery of China’s real estate sector, the Covid situation and outlook needs to be improved and some certainty about future housing demand needs to be established. When such a “pivot” will take place has been highly debated among China’s-focused analysts, and so far, the consensus is that come early spring, such a recovery might take place.

Dry bulk focus shifts back to fundamentals – Following a period of high uncertainty and significant disruptions across the commodity spectrum, the gradual normalization of trade is shifting the market’s attention back to the traditional demand and supply dynamics that have shaped dry bulk profitability for decades. As effective fleet supply growth for the next few years looks marginal, demand will be the main determinant of spot freight rates with China returning back to the driver’s seat as the dominant force of bulk imports.