Setting aside the spot market of the geared segments, the forty-fifth week was anything but dull. Risk assets rallied last Friday amid speculation that China was preparing to relax its pandemic restrictions. However, over the weekend, health officials reiterated their commitment to the “dynamic-clearing” approach to Covid-19 cases as soon as they emerge. Against this backdrop, US stock futures and commodities slipped in Asia on Monday.

In sync, Oil prices reported $1 a barrel loss on Monday, with Brent crude futures dropping as low as $96.50 earlier in the day and US West Texas Intermediate crude hitting a session-low of $90.4. Following a 7.5 percent increase last Friday, copper prices also traded lower on Monday as the reality of China’s “Zero-Covid” policy weighed on the industrial metal outlook. Capesizes, on the other hand, started the week on the right foot, with the BCI 5TC balancing at $11,648 daily on Monday's closing after reporting daily gains of $509.

On the same day, Norwegian Prime Minister Jonas Gahr Store and the US Special Presidential Envoy for Climate John Kerry chaired the launch of the Green Shipping Challenge during the World Leaders Summit of COP27. Countries, ports, and companies made more than 40 major announcements on issues such as innovations for ships, expansion in low- or zero-emission fuels, and policies to help promote the uptake of next-generation vessels.

Additionally, international zero-emission shipping routes came one step closer to becoming a reality, as the UK made a major pledge alongside the US, Norway, and the Netherlands to roll out green maritime links between them at this year’s COP27 conference in Sharm el Sheikh, Egypt. So-called ‘green shipping corridors’ are specific maritime routes decarbonised from end to end, including both land-side infrastructure and vessels.

Setting up such routes involves using zeroemission fuel or energy, putting in place refuelling or recharging infrastructure at ports, and deploying zero-emission capable vessels to demonstrate cleaner, more environmentally-friendly shipping on a given route. In particular, the UK and the US have agreed to launch a special Green Shipping Corridor Task Force focused on bringing together experts in the sector, encouraging vital research and development, and driving other important work and projects to see these initiatives come to life as quickly as possible.

The headline economic news this week though was neither related to the COP27 climate summit nor to the US midterm elections which dominated mainly the political press. Being the main theme of the front pages, the US inflation rate inched down in October at last! The all items index increased 7.7 percent for the 12 months ending October, this was the smallest 12-month increase since the period ending January 2022. The all items less food and energy index rose 6.3 percent over the last 12 months.

The energy index increased 17.6 percent for the 12 months ending October, and the food index increased 10.9 percent over the last year; all of these increases were smaller than for the period ending September.

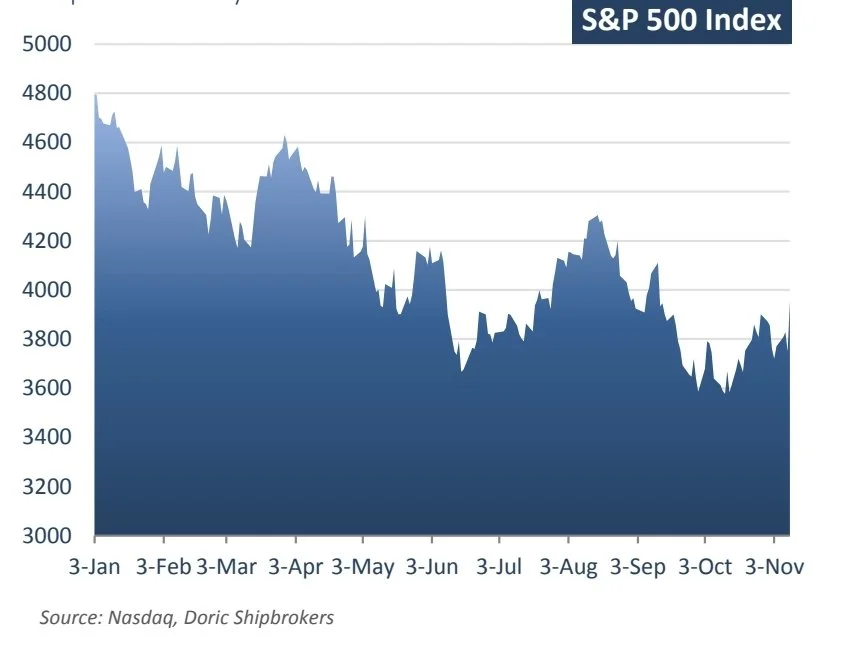

As expectations mounted that the Federal Reserve will increase interest rates by a lesser percentage next month compared to the recent increases, stock futures soared following the publication of the aforementioned figures. The S&P 500 surged by more than 5 percent after the data were published. The Nasdaq Composite surged by 7.35 percent – its best since March 2020 – closing at 11,114.15. Global stocks rose also on Friday – for a second day in a row – on hopes for less aggressive interest rate hikes from the Federal Reserve, an outlook that has the dollar facing its biggest two-day drop in almost 14 years.

Nevertheless, the week was not over yet. On Friday, Beijing eased some of its draconian Covid rules, shortening quarantines by two days for close contacts and for inbound travellers and removing a penalty for airlines for bringing in too many cases. Additionally, China will stop trying to identify “secondary” contacts. Markets were cheered by the loosening of the curbs, albeit many sources stressing that these measures were only incremental and reopening possibly remained way off.

Soever, oil prices reported strong gains in the last trading days of the week, on rising hopes of improved economic activity and demand in the world’s top crude importer. In tandem, industrial metal prices jumped on Friday, following a rise the day before in anticipation of a dovish pivot by the Fed. A weaker US dollar also supported commodity prices as it makes them relatively cheaper for buyers holding other currencies. Whilst short-term positive emotional factors are dominating most of the markets, dry bulk shipping seems to take small notice thereof.

Data source: Doric