The well documented slowdown in the Chinese economy has raised demand worries across the dry bulk market. We look at the causes and where potential upside may come from.

By Mark Nugent

Demand softening in Q4

A series of defaults in the property sector and slowing consumer activity following fresh Covid-19 restrictions has reared cause for concern over the strength of the Chinese economy. Chinese GDP increased by 4% YoY in Q4 2021, compared to growth of 6.5% over the same period a year ago, its slowest rate of growth over the last 18 months.

In terms of tonnes moved, Chinese imports on bulk carriers totalled 492.2m tonnes in the fourth quarter last year, declining by 2.2% YoY. This is the lowest quarterly total since Q2 2020 at the height of the pandemic.

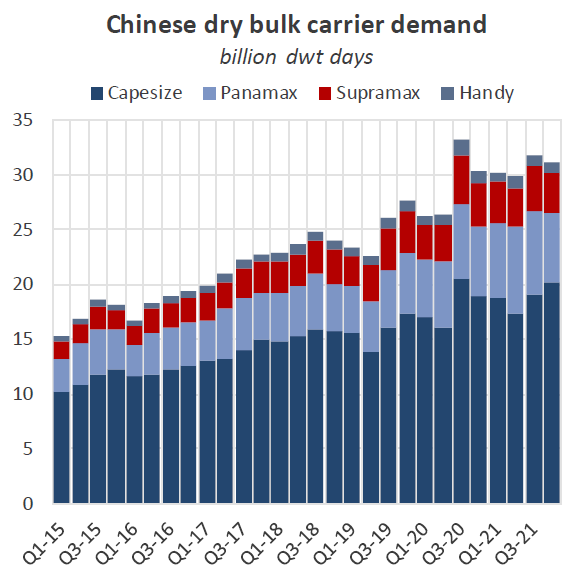

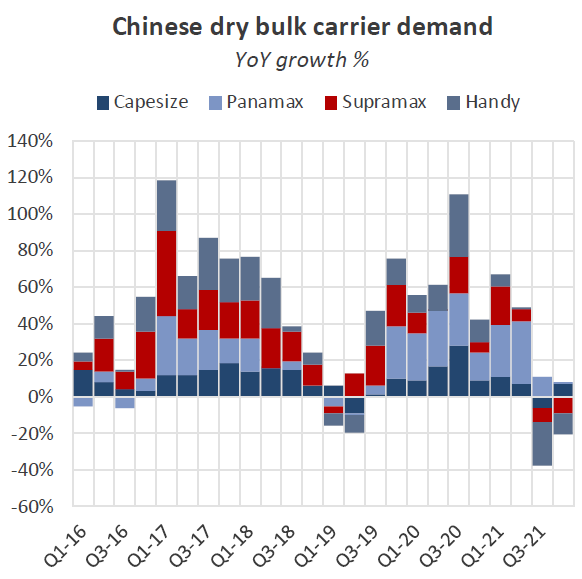

Chinese dry bulk import demand, across all vessel sizes, increased by 2.6% YoY in Q4 but slowed by 3% on a quarterly basis off the back of a seasonally strong Q3. When analysing this trend by vessel category, we can see demand growth in 2H21 has predominantly come from the Capesizes, increasing by 6.5% YoY, the strongest Q4 for this metric on record and the only vessel size in growth territory at the end of the year.

Towards the back end of 2021, total demand for Supramaxes and Handies declined by 9.3% and 11.1% YoY in Q4 2021 respectively. Weaker Chinese seaborne steel demand has contributed to this effect, with employment from longer haul steel trades from Brazil and Russia declining by 77.8% and 44.6% YoY in Q4.

Commodity breakdown

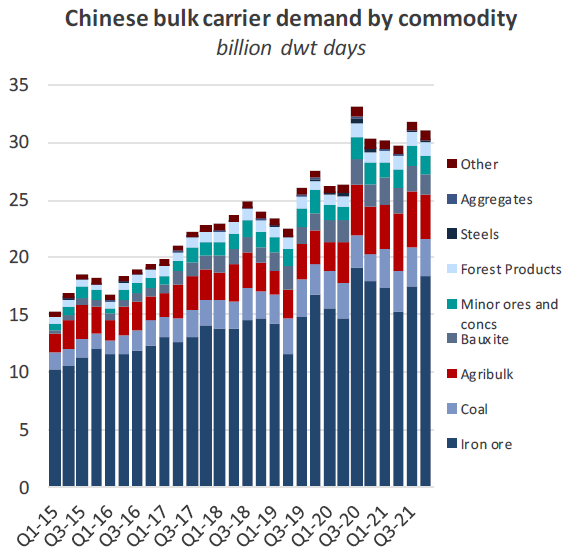

When breaking this down by commodity, shipping demand from Chinese iron ore imports has gained over two consecutive quarters, improving by 2.3% YoY in Q4. However, it has been the recent uptick in coal trade that has seen the greatest demand growth across all bulk commodities as China sought to ramp up inventories in 2H21 amidst domestic supply disruptions. Bulk carrier demand from Chinese coal imports improved 39.2% YoY in Q4, this trade’s highest annual growth rate since Q1 2018. This has primarily benefitted the Capes, as greater volumes have filtered through to the larger ships. This can in part be attributed to longer voyages for coal stems in 2021, with cargoes arriving in from Russia and the US becoming more frequent due to the Australian import ban. Further, this effect may intensify in the coming months following the announcement of the Indonesian coal export ban, despite some softening this week, it has been reported most miners still have not met their domestic sales obligation, prohibiting these producers from selling their product for export.

Chinese demand for seaborne grain, which has performed strongly since the start of the pandemic, recorded negative growth for the first time in Q4 since Q2 2019. Falling 9.5% YoY, compared to an abnormally strong Q4 2020, agribulk demand from China remains firmly above pre-pandemic levels as the country ramps up imports for food security. Although it is unclear to what extent China will be importing in 2022, the slowdown in demand in Q4 may signal grain stocks in the country are now near sufficient levels.

Steel production still muted

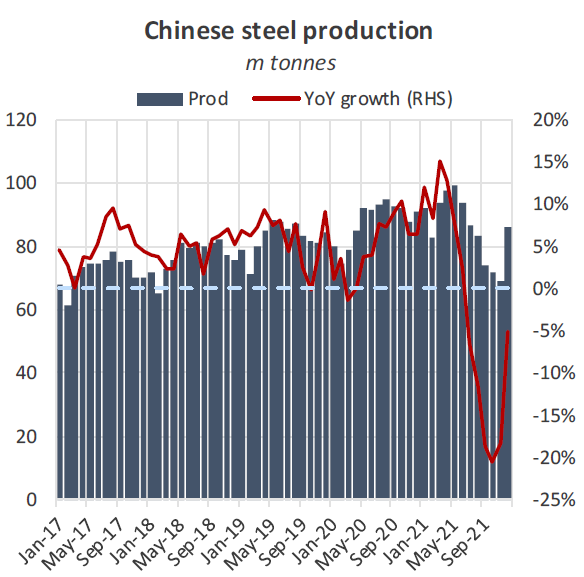

Chinese crude steel production totalled 86.2m tonnes in December according to the National Bureau of Statistics. Despite a 24.4% MoM improvement and the highest monthly output since July, this is still 5.5% lower YoY. Full year production fell 2.2% in 2021, coming in at a total of 1.03 billion tonnes.

A range of constraints in the Chinese steel sector, such as energy rationing and emissions controls have largely driven the decline in 2H21. As a result, utilisation rates at Chinese steel mills, which indicate the capacity at which mills are operating, have fallen to 18-month lows. For rebar in particular, which is used heavily in the construction sector, utilisation declined to 60.73% in December, the lowest figure since the start of 2018.

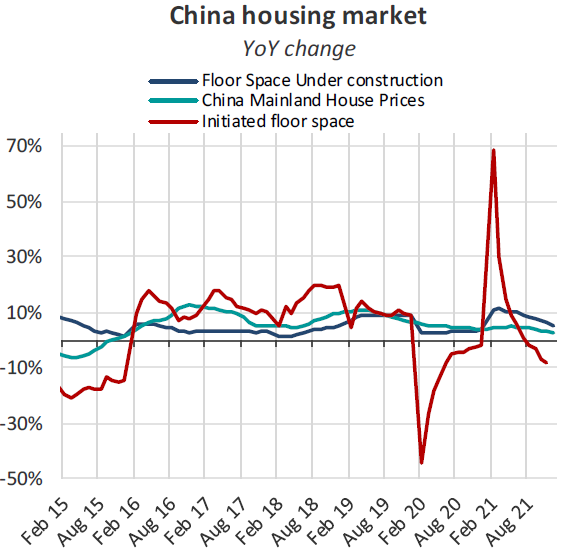

Continued drawdowns in housing

The Chinese property market has seen a swift decline since default rumours surrounding the Evergrande Property Group first emerged in September. Since then, more property firms have missed loan repayments, including those whose credit rating was investment grade, raising concerns the crisis is more systemic than previously thought.

As a result, liquidity in the Chinese housing market has thrust initiated floor space back into contractionary territory at -10.9%, levels considerably below those before the pandemic and the tenth successive month this figure has decelerated.

Outlook

Despite the slowdown in 2H21, the Chinese government has made several strides to spur economic activity and prevent any further downside in the property market. The government has eased lending restrictions, including lowering both the five and one-year loan prime rates this morning, and granted increased bond issuance to companies coming under pressure. These policies typically take time to filter through the economy before tangible results are realised, but if successful, we are likely to see an uptick in import demand for several bulk commodities.

The country’s energy shortage, which peaked in October, has somewhat tapered, giving opportunity for greater operational capacity within several industries that bulk carriers provide key inputs for. The upcoming Winter Olympics, which has delivered tighter emissions controls, particularly on steel, aluminium and cement manufacturers, will be concluded in mid-February, in which we will likely see an easing of these constraints.

The combination of these factors signals the current downside in Chinese dry bulk demand may be short-lived and an upturn in activity may be on the horizon.