Unsurprisingly, Capesize owners woke up in a bad mood with the New Year, and it was not only because of a bad hangover. January and February are the most dreaded months of the year for dry bulk, and throughout history Capesize rates have experienced significant weakness during those months due to a combination of factors but mainly related to weather. This year is no different, and already 12 days into the year, the mood around the physical Capesize desks has already turned quite sour.

However, such an environment is not necessarily bad for investors. After all, nobody is immune to mother nature when it comes to shipping and heavy rains in Brazil or possible cyclones in Australia can always disrupt iron ore trade and cause demand for ships to plummet.

What matters for freight is the averages, and if during the rest of the year demand proves resilient, then the first quarter will end up being the “known unknown” opportunity in an otherwise robust market.

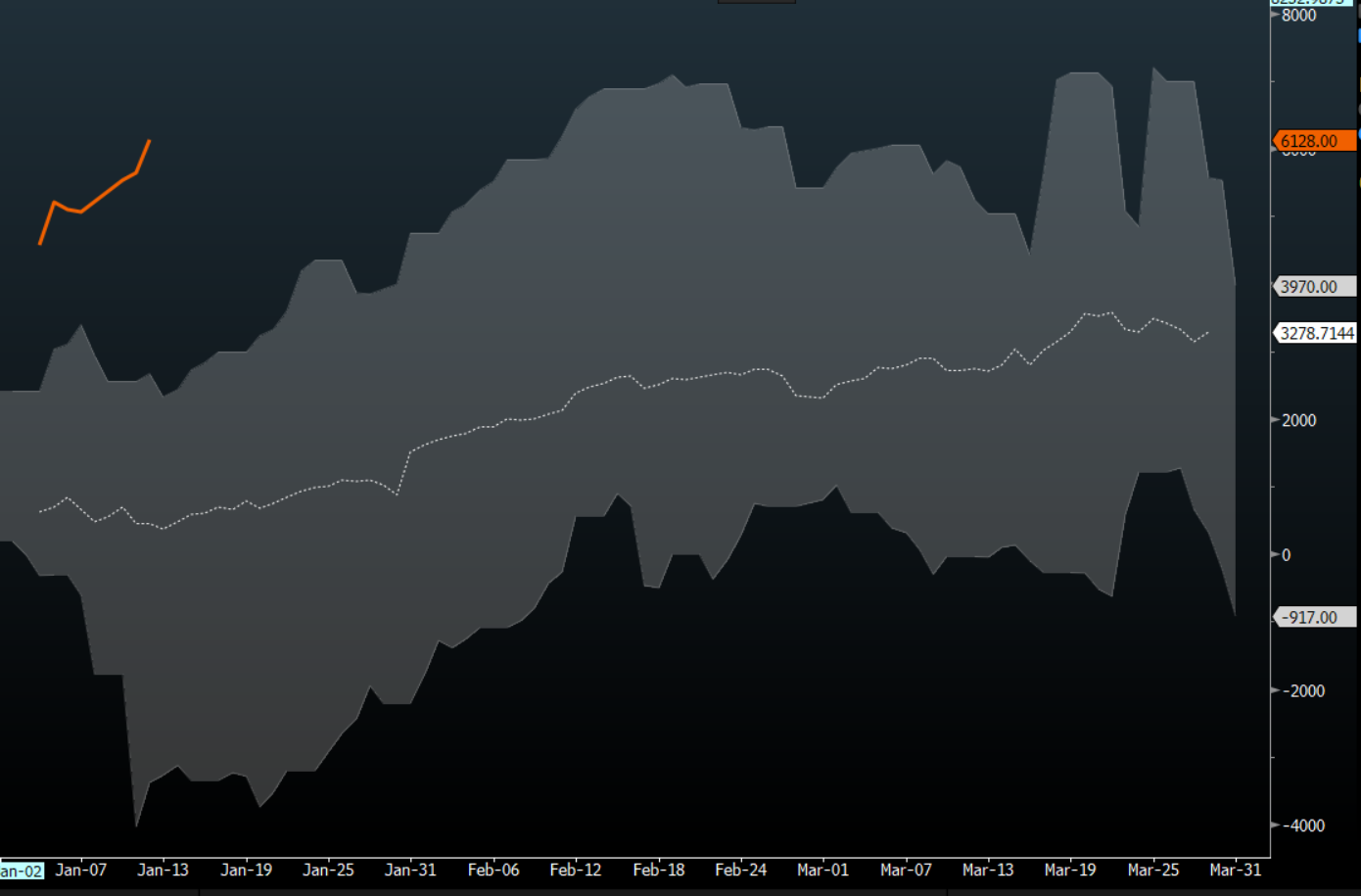

The futures market is clearly saying that the current weakness is temporary. Second quarter futures are trading at an unusually wide premium to the first quarter futures, signifying the optimism that market participants have for a recovery in rates (and the word “recovery” sounds quite dramatic, given that second quarter futures are “only” at ~22,000).

Q2 Capesize futures minus Q1 Capesize futures, 7-year range vs. Current (orange)

Source: Bloomberg

Is such optimism warranted for 2022? Are we going to see repeat of last year’s performance when the broader dry bulk market managed to post the best year in at least a decade?

After all, dry bulk rates were definitely not driven by an extraordinary boost in global demand for bulk commodities (iron ore, coal). If one was to just look at Capesize rates that managed to average north of 33,000 last year, such a market observer would have to at least expected some significant increase in seaborne iron ore trade.

That was hardly the case though. Coal trading did grow, but again, not to the extend one would have expected while iron ore seaborne trade was actually down(our estimated growth rates, just for the record, were 1.1% for coal and -1.5% for iron ore).

So, if demand was not there, what drove rates to new highs and why would one expect a similar performance to last year?

History clearly has shown again and again that strong bull markets in commodities are driven by supply constraints (while at the same time being enabled by steady demand). Shipping is no different. An extraordinary disruption in the global supply chain has had also an impact on dry bulk shipping, and although there are no specific choke points or easily identifiable congestion elements, it is the sub-optimal configuration of the dry bulk trade that has caused utilization to spike, causing the very strong rates experienced last year and that continue to affect the global shipping markets, from the gigantic container ships to the small bulk carriers.

Unfortunately, Capesize vessels have a very specific target audience, and thus, the direct impact of the global supply chain slowdown has been minimal. It is the indirect results that affected and could potentially continue to impact the Capesize trade, which can once again unexpectedly tighten the market and lead to much stronger rates.

It is not difficult to see why. During the early October days, when Capesize rates were hovering at the 100,000 level, major charterers were basically reporting that they were unable to find any ships to make their loading dates, with a handful ones that finally sped up and managed to make it, asking for the extraordinary prices we all experienced. It was only a few, and the reported rates were achieved by a handful of ships. This is the nature of the market, and the headlines rarely reflect the reality in the ground.

Is it possible to see a similar environment in the months ahead?

For starters, the global supply chain remains messy. Covid restrictions around the world continue to come and go causing port delays and operation inefficiencies. Weather, which has always been a wild card, exaggerates such elements although it can always lead to the opposite effect (great example the recent heavy rains in Brazil that are currently constraining iron ore exports).

Then, it is the broader economic picture that is also helping shipping. The macro environment remains accommodative with central banks (with China the most recent one) continuing to support the economies using different tools while a significant part of the recent economic stimulus been directed to infrastructure. Inflation, which has a positive correlation to commodity prices and thus freight rates, remains at multi-decade highs. Energy transition supports fossil fuels, at least in the near term, as renewable energy remains still unreliable.

Finally, the elephant in the room is fleet growth. The decade of oversupply that haunted the industry is behind us, and for now, there is little evidence that owners are about to go on an ordering spree despite the strong returns that ships are currently generating. There is simply too much uncertainty on the regulatory front as it relates to propulsion technologies and future fuels.

Source: Clarksons

The shipping investor (at least on dry bulk and containers for now) will be faced with considerable trading opportunities in the next 12 months. Equities have corrected to more reasonable valuations, freight futures are not at extravagant levels and volatility will be once again the main characteristic of the shipping universe.

We have entered the seasonally slow and weak period for dry bulk, and the bleaker the short term outlook, the greater the opportunity to take advantage of such low prices. It is impossible to call the bottom, but as the recent history has shown, one has to only be able to peak a relative low level, even if it’s not the absolute low.

Then, let the industry volatility and the mean-reverting nature of shipping do its magic…

Voilà!